Investment Review №331. At zero

Slow and steady wins the race

The positive external backdrop led to continued sideways movement in local stocks

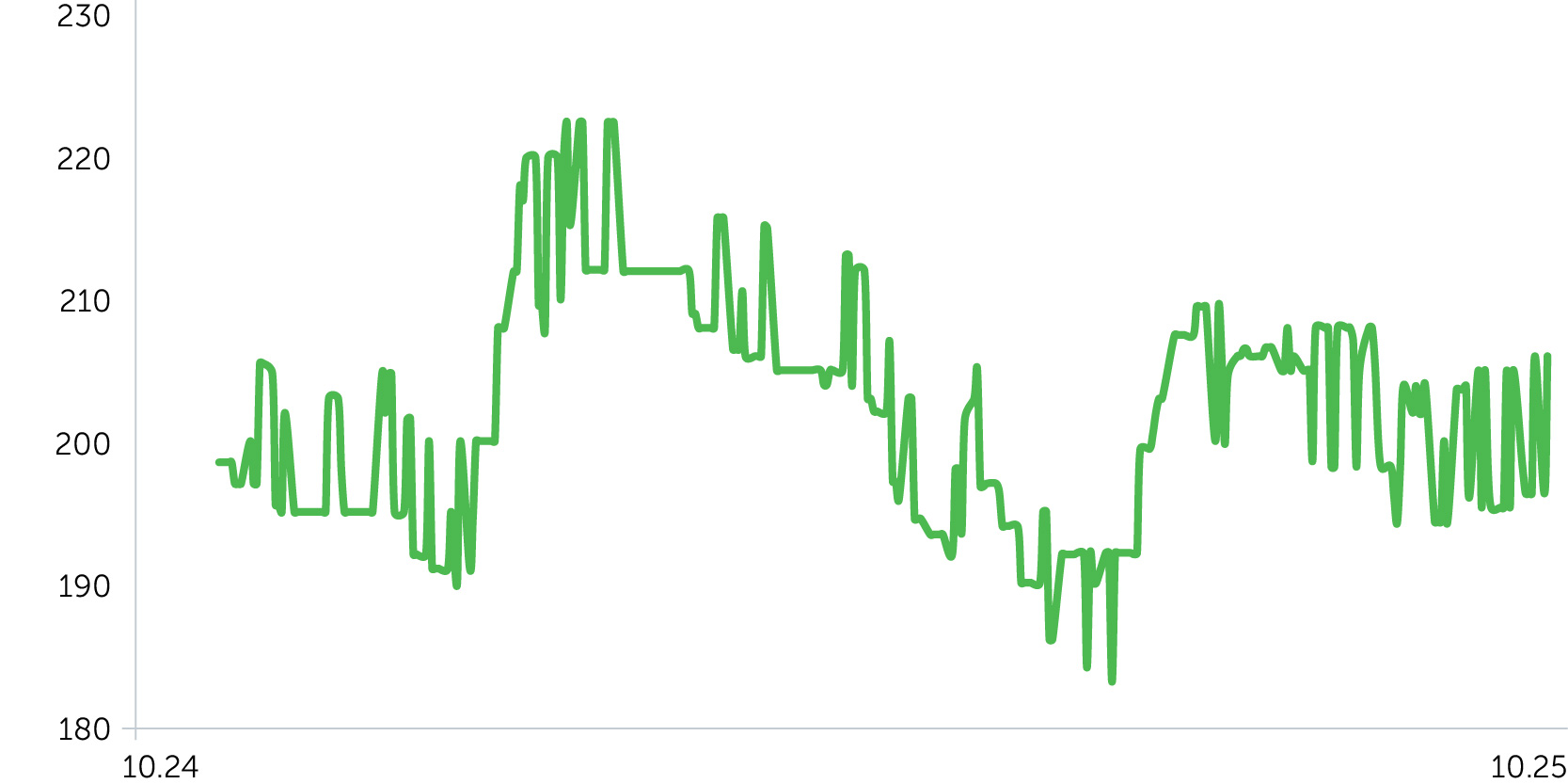

Telecom Armenia: 1-Year Stock Trends

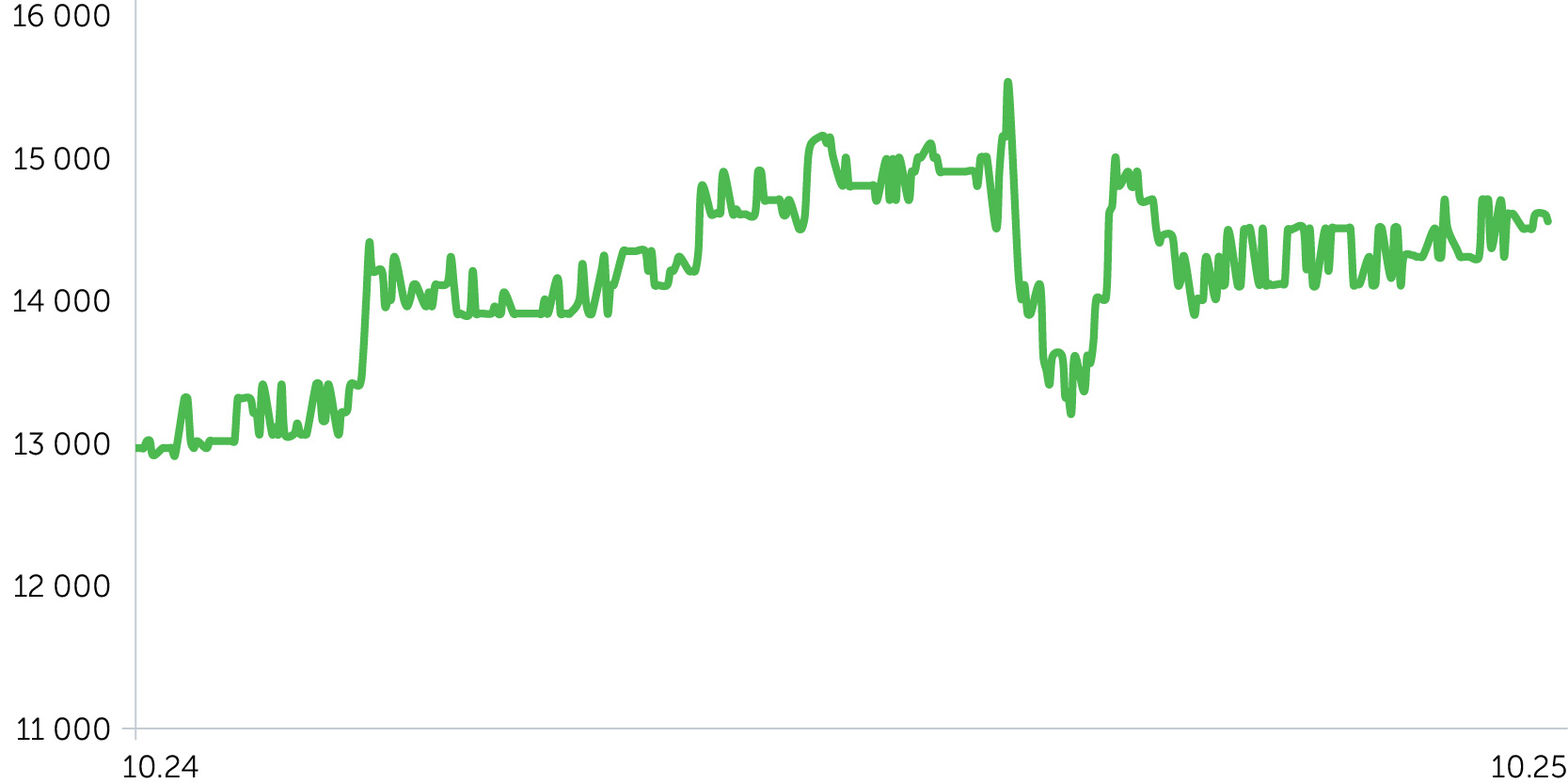

