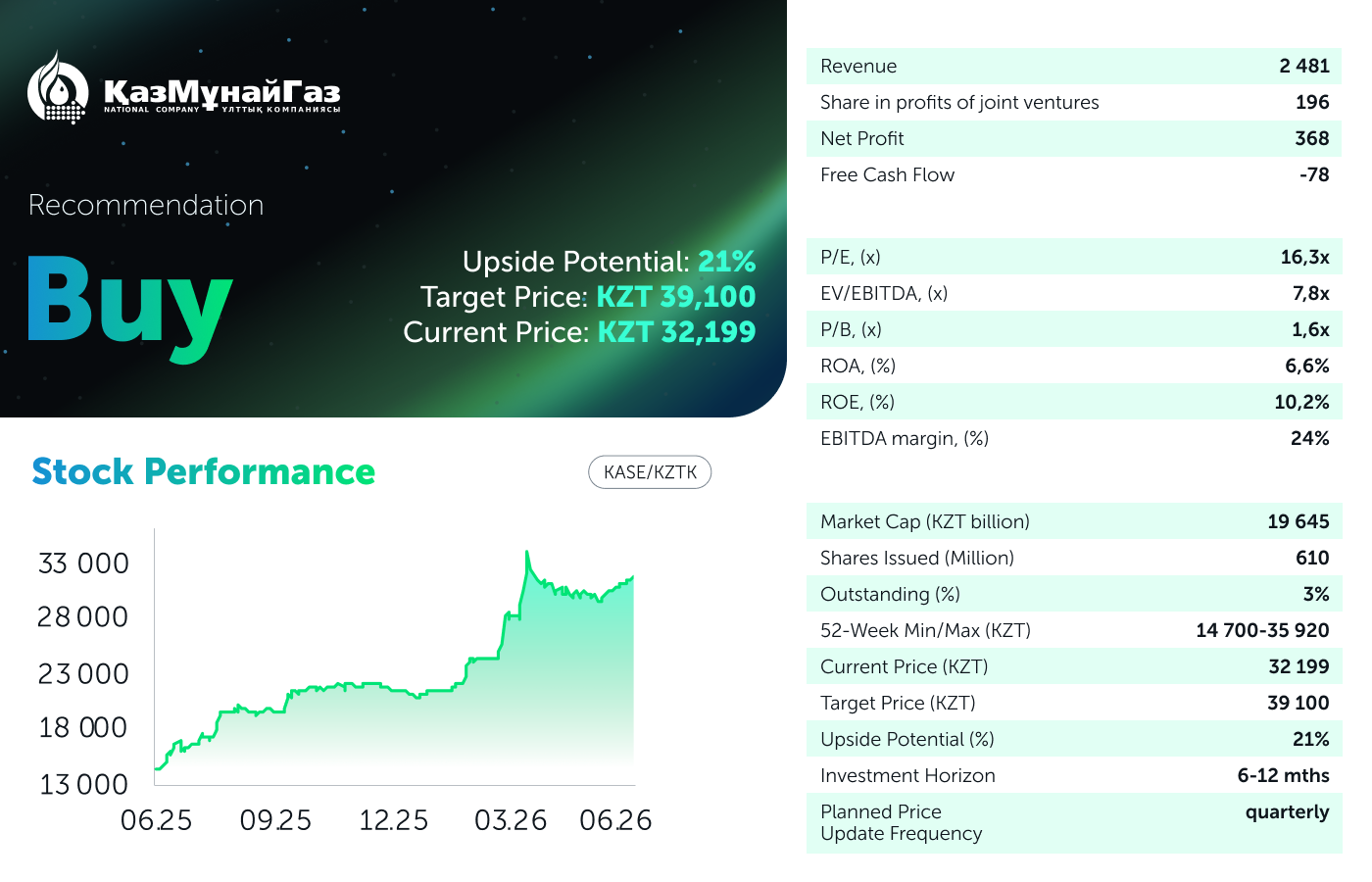

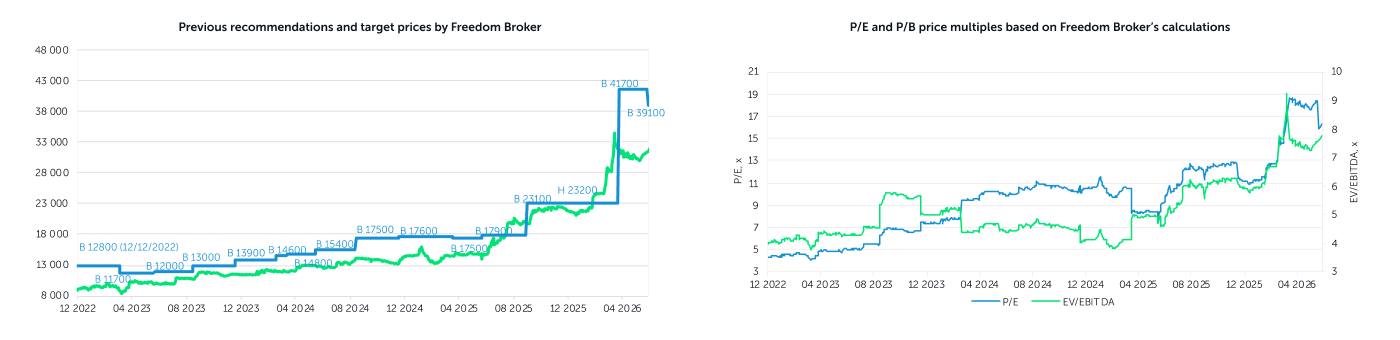

NC KazMunayGas JSC (KMG) has published its Q1 2026 financial results. We assess the report as neutral: net profit YoY nearly doubled, and revenue and EBITDA demonstrated solid growth; however, the improvement in metrics was primarily driven by higher oil prices, whereas the quarter proved weak from a production standpoint. Oil production fell by 12% YoY due to the January transformer fire at Tengiz and restrictions on oil acceptance by the CPC, while free cash flow turned negative for the first time in a long period, owing to a sharp rise in accounts receivable and capital expenditures. The debt burden remains very low, which also contributed to a 17% YoY increase in dividends. In our valuation model, we have updated the key financial and operational metrics and maintained the previous oil forecasts. The main impact on the price was caused by the adjustment of net debt. As a result, the target price has been reduced from KZT 41,700 per share to KZT 39,100, with an upside potential of 21%; the recommendation is Buy.

