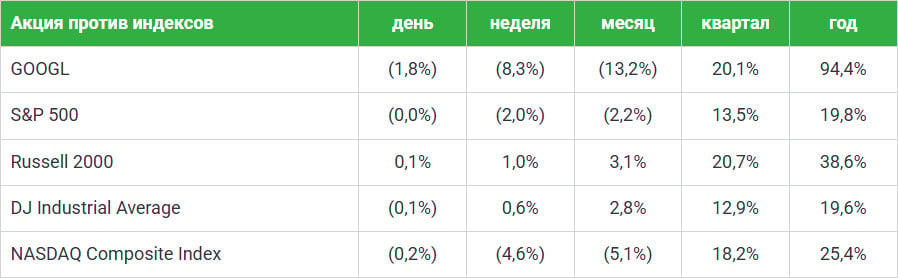

Analysts at Freedom Finance Global recommend buying Alphabet (GOOGL) shares, setting a target price of $400 per share. At the current price of about $360, the upside potential is 9.3%.

Why Freedom is positive on Alphabet

Alphabet (GOOGL) remains one of the largest technology holding companies, bringing together the Google search engine, advertising business, Google Cloud platform, YouTube service, Android operating system, and its own artificial intelligence developments.

Despite market concerns that the development of generative AI could weaken Google’s position in internet search, analysts believe these risks are overstated. On the contrary, the company is actively integrating artificial intelligence into its own products and using it as an additional source of business growth.

Strong business diversification

Analysts cite Alphabet’s diversified revenue structure as a key advantage. About 56% of the company’s advertising revenue comes from Search, the Gmail email client, Google Maps, and Google Play services. Another roughly 10% is generated by YouTube, about 7% by the Google Network ad network, and the Google Cloud division already accounts for around 15% of revenue. Additional contributions come from subscription services, Pixel devices, and other ecosystem products.

This structure allows the company to reduce dependence on individual business lines while simultaneously investing in new technologies.

Why the shares remain attractive

Vadim Merkulov, Director of the Analytical Department at Freedom Global, believes the market has not yet fully priced in the potential for AI monetization. The company is not only defending its leading position in internet search, but is also gradually turning AI into a tool for growing ad revenue, the cloud business, and the user ecosystem.

According to Freedom, AI implementation is already helping Alphabet increase search advertising revenue. The tools AI Overviews, AI Mode and the Gemini model are expanding search capabilities and gradually changing the way users interact with Google services.

In the first quarter, revenue in the Search & Other segment rose 19% year over year, while the Google Cloud business is showing double-digit growth (~15%) thanks to strong demand for computing power and services for training AI models.

What’s happening around Alphabet

Alphabet continues to strengthen its position as one of the key companies in the U.S. stock market. At the end of June, Google’s parent company joined the Dow Jones Industrial Average, replacing Verizon. Freedom noted that inclusion in the index does not in itself change the fundamental value of the business, but it may generate additional demand for the stock from index funds and ETFs as portfolios are rebalanced. At the same time, the stock’s further performance will still depend on how successfully the company can monetize its multibillion-dollar investments in artificial intelligence.

Earlier, Freedom analysts drew attention to Alphabet’s large-scale capital-raising program to finance the development of AI infrastructure. In their view, the construction of data centers and computing capacity signals a bet on long-term growth in demand for artificial intelligence services. If these investments deliver the expected financial returns, Alphabet will be able to strengthen its market position and support further revenue and profit growth.