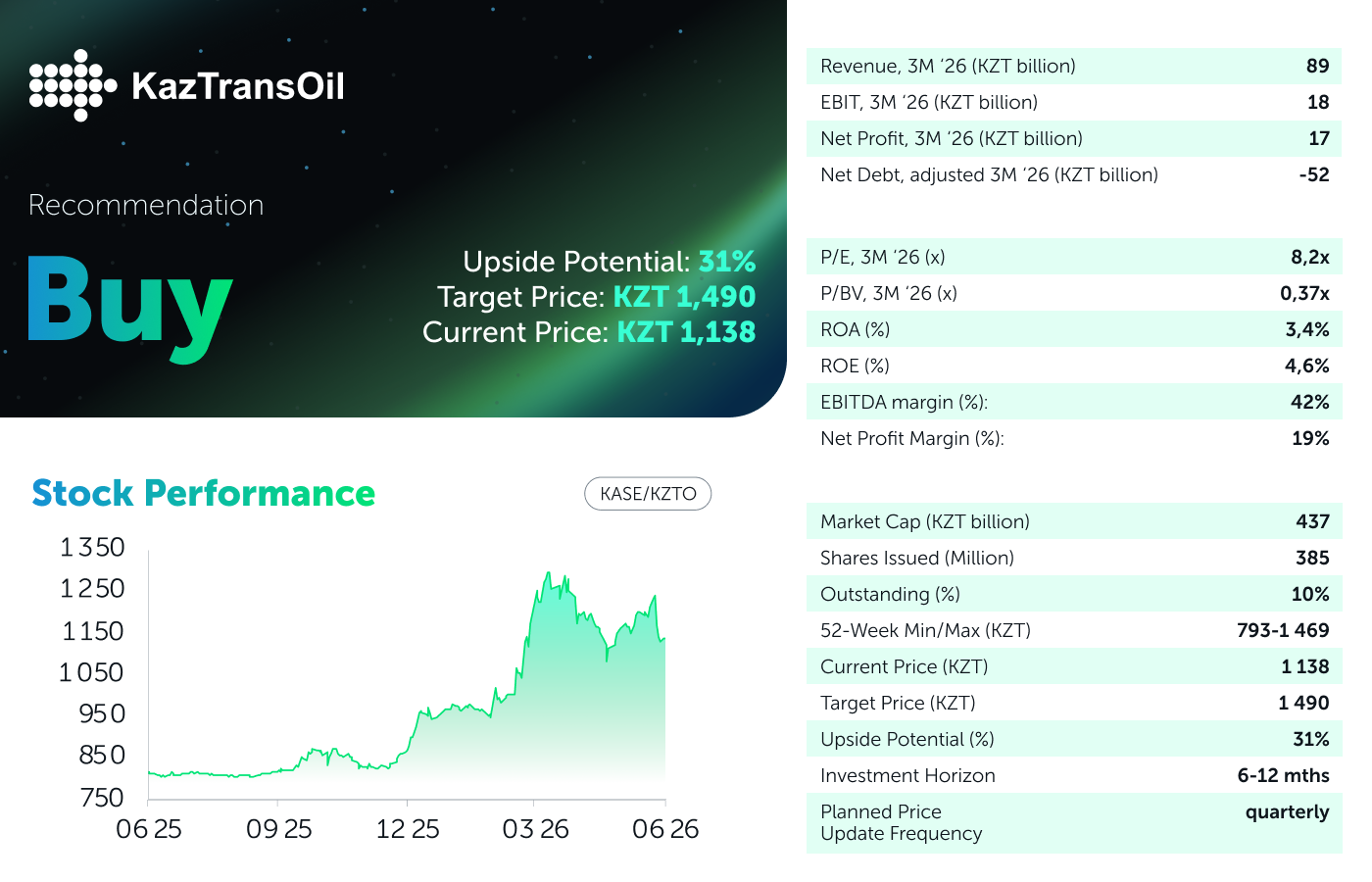

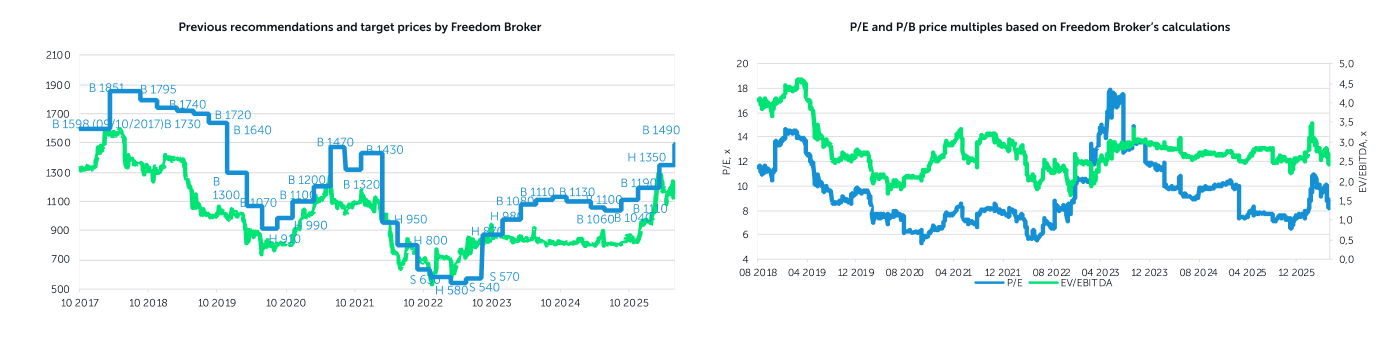

KazTransOil JSC published its financial results for the Q1 2026. We assess the report as positive: net profit surged 81% YoY to KZT 17 billion, gross margin expanded, and operating cash flow doubled. The growth was driven by higher transportation volumes, tariff increases, and strong interest income amid a record cash position, although a portion of the profit is one-time and non-cash in nature. A key positive was the dividend for 2025 declared at KZT 118 per share, exceeding both our expectations and the previous year’s pay-out. In our valuation model, the main growth driver is the approved increase in export tariffs. Other model assumptions were adjusted only marginally. As a result, our updated target price for KazTransOil shares has been raised from KZT 1,350 to KZT 1,490, implying 31% upside potential. The recommendation has been upgraded from Hold to Buy.

Core Valuation Factors. The key catalyst remains the tariff lever. The domestic oil transportation tariff effective January 1, 2026, was set at KZT 4,963 per ton per 1,000 km, up from KZT 4,462 in the prior year (an 11% YoY increase). An additional positive factor was the approval of a new export tariff of KZT 12,500 effective June 1, representing an 11% increase from the previous level. A strategic catalyst is the ongoing diversification of export routes to the western direction: deliveries of Kazakhstan crude oil into the Transneft system for onward shipment to Germany nearly doubled to 730,000 tons in the quarter, while throughput via the CPC rose 47% YoY to 1.3 million tons. Sanction-related uncertainty has significantly diminished following the U.S. Office of Foreign Assets Control (OFAC) extension of the license for Russian oil transit to China via Kazakhstan until March 19, 2027 (previously set to expire April 29, 2026). Furthermore, the UK’s Office of Financial Sanctions Implementation (OFSI) issued a general license permitting transactions with Transneft related to Kazakhstan oil, valid until March 18, 2028. We highlight the substantial liquidity position: cash and current financial assets reached approximately KZT 155 billion, a new record high, supporting both strong interest income and dividend sustainability.

Revenue Profile: Growth across All Key Segments Driven by Volumes and Tariffs. Quarterly revenue amounted to KZT 89 billion (+14% YoY). The largest revenue component — crude oil transportation — increased by 16% YoY to KZT 66 billion, driven by a 6.3% YoY rise in transportation volumes and higher tariffs on certain services. Revenue from pipeline operation and maintenance services grew 11% YoY, while water transportation revenue, in contrast to the previous quarter, increased by 14% YoY. The share of profits from joint ventures (CPC and MunaiTas) remained stable at KZT 4.7 billion (-1.4% YoY): a CPC decline to KZT 3.4 billion was offset by an increase at MunaiTas to KZT 1.3 billion.

