Investment Review №338. Change in Direction

Corporate News In Focus of Our Analysts

Alphabet, Meta Platforms, Microsoft, Amazon, Apple

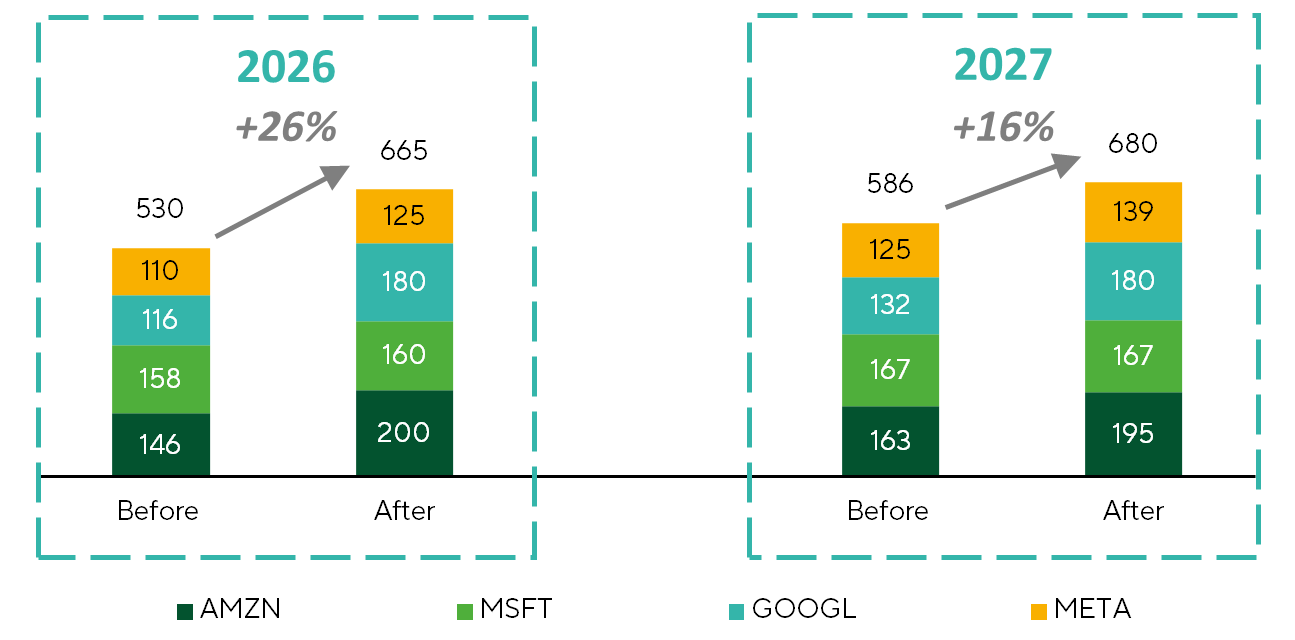

Last week’s earnings cycle for the tech titans delivered a clean story: AI demand is rock-solid, but mounting CAPEX and its returns are triggering fresh investor jitters. Alphabet (GOOGL), Meta (META), Microsoft (MSFT), Amazon (AMZN), and Apple (AAPL) all beat expectations across nearly every key financial and operational metric. Yet only Meta managed to excite the street on forward guidance, following a couple of underwhelming quarters. Across the board, capex rhetoric was uniform: relentlessAI demand, compute bottlenecks, and aggressive spend ramp-ups. While revenue and earnings beats were modest, CAPEX commitments are exploding. Following recent management commentary, 2026 and 2027 CAPEX targets are up roughly 26% and 16%, respectively. Microsoft stood out as the outlier, offering minimal CAPEX color beyond noting a heavy allocation toward internal capacity—slightly constraining Azure growth. This infrastructure-heavy messaging sets a constructive backdrop for data-center component suppliers, including Nvidia Corp. (NVDA), which reports quarterly results on February 26 after the market close.

