Investment Review №332. The Bulls switched to big tech

Review as of November 4

Global Perspective

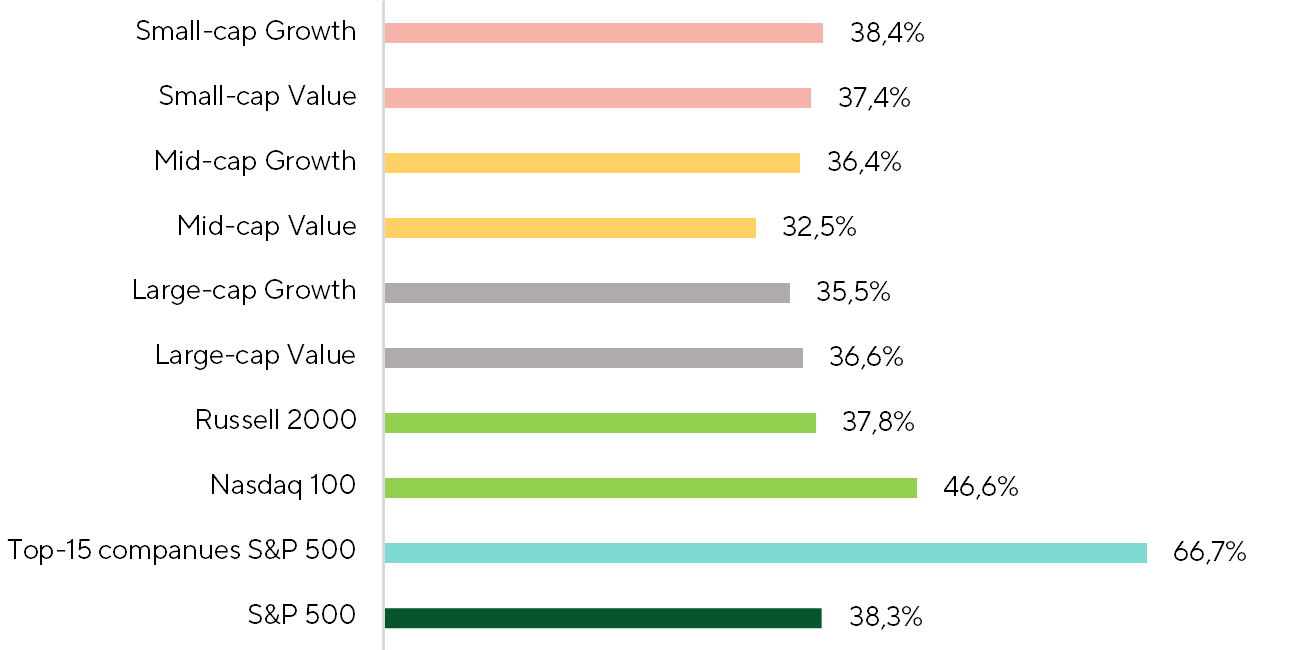

Over the past two weeks, major U.S. indices experienced gains, with the S&P 500 up 1.8%, the NASDAQ 100 rising 3.4%, and the Dow Jones Industrial Average advancing 0.7%. However, beneath the headline figures, the market saw a remarkable rotation. Breadth indicators reveal that the proportion of companies yielding positive returns over this period remained modest (see chart below), with most of the growth provided by the largest companies. Among the top 15 mega caps within the S&P 500, 67% posted gains, compared to just 38% for the overall index. Similarly, in the Russell 2000, only 37.8% of constituents recorded positive performance, underscoring that the current market advance is narrow.

