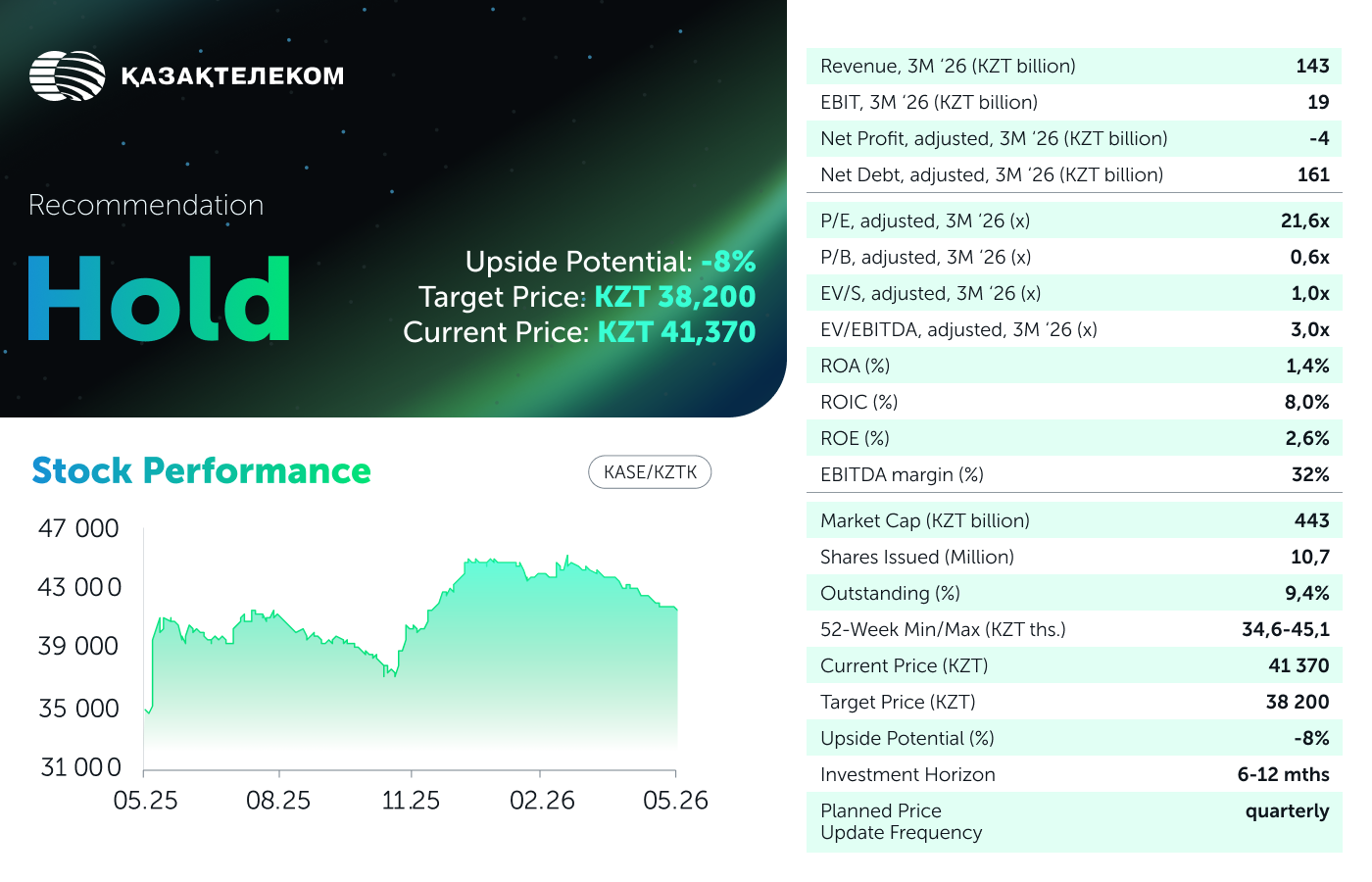

We assess Kazakhtelecom’s Q1 Performance Report as moderately negative. Revenue showed a marginal increase, while margin metrics deteriorated year‑on‑year (YoY). The quarter ended with a net loss, largely due to a sharp appreciation of the tenge. The current depreciation of the tenge is likely to have a positive impact on overall net profit in the first half of the year. At the same time, capital expenditures (CapEx) increased significantly, which led to a deterioration in cash flow. In our valuation model, we have updated core financial metrics, revised CapEx forecasts upward (to reflect higher expected spending), and adjusted forecasts for certain expense items downward — as they demonstrated lower-than‑expected growth. As a result, our target price for one share of Kazakhtelecom has increased from KZT 37,900 to KZT 38,200, implying an 8 % upside relative to the current market price. Recommendation: Hold.