BigTechs' CAPEX estimates before & after earnings, $ bn

Source: FactSet, Freedom Broker

Anthropic

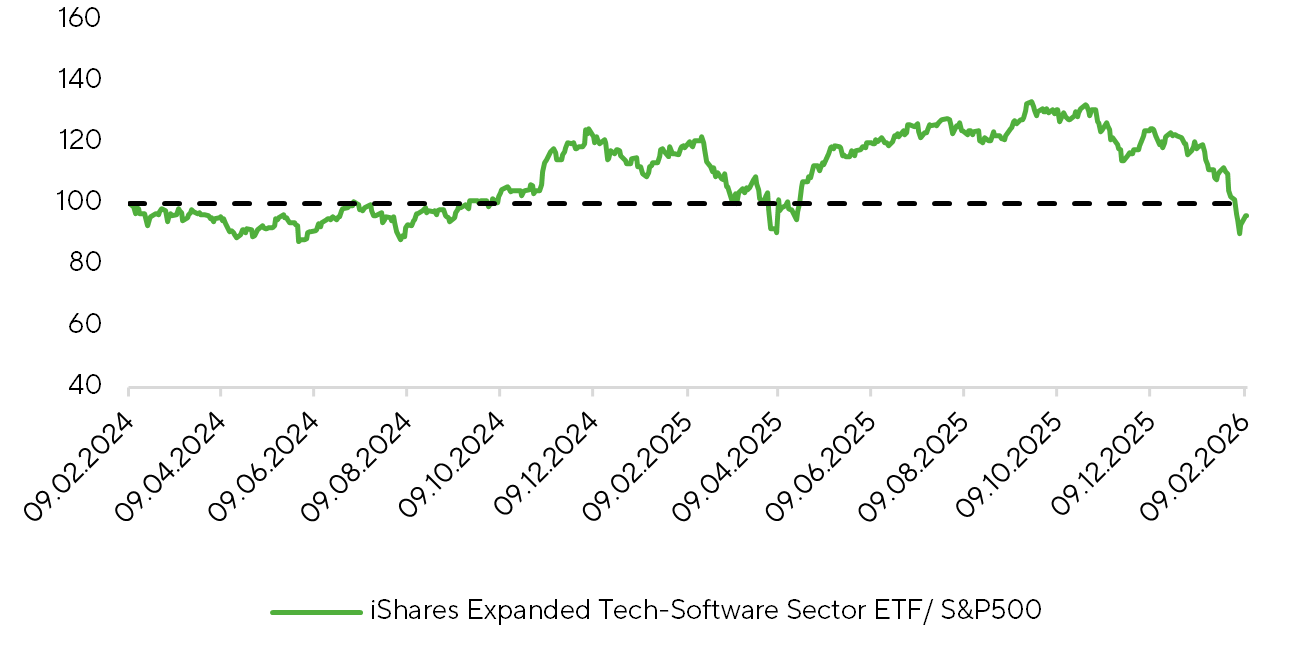

Anthropic’s latest autonomous AI agent just ripped the rug out from under software valuations. Current share price drops aren’t a routine pullback—they reflect a fundamental structural shift: the “end of the jobs-and-screens era.” Investors are waking up to the reality that the classic SaaS growth engine—tied to headcount—is breaking down. Autonomous AI can replace multiple human roles simultaneously, triggering a “job compression” effect. The implication is that clients will stop renewing redundant licenses, hitting software vendors’ revenue even if usage remains steady.

This release marks more than a product launch—it’s a marketwide reset, forcing a hard rethink of both software stock valuations and the very economics of software itself.