Market breadth: share of companies with positive returns

Source: FactSet, Freedom Broker

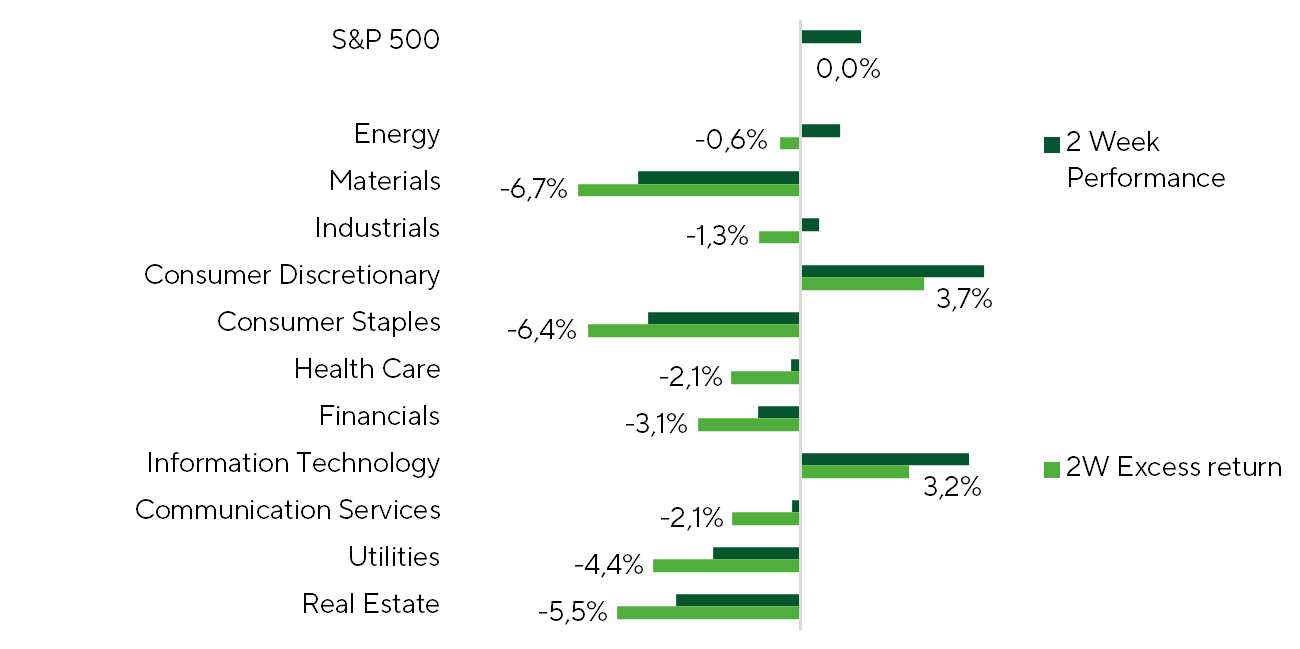

Excess returns of major US stock indices

Source: FactSet, Freedom Broker

The breakdown of returns by sector reflects the same trend, with IT and Consumer Durables emerging as key beneficiaries, as mega caps are mostly concentrated in these sectors. As a result of capital rotation, big tech firms once again came into focus. NVDA shares rose by 13.3% to reach a record market capitalization of $5 trillion, GOOG/GOOGL stock gained 10.6%, and AMZN surged by 17.3%.

This shift in sentiment was prompted by the outcome of the recent Fed meeting. As widely anticipated, the central bank cut the rate, while pivotal was Powell’s press conference commentary. He emphasized that the Fed’s policy remains flexible rather than being on “autopilot,” indicating that a rate cut in December is far from guaranteed. Fed Chair also highlighted that some macroeconomic data is being delayed due to the ongoing U.S. government shutdown, adding to the uncertainty of economic assessments. These remarks nudged the market to reassess expectations, and the probability of a December rate cut fell from 84.8% to 62.6% based on futures markets, and from 90% to 65% according to the Polymarket platform. The adjustment in expectations dampened risk appetite and triggered a partial capital rotation.

As to the shutdown, little has changed. Polymarket projects it to end by November 15, implying a duration of approximately 45 days and making it the longest in U.S. history. Until then, macroeconomic data releases remain highly limited.

Fed Meeting Details

Key takeaways from the Fed meeting: Chair Powell struck a cautious tone, and December is shaping up to be the most uncertain month on the policy calendar.

The Fed cut the rate by 25 basis points and announced that the QT program will end on December 1—both moves widely anticipated by the market. 10 committee members voted in favor of the rate cut, while Stephen Miran advocated for a more aggressive 50 basis point cut, and Jeffrey Schmidt preferred to keep the rate unchanged. During the press conference, Powell acknowledged that inflation risks remain elevated and the labor market is cooling, creating a complex landscape for policy decisions. He explained that the decision to end QT reflects “sufficient reserves” achieved in the banking system and clarified that proceeds from maturing mortgage-backed securities will now be reinvested in Treasury bonds. The key new signal was the acknowledgment of significant divisions within the committee over the December policy path. Powell also emphasized that the labor market’s cooling largely reflects weaker immigration and lower labor‑force participation, which softens the case for aggressive monetary‑policy easing. Fed Chair concluded with a cautious note, stating, “If we are in doubt, it is better not to change policy,” underscoring the Fed’s preference to move carefully. His address tempered market expectations for a December rate cut, emphasizing the regulator’s commitment to a flexible, yet restrained, policy stance.

Inflation

On October 24, a week ahead of the FOMC meeting, the September CPI report was released despite the ongoing government shutdown. Most data had been collected before the shutdown, and the report’s relevance to the October 28-29 meeting warranted its publication.

Inflation came in below expectations: headline CPI rose 0.31% m/m versus 0.4% predicted, while core CPI increased 0.23% m/m compared to the 0.3% consensus. On a year-over-year basis, both indices were up 3.0%.

