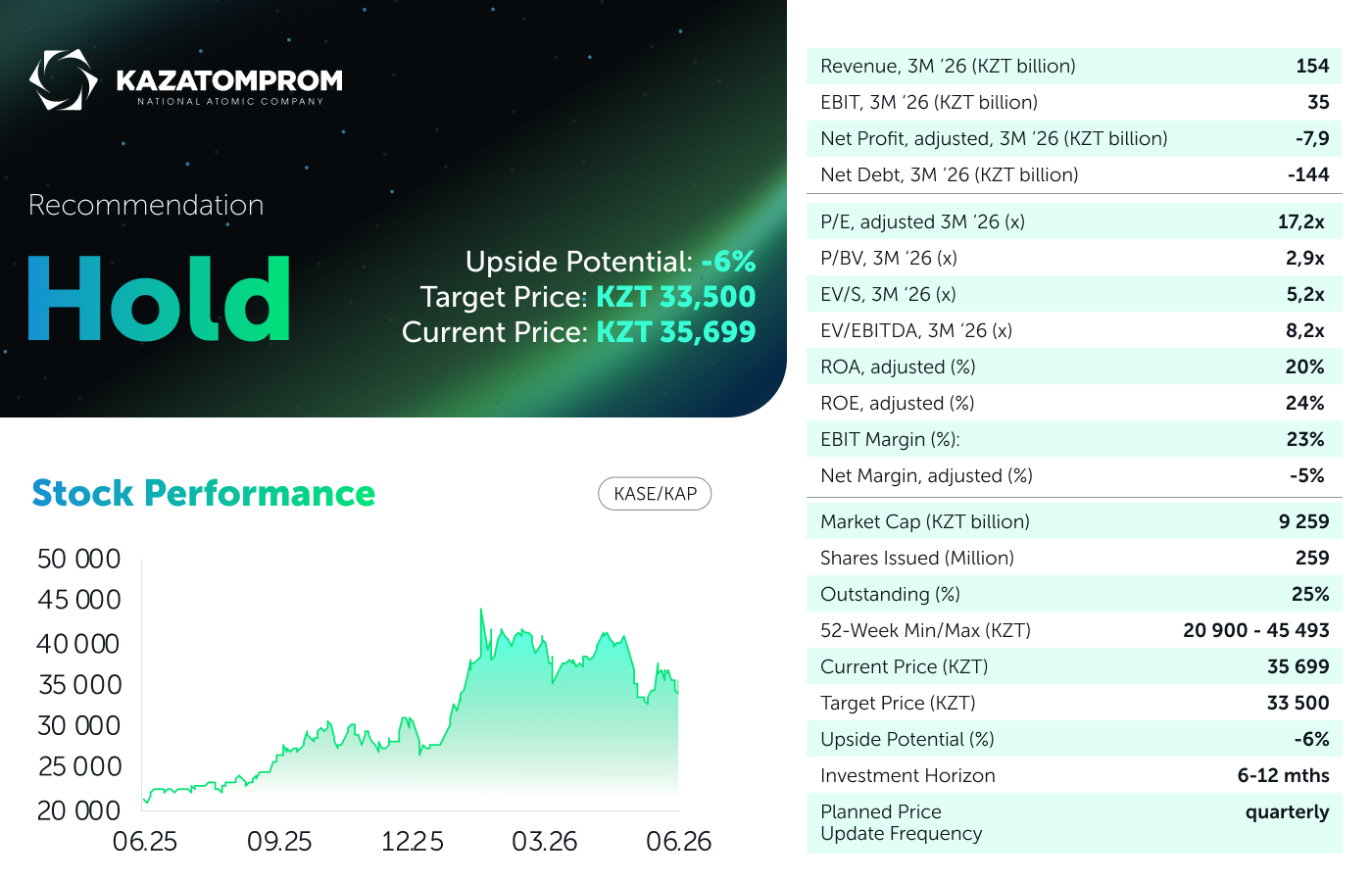

Kazatomprom JSC has released its Q1 2026 performance. We assess the report as neutral, adjusted for high quarterly volatility: revenue decreased by 28% YoY amid a 40% YoY decline in uranium sales volumes, driven solely by delivery timing. Production increased by 9-10% YoY, while the average selling price increased by 12% YoY. Net shareholder loss amounted to KZT 30 per share, almost entirely attributable to foreign exchange gains and the negative contribution of associates. The company confirmed all 2026 forecasts, leaving the operating forecasts in the valuation model unchanged. We updated our valuations for the major production assets Budenovskoye, KATCO, and Semizbay-U based on the audited 2025 results and lowered our average USD exchange rate assumption. As a result, the target price for Kazatomprom shares was reduced from KZT 35,500 to KZT 33,500, representing a 6% overvaluation of the current price. Recommendation: Hold.