The outperformance of software companies relative to the S&P 500 has been erased

Source: FactSet, Freedom Broker

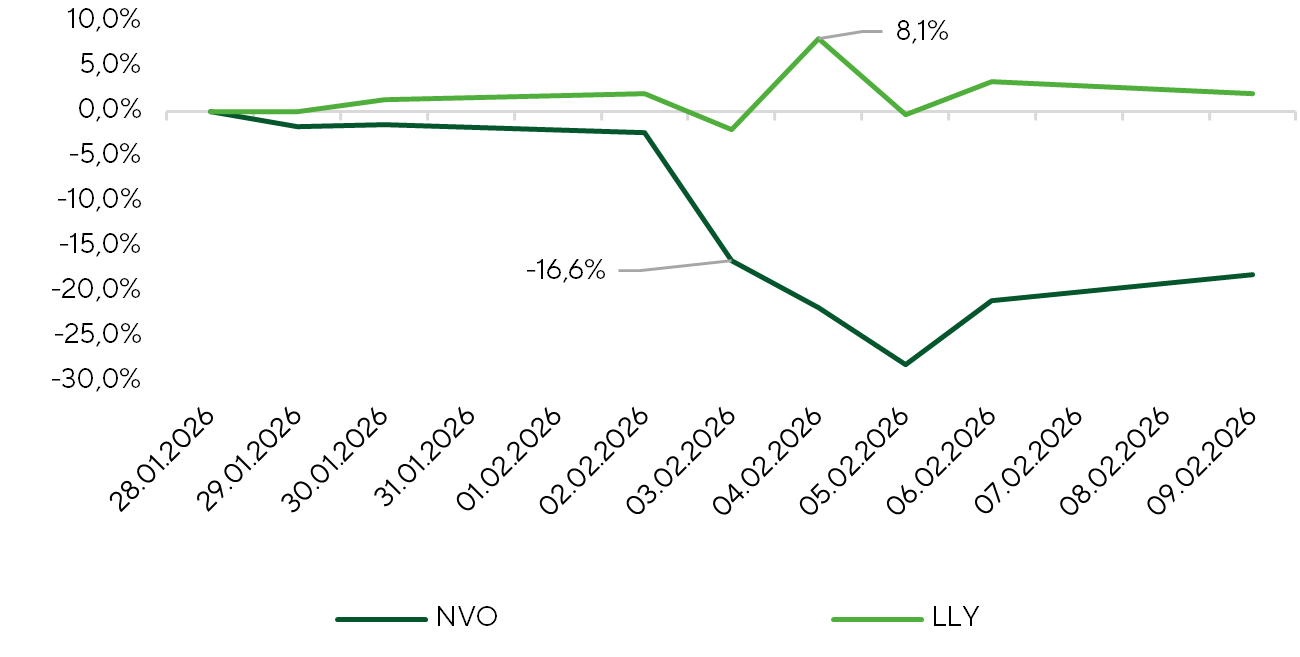

Novo Nordisk, Eli Lilly

Novo Nordisk and Eli Lilly once again delivered sharply divergent earnings trends, despite both competing in the same GLP-1 therapeutic niche. Novo Nordisk’s quarterly results beat market estimates, but management flagged signs of moderating demand, which fed into a cautious outlook. The company now guides to a roughly 5-13% decline in 2026 revenue and operating income—a negative surprise for investors who expected a stronger trajectory given the robust early sales of its oral GLP-1 products.

By contrast, Eli Lilly reported exceptionally strong results, exceeding the most optimistic market projections. The company reinforces its leadership in the GLP-1 segment, posting growth across key markets, and now guides to an about 25% revenue increase in 2026. Lilly’s GLP-1 market share expanded to 60.5%. An additional catalyst could be the expected approval of its oral GLP-1 formulation in Q2 2026, which would strengthen its long-term competitive position.

LLY and NVO Share Price Dynamics

Source: FactSet, Freedom Broker

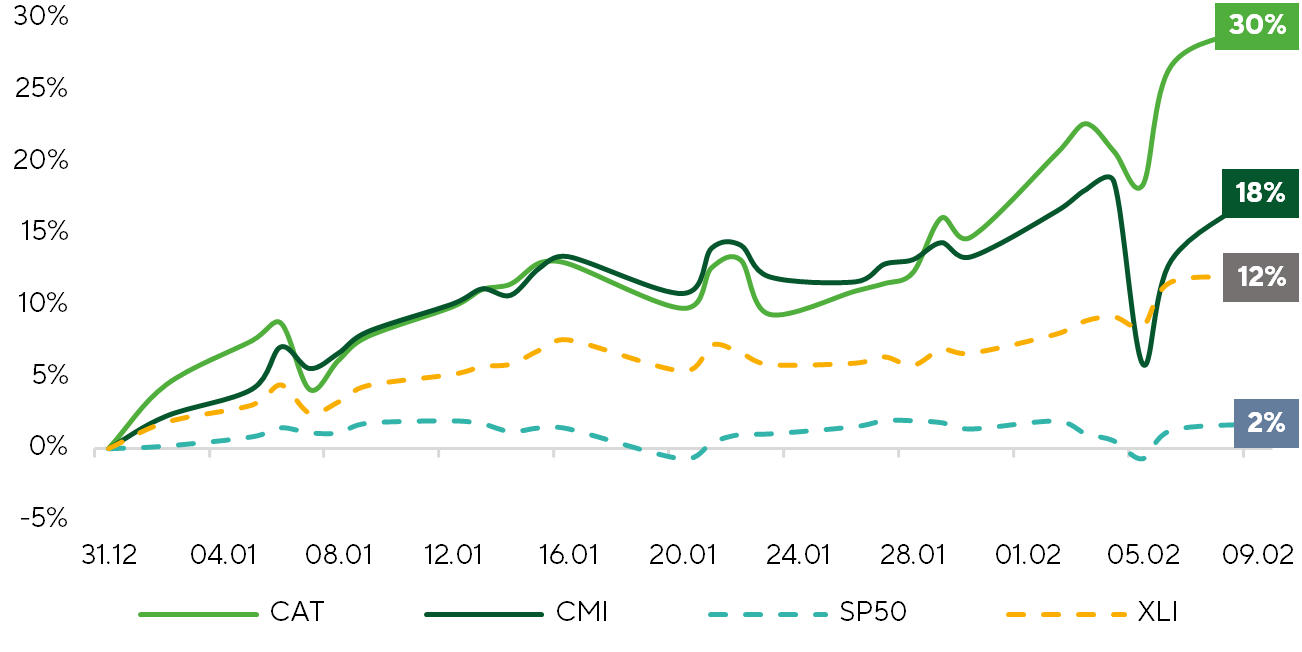

Caterpillar, Cummins

The machinery sector (XLI) is undergoing a structural shift from traditional demand cycles to a focus on energy infrastructure. Q4 FY25 results from Caterpillar (CAT: $700) and Cummins (CMI: $670) underscore this trend, with data center power infrastructure emerging as a key growth driver. These dynamics support solid top-line figures despite a broader slowdown in heavy-duty trucks.

