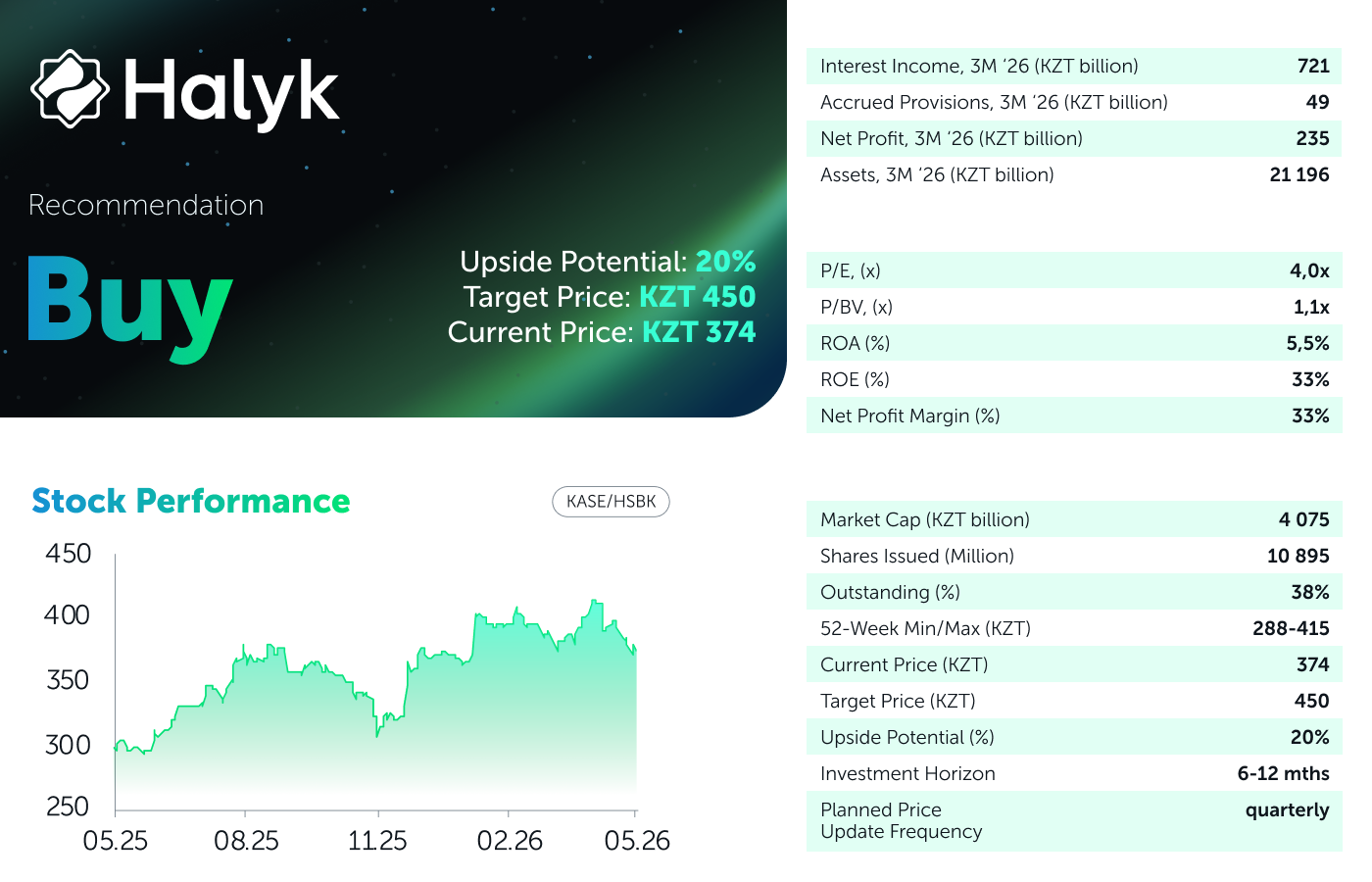

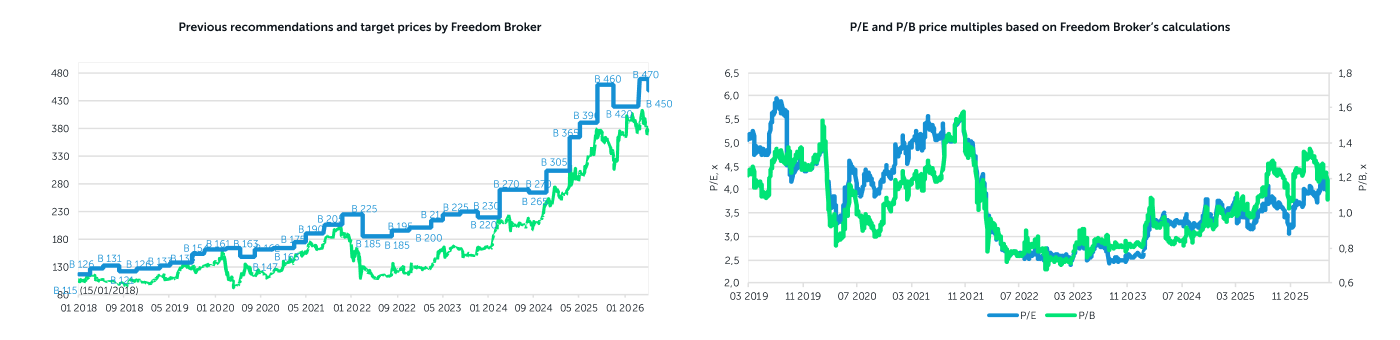

Halyk Bank JSC has published its financial results for Q1 2026. The report is assessed as moderately negative: quarterly net profit declined by 14.6% YoY, driven by higher credit loss provisions, as well as lower insurance and fee & commission income. Additional pressure stemmed from new minimum reserve requirement (MRR) ratios. Notably, another MRR hike is likely to weigh on the net interest margin (NIM) as early as Q2. Nonetheless, most of the management’s 2026 forecasts remains on track so far, with a recovery in fee & commission income expected in the next quarter. A key underlying assumption continues to be a reduction in the base rate, which we expect to commence in the second half of the year. In our valuation model, we have lowered our forecasts for net fee & commission income and non‑interest income. At the same time, operating expenses came in below expectations, prompting a downward revision to our operating cost outlook. As a result, the projected net profit for 2026 has been reduced. The target price for one share of Halyk Bank has been lowered from KZT 470 to KZT 450, implying a 20 % upside potential from current levels. Recommendation: Buy.

Core Valuation Factors. The main risk is the ongoing pressure on margins amid deteriorating asset quality. The cost of funding from customer deposits has increased from 8.2% to 10% YoY, although the growth rate has already slowed down amid stabilization of the National Bank’s base rate. The Group was able to stabilize the overall net interest margin (NIM) at 7.0% through active rebalancing of its securities portfolio. However, the new increase in the MRR since early April may put pressure on the margin indicator. Over the quarter, the average yield on securities jumped from 8.9% to 10% thanks to an increased position in National Bank of the Republic of Kazakhstan (NBRK) notes. At the same time, credit loss expenses remain elevated, and the NPL 90+ continues to rise, reaching 4.7%. Management indicates that this increase is linked to a moratorium on the sale of distressed retail loans to debt collectors. Additional pressure came from a contraction in balance sheet metrics: the gross loan portfolio decreased by 2.2% QoQ, and customer deposits fell by 3.1% QoQ amid tenge appreciation. The key catalyst remains the Group’s strong market position. The Group holds a 30% market share in assets, 28% in deposits, 30% in the loan portfolio, and ensures 86% penetration among the largest taxpayers. MAU of the Halyk super‑app remains at 8.5 million users, while payment and transfer volumes through the app grew by 14% YoY. We also note that the Group remains fairly undervalued relative to its net profit.

Growing Revenues, Declining Profits, First Signs of Stabilization. In Q1 2026, interest income reached a record KZT 721 billion (+15% YoY, +2% QoQ). At the same time, interest expenses rose by 28% YoY and fell by 0.4% QoQ to KZT 388 billion, continuing to weigh on profitability. As a result, net interest income before credit loss provisions amounted to KZT 333 billion (+2.3% YoY, +4.4% QoQ). Quarterly credit loss expenses totalled KZT 49 billion (+77% YoY, +2% QoQ). Consequently, the cost of risk stood at 1.5%, up from 1.3% in the