Core Valuation Factors. The key structural factor remains the differentiated mineral extraction tax rate, introduced on January 1, 2026. Its impact is already visible in the financial statements and confirms the Company's own forecast of a 34% increase in C1 cash cost and a 21% YoY increase in AISC. However, the quarter was moderately positive operationally. Uranium production on a 100% basis increased by 9.1% YoY. The 40% YoY decline in sales was due to the timing of physical delivery, not a loss in volume: unsold inventory in Q1 was carried forward to subsequent periods, and all of the Company's annual forecasts remained unchanged. A significant event was the extension of the Akdala deposit rights: due to the expiration of the contract with “Joint Venture “South Mining Chemical Company” LLP on March 28, 2026, the site was transferred to the Group with execution of a new subsoil use contract effective March 29. The Group is required to reimburse SMCC for the book value of its assets in the amount of KZT 8.8 billion and has recognized a reserve for deposit restoration in the amount of KZT 10 billion.

Revenue Profile: Volume Decline due to Delayed Delivery Schedule. Consolidated revenue amounted to KZT 154 billion tenge (-28% YoY). Revenue from natural uranium sales fell by 35% YoY to KZT 122 billion, following volume declines. Production volume on a 100% basis increased by 9.1% YoY to 6.1 thousand tonnes, while production on a part-owner basis increased by 9.6% YoY to 3.2 thousand tonnes. However, sales volume fell by 40% YoY. This sharp decline is explained by the delayed delivery schedule of uranium to customers. On the other hand, non-uranium segments provided some support to revenue: tantalum products increased to KZT 4.4 billion (+228% YoY), while processing, transportation, and drilling services also increased.

Margin Profile: MET Pressure is Becoming Visible. Gross profit decreased by 35% YoY to KZT 50 billion, while gross margin narrowed from 35.7% to 32.5%. The main structural pressure factor, the differentiated MET rate effective January 1, 2026, has already been reflected in the financial statements: taxes other than income tax as part of the cost of sales increased by 78% YoY to KZT 18 billion. This is consistent with the Company's own forecast of a 34% increase in C1 and a 21% increase in AISC. Raw material and consumables costs decreased by 44% YoY to KZT 52 billion, following lower sales volumes and the purchase of uranium from joint ventures. Depreciation and amortization as part of the cost of sales remained stable at KZT 12 billion. The EBITDA margin fell from 35.5% to 30.8% due to rising costs. Net loss attributable to shareholders amounted to KZT 7.9 billion, compared to a profit of KZT 26 billion a year earlier. At the same time, total net profit amounted to KZT 14 billion, with a significant portion of this profit coming from the non-controlling stake of Inkay JV, which demonstrated a sharp increase in revenue and profit compared to a near-zero base last year. Additional pressure was also exerted by a KZT 22 billion foreign exchange loss amid the strengthening tenge. Operating cash flow declined sharply amid low quarterly sales, and free cash flow fell by 72%.

Our Opinion and Changes to the Valuation Model. The quarterly loss per share appears concerning only at first glance: it is almost entirely driven by non-cash and temporary factors (foreign exchange rate differences, a shifted sales schedule, and the consolidation structure). Operationally, the quarter was neutral, with growing production, rising selling prices, and confirmed annual forecasts. The pressure from the MET visible in the financial statements confirms the thesis of a structural increase in production costs in 2026. Since the company maintained all annual forecast, the operating factors and forecasts remained unchanged in the valuation model. Given the release of audited financial statements for 2025 for major production assets, we have updated the valuation models for Budenovskoye JV, KATKO JV, and Semizbay-U JV. A slight increase in production costs above our previous expectations led to a slight downward revision of the joint ventures. The expected average USD exchange rate has also been reduced from the previous forecast. The actual price is below expectations, which has led to a reduction in our valuation. As a result, the target price for Kazatomprom shares was reduced from KZT 35,500 to KZT 33,500, representing a 6% overvaluation of the current price. Recommendation: Hold.

Author: Daniyar Orazbayev,

CFA, Investment Analyst

(+7) 727 311 10 64 (688) | [email protected]