ACBA Bank: 1-Year Stock Trends

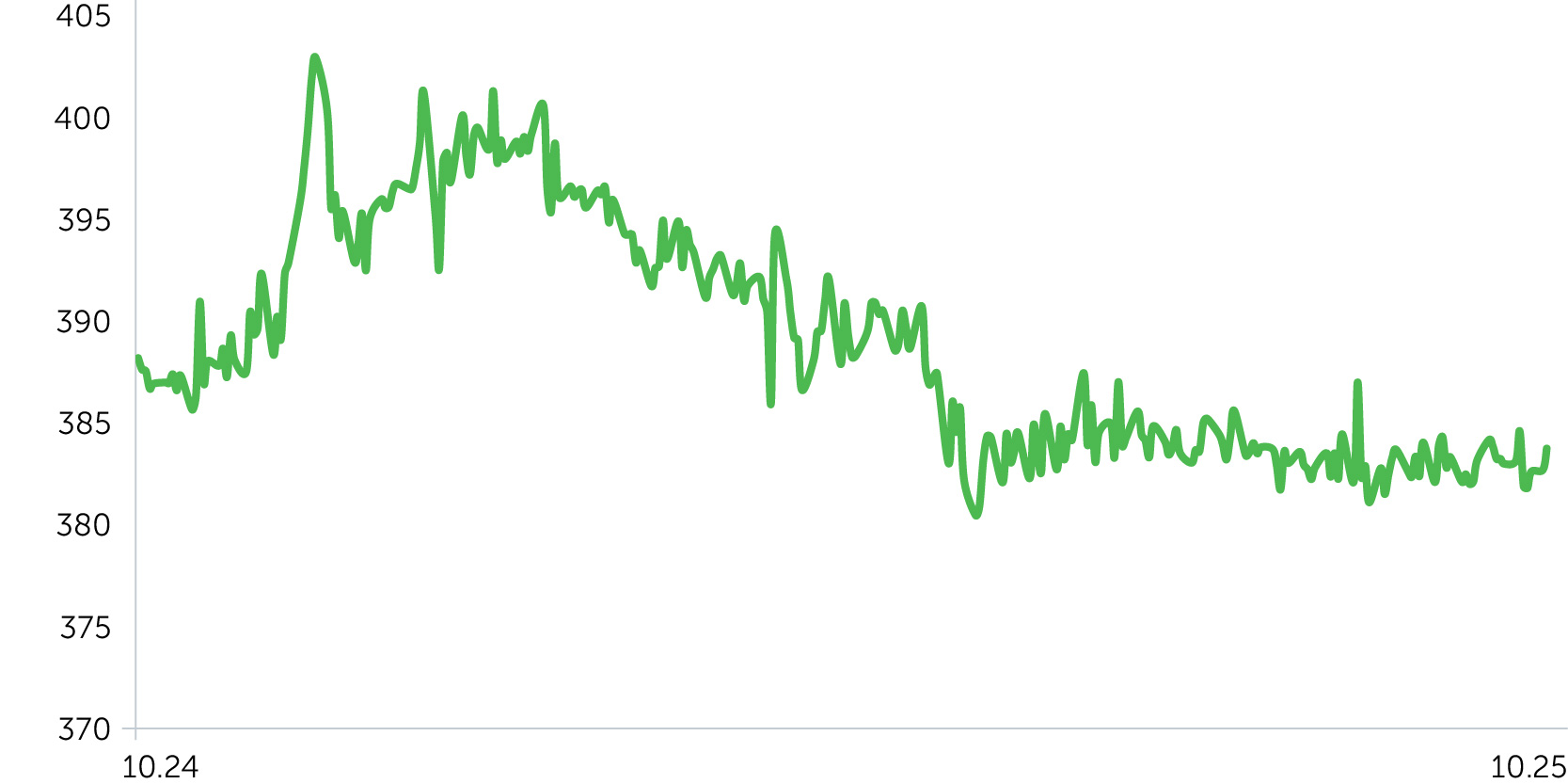

USD/AMD: 1-Year Dynamics

Between October 6 and 20, 2025, Acba Bank (ACBA) remained largely consolidated, retreating by 0.7% after a brief rally driven by strong Q3 2025 results. Notable drivers of this performance included a 22% year-over-year increase in net interest income and a 10.7% year-over-year rise in diluted EPS, which reached AMD 1,563 (~$4.09). The bank retained its third-place ranking within the industry by net profit.