previous quarter and 1.2% a year ago. Net fee and commission income showed the weakest performance in the past two years, reaching KZT 25 billion (−26% YoY, −35% QoQ). Management identified several factors affecting the quarterly dynamics: the new Tax Code, which led to a shift of client transactions to the end of 2025; tighter underwriting standards for short‑term BNPL products; a phased pass‑through of VAT on certain banking services to customers; an expanded loyalty program for SMEs. A recovery in momentum is expected in the next quarter. Net insurance income declined by 47% YoY to KZT 8.2 billion, becoming one of the key drivers of non‑interest income contraction. Operating expenses for the quarter amounted to KZT 74.6 billion (+7.8% YoY). Consequently, despite a sharp year‑over‑year increase in net profit from financial assets, quarterly net profit totalled KZT 235 billion, down 15% YoY and 5.5% QoQ. This represents the weakest quarterly net profit result in the past seven quarters. Earnings per share (EPS) amounted to KZT 21.57. The Group’s assets grew by 1.4% since the beginning of the year to KZT 21.2 trillion. Meanwhile, the securities portfolio expanded by 7.6% QoQ to KZT 4.7 trillion, offsetting a 2.2% QoQ decline in the loan portfolio. The decline is observed in the corporate segment, where the portfolio contracted by 4.4% QoQ, while the retail segment delivered a neutral result. The share of liquid assets in total assets reached 38.4% (up from 34.7% at the beginning of the year), and the collection rate of interest income in cash improved sharply compared to the previous two quarters, rising from 91.3% in Q4 to 97%.

Changes to the Valuation Model and Our Opinion. Based on the results of the first quarter, progress towards achieving management’s 2026 forecasts appears mixed. On the one hand, the net interest margin (NIM), the cost‑to‑income ratio, and the cost of risk are tracking in line with or better than expected values. Moreover, the NIM has actually shown signs of stabilization for the first time in several quarters. On the other hand, annual net profit is currently 6% below the target level of KZT 1 trillion. We also note a 26% YoY decline in fee and commission income, instead of the expected 5–10% growth. The approved first portion of dividends for 2025, at KZT 30.1 per share, was slightly below our expectations of KZT 34. However, dividend levels may catch up in the second half of the year. At the same time, we note a number of positive factors: the expected reduction in the base rate in the second half of 2026 should begin to lower interest expenses; active rebalancing of the securities portfolio is already generating additional interest income; a notable improvement in capital adequacy creates a safety buffer and potential for future dividends. In our valuation model, we have lowered the net profit forecast for 2026 due to reduced projections for net fee and commission income and non‑interest income. On the other hand, operating expenses came in below expectations. As a result, the target price for a share of Halyk Bank has been reduced from KZT 470 to KZT 450, with a 20 % upside potential from the current price. Recommendation: Buy.

Author:

Daniyar Orazbayev,

CFA, Investment Analyst

(+7) 727 311 10 64 (688) | [email protected]