Investment Review №338. Change in Direction

At Full Throttle

The UAE stock exchanges showed a strong rally by the end of the first ten days of February

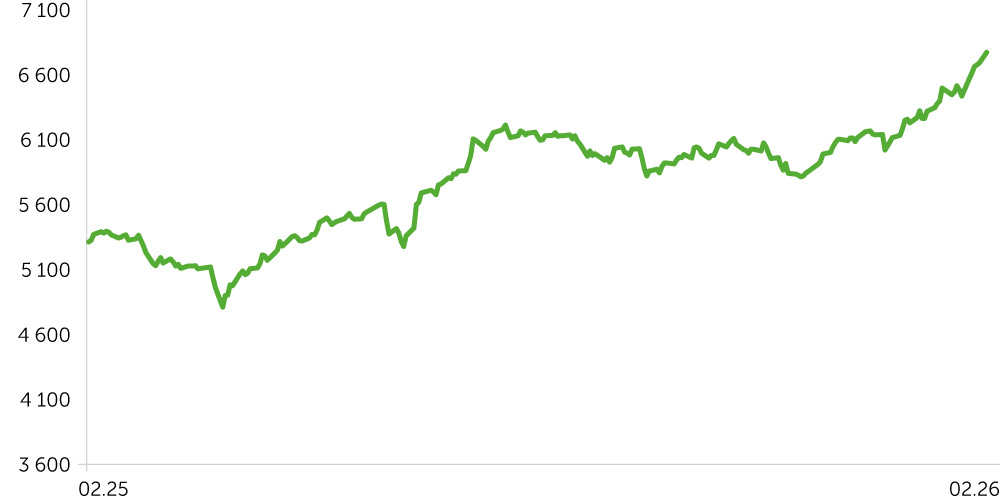

DFM General Index: 1-Year Dynamics

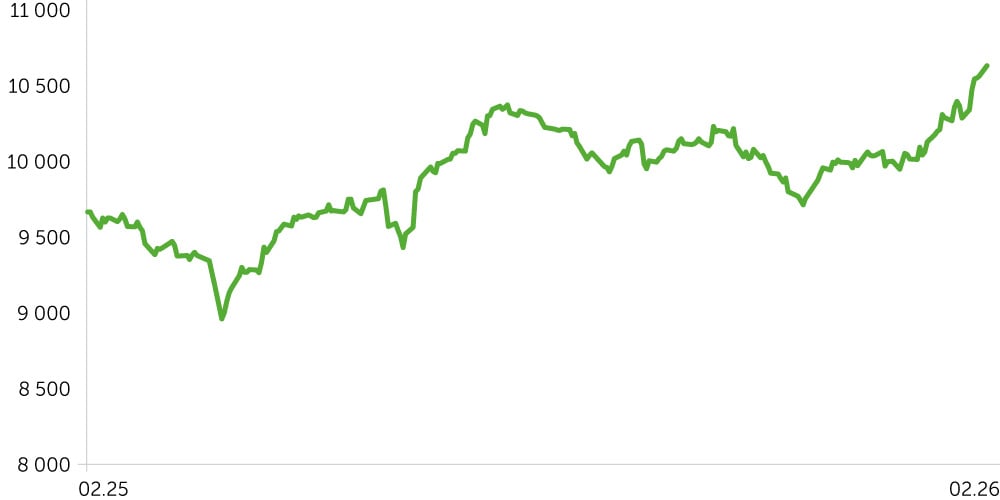

Abu Dhabi Securities Exchange Index: 1-Year Dynamics

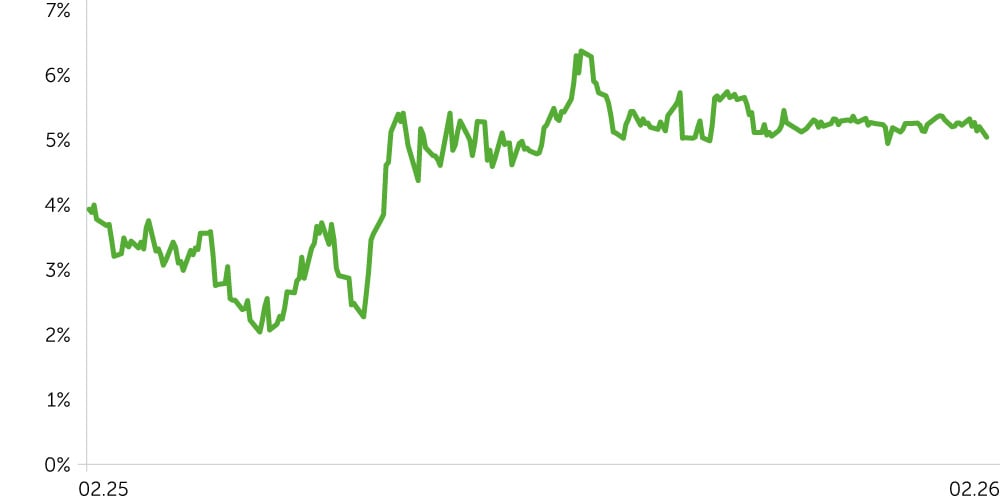

Yield, Forward Rate 1m10y, UAE, 1-Year Dynamics

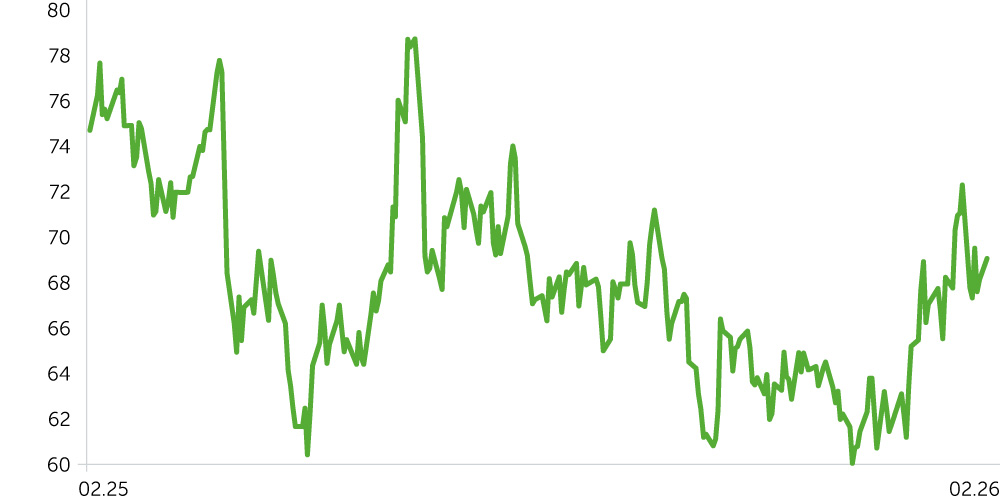

Brent Oil, 1-Year Dynamics

- The UAE equity market posted strong gains between January 26 and February 9, 2026. The DFM index rose 5.1% to 6,774 (from 6,446), and the ADI advanced 3.6% to 10,629 (from 10,264). Local benchmarks significantly outperformed the U.S. market, where the S&P 500 rose just 0.2% (to 6,965 from 6,950) over the same period. The geopolitical backdrop—ongoing uncertainty around Iran—supported Brent, which climbed 1.9% to $69 per barrel. On the macro side, Abu Dhabi’s GDP expanded 7.7% YoY in Q3 2025, driven by the non-oil sector (construction and financials).

- Sector performance was broadly positive. Real Estate led with an average return of 9.04%. The segment’s stock prices were boosted by record earnings and land‑bank expansion: Aldar Properties jumped 15.90% after reporting a 36% rise in net profit to ~$2.40bn and announcing a $10bn expansion of its JV with Dubai Holding. Emaar Properties gained 10.44% on record Dubai sales, which reached approximately $19bn in January. Consumer Discretionary stocks advanced an average 7.51%, driven by Americana Restaurants (+16.87%) due to a 38% net profit increase in 2025 and the announcement of a $201.6m dividend. Utilities added 6.12%: Abu Dhabi National Energy Co. (TAQA) was up 8.62% on demand for defensive assets and steady dividends. Financials rose an average 2.9%, with Abu Dhabi Islamic Bank (+12.99%) and Emirates NBD (+8.21%) leading after posting record full-year pre-tax profits of $2.2bn (+16%) and $8.1bn (+10%), respectively.