CAT closed the year with record revenue despite tariff headwinds, delivering 18% YoY growth on robust demand for energy solutions. Cummins reported more muted results, with weakness in heavy truck engines offset by strength in power systems. Both stocks have outperformed the broader market and the XLI benchmark due to quarterly beat. With leading big techs having outlined 2026 CapEx programs, the two companies are expected to sustain strength in power‑generation equipment.

YTD Normalized Return

Source: FactSet, Freedom Broker

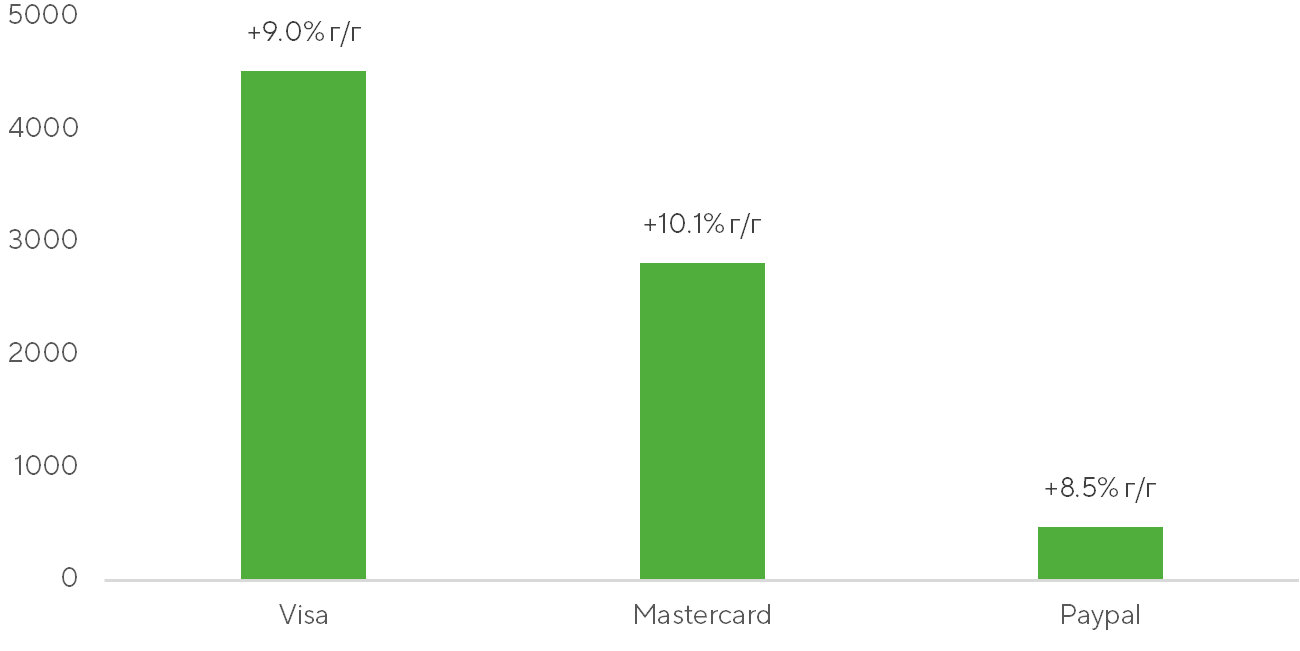

Mastercard, Visa, PayPal

Mastercard (MA) and Visa (V) underscored the resilience of their card segments, but the key sector highlight was PayPal’s (PYPL) weak quarter and an abrupt CEO change. In Q4 2025, Mastercard’s net revenue rose 18% YoY to $8.8bn, with a 57.7% operating margin and 25% growth in adjusted EPS. This performance reflected a 7% increase in gross dollar volume (GDV) on a constant-currency basis and outperformance in value-added services. Visa likewise posted double-digit growth, with revenue up 15% to $10.9bn and EPS up 15%, supported by GDV expansion (including an acceleration in the U.S.) and strong momentum across value-added and commercial solutions, though higher costs and taxes somewhat constrained margin improvement.

In this context, PayPal’s print disappointed: results were slightly below consensus, growth in high-margin branded checkout slowed, and the 2026 outlook was cautious—together driving a nearly 17% decline in the shares. The market reacted particularly sharply to the leadership change: Alex Chriss is departing after less than two years, and Enrique Lores, the longtime head of HP Inc., will take over on March 1. This accelerated transition has heightened concerns about the pace and quality of PayPal’s transformation and introduced additional uncertainty around its strategic priorities.

Total Payment Volumes

Source: corporate earnings