Core Valuation Factors. Oil prices were the main driver of the results: Brent averaged a 7.1% YoY increase, while KEBCO rose by 5.8% to USD 81.1 per barrel, with virtually zero discount to Brent. This enabled the company to boost revenue and its share in the profits of key joint ventures despite an unexpected volume shortfall caused by equipment failures. The share in TCO’s profit grew by 17% YoY even as production declined at Tengiz by 39% YoY, which underscores the high price sensitivity of the outcome. At the same time, CPC’s contribution decreased by 42% YoY to KZT 24 billion due to restrictions on the operation of single point moorings. The maintenance of a low debt burden and a cash pile of around KZT 2.9 trillion were factors supporting the dividend growth from KZT 491.71 to KZT 573.66 for 2025. Additional support to the cash position in Q2, apart from the recent weakening of the tenge, will come from dividends received in April: KZT 140 billion from TCO and KZT 24.5 billion from KC Energy Group. Among the risks, we highlight a possible reversal in oil prices and the dependence of transportation and production volumes on the operational stability of the CPC system amid the conflict in Ukraine.

Revenue: Growth Driven by Oil Prices amid Declining Volumes. Quarterly revenue amounted to KZT 2.48 trillion (+11% YoY), with growth recorded across all segments. The increase was driven by a 5.8% YoY rise in global oil prices and higher sales prices for petroleum products from KMG International; this was partially offset by a 2.5% YoY appreciation of the average tenge‑to‑dollar exchange rate. Revenues from the sale of crude oil and gas grew by 9.8% YoY to KZT 1.37 trillion, while revenues from petroleum products increased by 12% YoY to KZT 848 billion; oil transportation services added 29% YoY. At the same time, operating volumes declined: oil and gas condensate production fell by 12.0% YoY to 5.65 million tonnes, including a 27% YoY drop for megaprojects (Tengiz: −39%, Karachaganak: −19%) due to the January transformer fire at TCO and restrictions imposed by the CPC. The design production capacity was restored at Tengiz by the end of March. Production at operating assets grew by 0.9% YoY thanks to the launch of Western Prorva at Embamunaigas (+7.4%). Oil transportation decreased by 0.8% YoY to 20.8 million tonnes, with CPC volumes down 25% YoY; oil refining fell by 2.8% YoY to 5 million tonnes due to scheduled maintenance at Petromidia (−11%) and PKOP (−13.5%). The share in the profit of joint ventures and associates rose by 5.5% YoY, driven by TCO and MMG, while CPC’s profit declined by 42%. Total revenue, including other income, amounted to KZT 2.74 trillion (+11% YoY).

Margin Profile: EBITDA and Net Profit Rose, but FCF Turned Negative. The cost of purchased oil and petroleum products increased only by 2.0% YoY to KZT 1.24 trillion; operating expenses rose by 5.7% YoY, depreciation and amortization by 6.8% YoY, and transportation and sales expenses by 21% YoY. Taxes, excluding income tax, decreased by 1.6% YoY. Adjusted EBITDA grew by 6.8% YoY to KZT 591 billion, and margin expanded from 23.1% to 23.7%. Financial costs declined by 11% YoY to KZT 73 billion thanks to debt reduction. At the same time, impairment of property, plant and equipment virtually dropped to zero compared to the previous year. These factors drove a near‑doubling of net profit to KZT 368 billion (+94% YoY), or approximately KZT 603 per share. We note the profit growth despite an increase in foreign exchange loss (+39% YoY) due to the tenge’s appreciation. Free cash flow turned negative, amounting to minus KZT 78 billion versus plus KZT 283 billion a year earlier, driven by a KZT 504 billion rise in trade accounts receivable, a 64% YoY increase in CapEx, and low dividends from joint ventures (as TCO’s payout fell outside the reporting period). Net debt, according to our calculations, rose by 48% QoQ due to a decline in the cash position. At the same time, the leverage remains very low — around 0.3x net debt to EBITDA.

Our Opinion and Changes to the Valuation Model. The quarter proved eventful for KMG, with various developments exerting opposing impacts on financial results. On the one hand, the rise in oil prices in March—driven by geopolitical tensions—had a positive effect. On the other hand, certain incidents led to temporary operational constraints. The negative free cash flow was also affected by a one-off factor; upcoming dividends from joint ventures, received in April, are expected to return cash flow into positive range. Additionally, the sharp appreciation of the tenge has halted, which, combined with sustained relatively high oil prices, should support further improvement in financial metrics. In our valuation model, oil price assumptions have been maintained at previous levels. Among the adjustments, we have slightly increased CapEx expectations, while reducing administrative expense forecasts and raising the current USD/KZT exchange rate assumption. Nevertheless, the net debt adjustment had the most significant impact on the model. As a result, we have revised downward our target price for KazMunayGas shares from KZT 41,700 to KZT 39,100, implying a 21% upside potential from the current market price. Recommendation: Buy.

Author: Daniyar Orazbayev,

CFA, Investment Analyst

(+7) 727 311 10 64 (688) | [email protected]