- The UAE sovereign proxy yield dropped 17bps to 5.02% from 5.19% in late January. By contrast, U.S. Treasury yields were little changed, edging down 3bps to 4.33%. As a result, the UAE-U.S. yield spread narrowed to 69bps, reflecting stronger liquidity and rising investor confidence in the Emirati financial system. Notably, the UAE imports the Fed’s monetary policy, so fluctuations around the long-term average are to be expected.

Economic Updates

- Abu Dhabi’s economy remains resilient. SCAD data released on February 9 showed 7.7% GDP growth in Q3 2025. The non-oil economy (+7.6% YoY), which continues to be the key driver, now accounts for 54% of total GDP. Construction (+13.9%) and real estate (+13.1%) recorded the fastest growth rates.

- 2026 GDP growth outlook. Early‑February reports from the World Bank and BMI (Fitch Solutions) revised the UAE 2026 growth forecast up to 5.0-5.6%, supported by recovering OPEC+ oil production and strong non‑oil momentum.

- Record non‑oil trade. On February 1, 2026, authorities announced the UAE’s non‑oil foreign trade reached a record $1.03tn, highlighting the success of the country’s diversification strategy.

- Monetary policy. The Central Bank of the UAE (CBUAE) kept its base rate unchanged at 3.65%, in line with the U.S. Fed’s decision. The central bank also unveiled a new symbol for the national currency and launched a platform for issuing digital bonds, enhancing the market’s technological appeal.

- The Abu Dhabi emirate has consolidated the state holding ADQ into a new sovereign fund, L’imad, with total assets of $263bn. L’imad’s portfolio includes Abu Dhabi’s strategic assets in infrastructure, energy, logistics, finance, and industry, previously spread across several entities. The fund is headed by Crown Prince Sheikh Khaled bin Mohamed Al Nahyan, formalizing his role as a key overseer of government investment strategy. The restructuring is designed to improve coordination among the emirate’s sovereign funds—including Mubadala and ADIA—and to increase decision‑making flexibility under a single capital center.

Corporate News

- Aldar Properties: the company delivered exceptional 2025 results, with revenue of ~$6.27bn and net profit up 36% YoY to $2.40bn. The backlog closed at a record ~$45.5bn, including government contracts, providing strong visibility and a stable revenue trajectory over the next 3-5 years.

- Americana Restaurants: the region’s leading Food & Beverages operator reported full-year revenue up 11% to $2.51bn, with net income surging 38% YoY to $219.1m. The board declared a dividend totaling $201.6m (~$0.024 per share). The company also expanded its network, opening 159 new restaurants during the year.

- Emirates NBD: the bank reported a record pre-tax profit of more than $8.1bn, up 10% YoY. The Board of Directors has proposed a dividend of around $0.272 per share. Strong results were driven by loan portfolio growth and expansion in India after securing an investment banking license.

- Abu Dhabi Islamic Bank (ADIB): net earnings rose 16% to $1.93bn after tax. The bank declared a dividend of ~$0.264 per share (50% of earnings). With ROE at 29%, it remains one of the region’s best-performing banks.

Two-Week Outlook

The likelihood of a U.S. or Israeli strike on Iranian military targets overnight on February 13-14 has risen meaningfully amid stalled negotiations and a buildup of regional military assets. The coming weekend could prove tactically opportune, with U.S. equity markets closed on Monday, February 16, for the Presidents’ Day holiday.

The Iran overhang injects considerable uncertainty into the near-term path of oil prices. The onset of military action would likely trigger a short-lived risk premium.

Technically, the UAE market is signaling a decisive trend reversal. The DFM has reclaimed its 50- and 200-day moving averages and fully retraced January’s geopolitically driven pullback. The index is in an active upswing and is tracking toward the 6,800 psychological level.

The ADI also retains a constructive, bullish bias, trading above key moving averages. That said, RSI readings on both indices are approaching overbought territory (above 75), which could prompt a brief technical pullback or consolidation in the nearest sessions before the uptrend resumes.