Core Valuation Factors. The main risk is margin contraction amid outpacing cost growth against a backdrop of moderate revenue dynamics. Gross margin contracted by 3.6 percentage points (p.p.), with the pressure being broad‑based: rising personnel expenses, higher costs of mobile device sales, and increased infrastructure costs. In parallel, debt load is rising, while CapEx remain elevated due to the ongoing 5G network deployment via Kcell and the development of digital infrastructure. The key valuation catalyst is a contingent consideration related to the sale of MTS, amounting to KZT 167 billion. However, this asset carries a two‑sided risk: a $400 million payment from Qatar’s Power International Holding is spread over three years and is subject to the fulfilment of certain deal conditions. A supporting factor is the 90% reduction in radio frequency usage fees; however, in absolute terms, the effect is limited to savings of approximately KZT 2 billion per quarter.

Revenue: Moderate Growth amid Fixed‑Segment Contraction. Quarterly revenue amounted to KZT 140.5 billion (+4.8% YoY), and including the government subsidy and rental income, total revenue reached nearly KZT 143 billion (+3.4% YoY). The mobile segment (Kcell) contributed most to this growth, with external revenue increasing by 13% YoY to KZT 65 billion, while the fixed-line segment declined by 1.2% YoY to KZT 75.4 billion. By service category, the main growth drivers were sales of mobile devices (+35% YoY), interconnection services (+15% YoY), and data transmission services (+3.1% YoY). Revenue from fixed and wireless telephony services showed a slight decline of 1.2% YoY, reflecting the structural decline in fixed-line telephony.

Margin Contraction amid Rising Personnel Costs. Cost of goods sold (COGS) rose by 8.2% YoY to KZT 115.5 billion, significantly outpacing revenue growth. The main driver was personnel expenses, which increased by 24% YoY. The cost of mobile device sales surged by 39% YoY, in line with higher sales volumes. The pressure was partially offset by a 35% YoY reduction in radio frequency usage fees to KZT 4.2 billion due to the aforementioned 90% discount. As a result, gross margin declined to 19.1%, down from 22.7% in the prior‑year period. General and administrative (G&A) expenses decreased by 5.0% YoY to KZT 8.8 billion, which partially mitigated operational pressure. Adjusted operating profit, excluding a one‑off gain from the sale of MTS amounting to KZT 162 billion and the related impairment of other non‑current financial assets of KZT 22.7 billion in the comparative period, amounted to KZT 19.4 billion, compared with KZT 18.6 billion in Q1 2025. According to our calculations, adjusted EBITDA margin declined from 35% to 32%.

Net Loss and Cash Flow Decline. Financial expenses rose by 23% YoY amid an expansion of the debt portfolio, while financial income declined by 17% YoY. The net foreign exchange loss amounted to KZT 8.9 billion, compared with a loss of KZT 19.2 billion a year earlier. The appreciation of the tenge against the US dollar led to a revaluation of the Group’s foreign currency assets and liabilities. As a result, the Group reported a net loss for the quarter of KZT 0.7 billion, and the net loss attributable to shareholders of the parent company reached KZT 2.3 billion. According to our calculations, adjusted net loss amounted to KZT 3.7 billion, compared with KZT 9.6 billion of net profit in the prior year. Cash flow from operating activities declined by 71% YoY, primarily due to a decrease in accounts payable and a 50% YoY increase in interest payments. CapEx remained at an elevated level of KZT 68.1 billion (+21% YoY), resulting in a substantial negative quarterly free cash flow (FCF) of approximately KZT 63 billion, compared with KZT -39 billion in the prior year. Thus, cash and cash equivalents, including short‑term financial assets, amounted to KZT 145 billion as of the end of March. This figure excludes long‑term financial assets arising from the sale of MTS. Net debt, including these assets, increased by 64% over the quarter, reaching KZT 161 billion.

Our Opinion and Changes to the Valuation Model. The report confirms the main risks embedded in our valuation model: moderate revenue growth; margin contraction amid outpacing cost growth; rising debt load; and sustained high level of CapEx, driven by the ongoing 5G deployment and digital infrastructure development. The key supporting factor remains the contingent consideration from the sale of MTS. The reduction in frequency spectrum fees also provides support to margin metrics. In the valuation model, we have updated the key financial indicators: the CapEx forecast for 2026 has been increased. The rise in net debt has had a negative impact on the valuation. On the other hand, forecasts for other income, administrative expenses, and selling expenses have been improved. As a result, our updated target price per share of Kazakhtelecom JSC is KZT 38,200, implying an 8% upside relative to the current market price. Recommendation: Hold.

Author: Daniyar Orazbayev,

CFA, Investment Analyst

(+7) 727 311 10 64 (688) | [email protected]