Margin Profile: Margin Expansion and Strong Net Profit Growth. Gross margin improved from 14% in the prior year to 17%. Cost of sales increased by 10% YoY, driven by higher personnel expenses (+6.7% YoY) and depreciation & amortization (+23% YoY). Other operating income surged 167% YoY, primarily due to a reserve reversal on asset decommissioning and gains from inventory sales. As a result, operating profit rose 39% YoY to KZT 18 billion. EBITDA margin improved from 37% in the prior year to 42%. Financial income nearly tripled to KZT 9 billion; however, the quality of growth was mixed, as it included a significant one-time, non-cash gain from the modification of bonds and loans. Consequently, net profit reached KZT 17 billion, or KZT 44 per share, up 81% YoY. Excluding the one-time item, normalized net profit would have been approximately KZT 14 billion, still reflecting solid growth of 45% YoY. Quarterly operating cash flow doubled to KZT 32 billion, while free cash flow amounted to around KZT 15 billion, a significant increase from KZT 0.6 billion in the last year.

Our Opinion and Changes to the Valuation Model. The report confirms structurally strong performance: the tariff lever and volume growth are translating into margin expansion and a doubling of cash flow, driving robust net profit growth. Given the recent dividend increase and our forecast for continued growth in the company’s cash position supported by strong free cash flow generation, future dividends could remain at similarly high levels relative to net profit. Lifting of sanction-related risks is also positive, as it supports the potential for increasing oil transit volumes. On the other hand, the domestic tariff remains below the approved tariff schedule, and this could persist if the company continues to generate excess cash flows. This factor somewhat limits our valuation upside. In our valuation model, the key change was the nearly 11% increase in the export tariff, which had the most significant impact on our target price. We have also updated core financial and operational assumptions based on the company’s Q1 results. For the joint ventures CPC and MunaiTas, we revised operating expense and capital expenditure forecasts following their 2025 financial reporting, leading to a reassessment of their valuation. Additionally, we slightly raised the CapEx forecast for KazTransOil. As a result of these adjustments, we have raised our target price for KazTransOil shares from KZT 1,350 to KZT 1,490, implying 31% upside potential from the latest market price. The recommendation has been upgraded from Hold to Buy.

Author: Daniyar Orazbayev,

CFA, Investment Analyst

(+7) 727 311 10 64 (688) | [email protected]