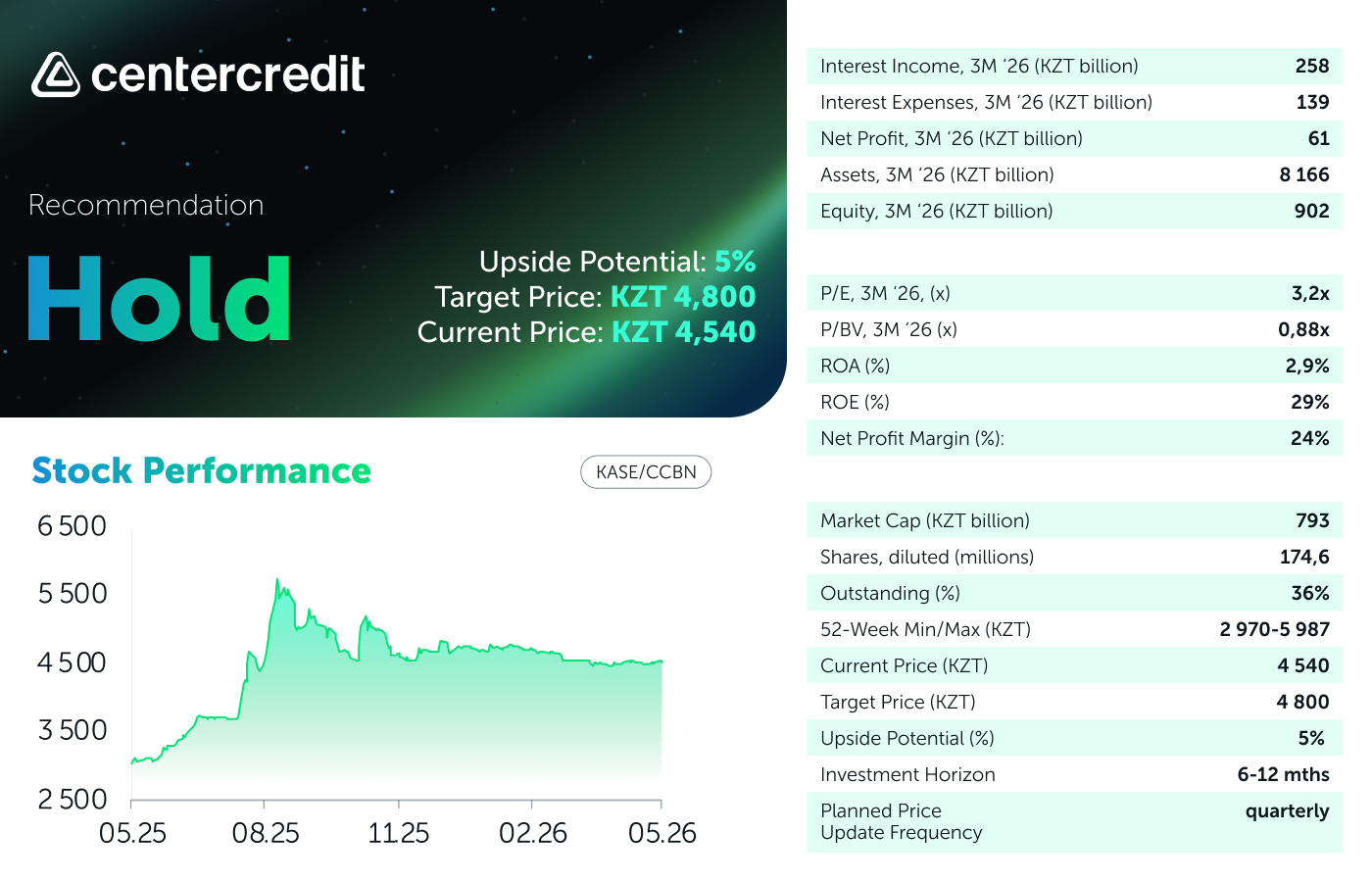

Bank CenterCredit has reported its performance for the Q1 2026. We assess the report as mixed: net profit decreased by 25% YoY, but this is largely due to a high base of last year, when certain income and expense items performed significantly better than current figures. Net interest income before provisions also set a new record for the third consecutive quarter, and credit loss expense stabilized. We have updated our key financial metrics in our valuation model and slightly lowered our expectations for interest expense and non-interest income. As a result, our target price per BCC share has increased from KZT 4,600 to KZT 4,800, with upside potential of 5% from the current level. Recommendation: Hold.