Tell Cell (TLCL) shares corrected by 1.7%, though low trading volumes dampened the significance of this movement. Telecom Armenia (AMTL) posted a marginal increase of 0.5%, continuing to trade within the sideways range that has prevailed since early September.

The price index for three-year corporate bonds (denominated in drams) remained stable, reflecting a stabilization of inflation and inflation expectations, alongside a favorable macroeconomic environment. Our base case scenario suggests that the Central Bank of Armenia (CBA) will maintain its current refinancing rate in the near term, as the regulator likely adopts a "wait-and-see" approach given the balanced macroeconomic data. However, the CBA has indicated the potential for a gradual rate reduction to 6.25% over the next 12 months.

The dram-to-US dollar exchange rate remained virtually unchanged, strengthening by 3.1% year-to-date. The reduced currency volatility likely reflects the stabilization of external trade flows and active interventions by the CBA in the foreign exchange market to mitigate fluctuations.

Economic Updates

Between October 6 and 20, 2025, only a limited amount of macroeconomic data was released for Armenia. The real estate market showed signs of cooling, with a decrease in the number of transactions and a continued decline in the local price index. However, the IMF and World Bank raised their economic growth forecasts for Armenia.

- In August 2025, there were 4,542 real estate transactions involving sale and purchase, which is 10% lower than in July and 5.8% lower compared to the same month last year. The total number of transactions reached 18,780, with real estate alienations accounting for the majority of the overall transaction structure. The number of sale and purchase transactions, along with a decline in construction prices (down 6.7% from January to August, according to the latest available data), indicates a cooling demand in the country’s real estate market, potentially shifting investor interest toward financial instruments.

- Both the IMF and World Bank have raised their economic growth forecasts for Armenia. The IMF now expects 4.8% growth in 2025 (up from 4.5% in April) and 4.9% in 2026 (compared to 4.5% previously). Inflation is projected to reach 3.3% in 2025 and 2.8% in 2026, remaining close to the central bank's target range of 3% ±1 percentage point.

- The Eurasian Development Bank (EDB) has kept its forecast unchanged, expecting CPI growth in 2025 to remain within the regulator’s target range. Meanwhile, the World Bank, in its autumn review, has raised its projections: 5.2% for 2025 (+1.2 percentage points from its spring report), 4.9% for 2026 (+0.7 percentage points), and 4.7% for 2027 (+0.2 percentage points). The simultaneous upward revisions suggest stronger domestic demand and the potential adaptation of the economy to the normalization of re-export flows, which could serve as a long-term support factor for the local capital market.

- Armenia's domestic trade turnover in August 2025 increased by 1.7% year-over-year and 1.2% compared to July, reaching AMD 589,559.8 million. Within the total turnover, wholesale trade contributed 65.6% (+3.4% year-over-year), retail trade made up 30.4% (+4.6% year-over-year), and motor vehicle trade accounted for 4.0% (+6.0% year-over-year). The balanced growth across all trade segments underscores the resilience of domestic demand, a positive indicator for economic growth that may further support the central bank’s decision to maintain the current refinancing rate in the near term.

Corporate News

- AgroProm announced plans to invest $22 million in the construction of a greenhouse complex in Aragatsotn Province as part of the government’s agricultural sector support program. The first phase of the project will focus on cultivating tomatoes across 10 hectares, with 75% of the produce designated for export. The project is expected to create 225 jobs. Looking ahead, the area will be expanded to 30 hectares, with greenhouse management incorporating AI and modern agricultural technologies.

Two-Week Outlook

Between October 24 and November 3, 2025, several significant macroeconomic data releases are expected. There may also be updates to previously released data, though we do not anticipate substantial shifts in the current economic outlook.

The key release will be the Economic Activity Index for September (previous value: +7.5% year-over-year), which could influence sentiment in the local market. In our base case scenario, we do not expect a sharp deceleration in activity. However, a marked slowdown in growth, coupled with anchored inflation, could prompt the regulator to consider an earlier rate cut.

The Producer Price Index (PPI) is forecasted at 3.5% year-over-year, down from 5.1% in August, signaling a disinflationary trend at the upstream level. This would support the central bank’s current monetary policy stance. Retail sales data will serve as another gauge of consumer demand, with expected growth normalizing to 1.0% year-over-year, down from 1.7% in the previous month.