The main driver of the higher headline CPI reading was fuel, with prices up 1.51% m/m, including a 4.2% m/m increase in gasoline (seasonally adjusted). This should prove temporary: we estimate fuel prices to decline about 1.5% in October, while the average annual growth in this category will remain around 1.3%. Elsewhere, the report contained no negative surprises. Recreational services prices rose modestly (+0.4% m/m), but their three-month average remains moderate at roughly 0.22% m/m. Overall, the data confirms a gradual easing in inflation pressures.

Earnings Season

In the large cap segment, earnings season is drawing to a close, with over 80% of S&P 500 constituents having already reported results. Preliminary data indicate the U.S. corporate sector remains solid, with aggregate Q3 EPS up 12.7% y/y, well ahead of the 7.0% consensus.

IT and Financials were the primary drivers, contributing 79% of total EPS growth. EPS in the IT sector rose by 26.9% y/y, and in Financials by 23.6% y/y. Within IT, semiconductor companies (EPS: +48.2% y/y) and software developers (EPS: +22.7% y/y) were the top performers.

The strong earnings season has prompted upward revisions to 2025–2026 forecasts. EPS growth expectations for 2025 have been raised to 11.6% y/y (from 10.9%), while the 2026 forecast has been nudged to 13.7% y/y (from 13.6%).

Market Focus

Over the next week and a half, investors will be focused on two key events: the Supreme Court’s review of Trump’s tariffs and developments around the government shutdown.

On November 5, the U.S. Supreme Court held hearing on the legality of tariffs imposed by Trump under the International Emergency Economic Powers Act. Several justices questioned whether a president can levy such duties without congressional approval. The central issue is whether the tariffs are a “regulatory tool,” as the administration asserts, or a tax, which falls under Congress’ exclusive authority. If the Court rules against the White House, the tariffs could be deemed unlawful, prompting refunds of duties collected, administrative complications, and a search for alternative legal mechanisms to regulate imports. Moreover, the case will set a significant precedent: a ruling in Trump’s favor would bolster the executive authority to pursue the America First strategy, while an adverse ruling would reassert Congress’ control over tariff policy. At the macro level, the outcome may influence supply chains, inflation, and risk sentiment. Polymarket estimates a 75% probability that the tariffs will be eliminated, though any rollback is likely to occur with a lag.

On the macro front, the key data should be October CPI (due November 13; consensus: +3.0% y/y), but the ongoing shutdown is likely to delay this release. The Senate has already failed 14 times to pass temporary funding, and the prospects for recovery from the crisis remain uncertain. Polls indicate that a majority of Americans blame the Trump administration and Republicans for the shutdown, increasing political pressure but not yet producing a compromise. The Congressional Budget Office estimates that a prolonged shutdown could weigh on Q4 GDP and add to market volatility.

Earnings season is winding down, with only 17 S&P 500 companies scheduled to report over the next week and a half. NVIDIA and Walmart will be in focus. NVDA faces elevated EPS expectations; any negative surprise could trigger sharp moves across the broader segment.

Overall, the risk balance has shifted toward caution given geopolitical and macroeconomic factors, but strong corporate earnings support a constructive backdrop. We maintain our prior forecast: the S&P 500 can reach 6,900 points by year-end and 7,500 in 2026. Besides, our stance remains balanced: elevated IT-sector multiples versus the 10-year averages reflect structurally faster growth rather than a disconnect between valuations and fundamentals.

Small Cap Stocks

Over the past two weeks, small-cap indices saw a moderate pullback: the Russell 2000 dropped 1.1%, the S&P Small Cap 600 slipped 1.2%, and the more volatile Russell Microcap index declined 2.0%. The FOMC meeting was a key driver for the segment, setting the tone for market rotation. Investors remain highly attuned to the path of policy easing, and Chair Powell’s cautious tone weighed on rate-sensitive assets.

Still, the earnings season to date has been notably strong. Nearly half of S&P Small Cap 600 constituents reported over the past two weeks. Aggregate EPS growth is running at 20.1% y/y, well ahead of the consensus (+11.2% y/y), underscoring small caps’ emergence from an earnings recession and providing a firm foundation for renewed interest in the segment.

In the weeks ahead, attention will likely remain on corporate results and macroeconomic developments. We expect market breadth to gradually widen, but we remain cautious: external shocks could still trigger short bouts of volatility.

Technical Broad Market Analysis

The S&P 500’s technical setup remains broadly positive, with the index holding within its uptrend channel. Only 5.4% of constituents currently have an RSI above 70 (overbought), compared with a 5-year average of 6.7%. Meanwhile, the proportion of companies trading above their 50-day moving average has shrunk from 53% to 40% amid rotation, a development that looks more like a temporary pause than a loss of momentum.

Expected Trading Range

We anticipate the S&P 500 index to move within a range of 6,600-6,950 points.