Interest Income: A New Quarterly Record. Quarterly interest income amounted to KZT 258 billion (+3.7% QoQ and +20% YoY), setting a new record for the third consecutive quarter. The main contributor to the growth was income from customer loans (+2.8% QoQ and +24% YoY). Interest expenses amounted to KZT 139 billion (+2.4% QoQ and +28% YoY), with the main pressure coming from customer deposit expenses (+33% YoY). The full redemption of subordinated bonds partially mitigated the increase in expenses. As a result, net interest income before reserves reached a record KZT 119 billion (+5.2% QoQ and +12% YoY).

Net Profit: Quarterly Figure YoY Declines for the First Time in 2.5 Years. Credit loss expenses stabilized at KZT 23.5 billion (-0.1% QoQ and -6% YoY), a positive sign after sharp increases in previous quarters. Net non-interest income declined sharply by 36% YoY, driven by a 31% YoY decline in fee and commission income and a high base of the last year's replenishment of provisions for expected credit losses on other financial assets. Foreign currency transaction income also declined by 11% YoY. Operating expenses increased by 16% YoY to KZT 54 billion, primarily due to payroll (+16% YoY) and administrative expenses. The main pressure on profit was a 72% YoY increase in income tax expense due to a low base of last year (effective rate of 11%) and the likely increase in the tax rate for the banking sector from 2026. As a result, quarterly net profit decreased to KZT 61 billion (up 20% QoQ and down 25% YoY), and EPS was KZT 348. The net loan portfolio increased by 2.7% QoQ to KZT 4.62 trillion, with annual growth of 19% (versus 17% at the end of 2025). Cash interest income collection decreased from 97% a year earlier to 94.5%, flat with the previous quarter. The quick asset ratio for the quarter decreased from 45.4% to 41.9%.

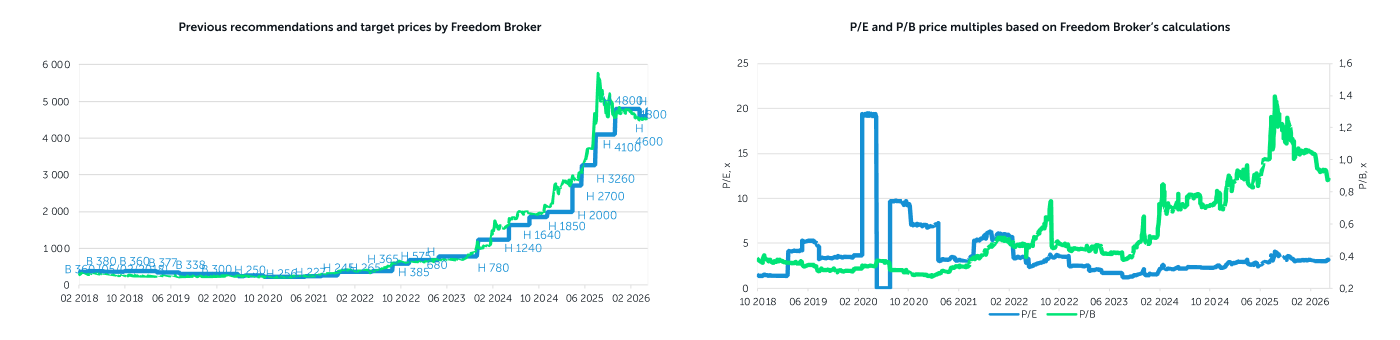

Our Opinion and Changes to the Valuation Model. The main risk is the increased tax burden, outpacing growth in interest expenses, and a decline in non-interest income, including fees, which has become a trend for publicly traded Kazakhstan banks. Further increases in minimum reserve requirements will likely negatively impact profitability in the second quarter. The valuation catalyst is record quarterly net interest income before provisions, driven by continued loan portfolio growth and improved operating efficiency. We also note a gradual easing of pressure on funding costs should the National Bank's base rate cut cycle begin. In our valuation model, we have updated our key financial indicators and improved our expense expectations amid a more rapid easing of monetary conditions. On the other hand, we have also downgraded our non-interest income forecasts, negatively impacting our valuation. As a result, the new target price for BCC shares has been increased from KZT 4,600 to KZT 4,800, with upside potential of 5% from current levels. Recommendation: Hold.

Author: Daniyar Orazbayev,

CFA, Investment Analyst

(+7) 727 311 10 64 (688) | [email protected]