Investment Review №339. Playing Defense

Review as of February 24

Global Perspective

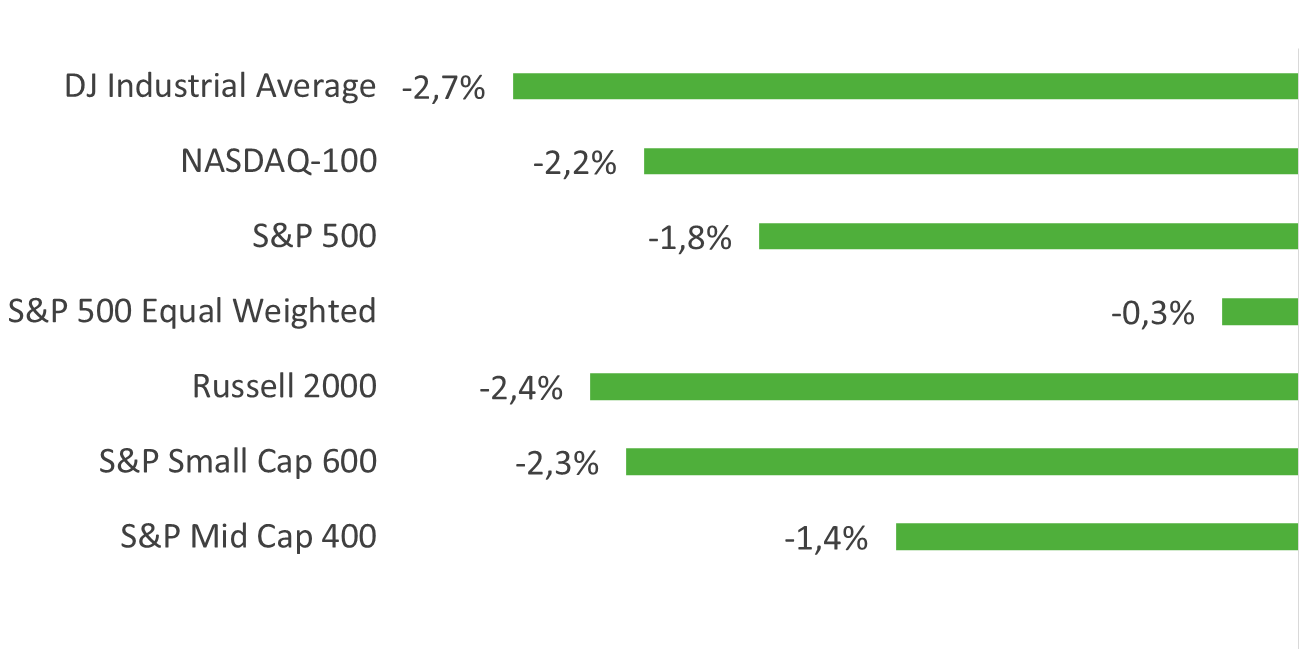

Over the past two weeks, the previously broadening rally has paused, with markets entering a phase of moderate correction amid elevated volatility. Major U.S. benchmarks finished the period in the red: the S&P 500 fell 1.8%, the Nasdaq-100 declined 2.2%, and the Dow Jones Industrial Average underperformed, down 2.8%. Notably, the equal-weighted S&P 500 showed greater resilience than traditional cap-weighted indices, suggesting that underlying market breadth has remained relatively healthy despite the pullback. Small- and mid-cap equity segments also faced pressure. The Russell 2000 dropped 2.3%, while the S&P MidCap 400 fell 1.4%, reinforcing the narrative of a broad cooling in risk appetite.

Benchmark Index Performance Over the Two-Week Period

Source: FactSet, Freedom Broker

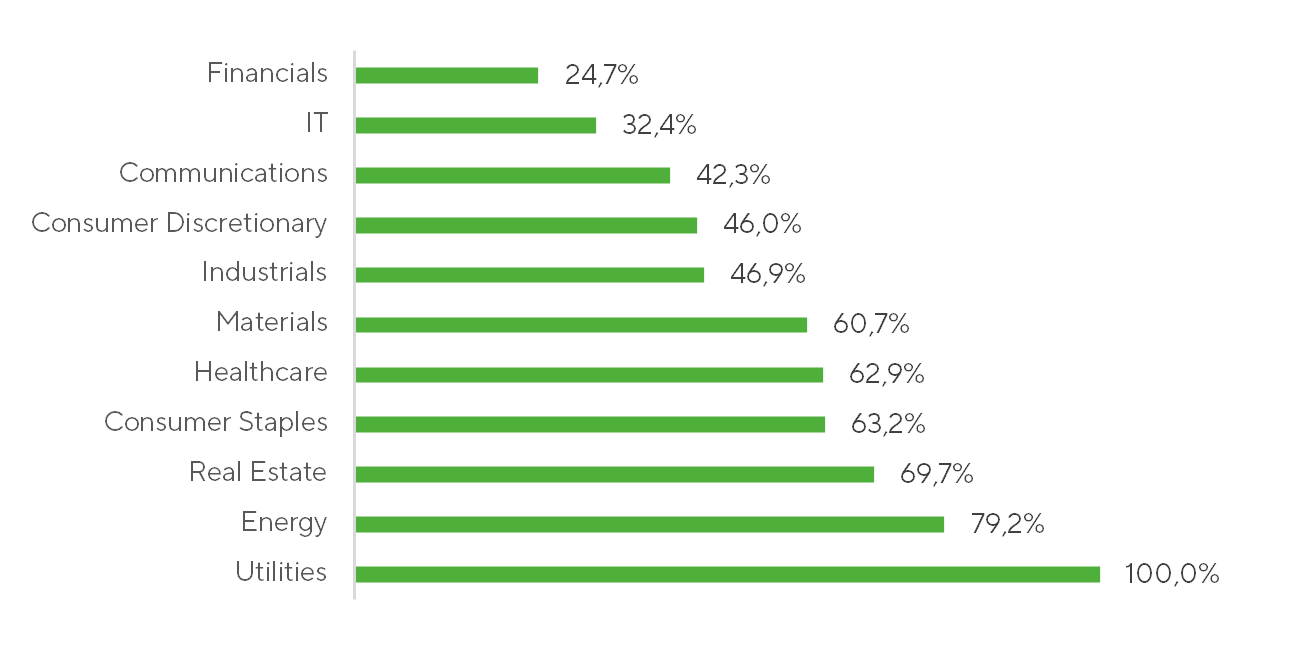

The internal “quiet rotation” hasn’t stopped — it has simply redirected. Fewer than half of stocks advanced across the major indices: 49.6% in the S&P 500, 43.1% in the Nasdaq-100, and just 33.6% in the Russell 2000. Beneath the surface, performance diverged sharply by sector. Defensives dominated. Utilities had 100% of constituents in positive territory, Energy 79.2%, and Real Estate 69.7%. In absolute terms, Utilities surged 7.0%, with Real Estate up 3.5%. These sectors combine stable cash flows and low volatility with high-rate sensitivity due to leverage. Yet rate expectations barely moved over the period, indicating the shift was not policy-driven. Instead, capital rotated into lower-beta assets as uncertainty rose.

Market Breadth: Share of Companies with Positive Returns

Sources: FactSet, Freedom Broker

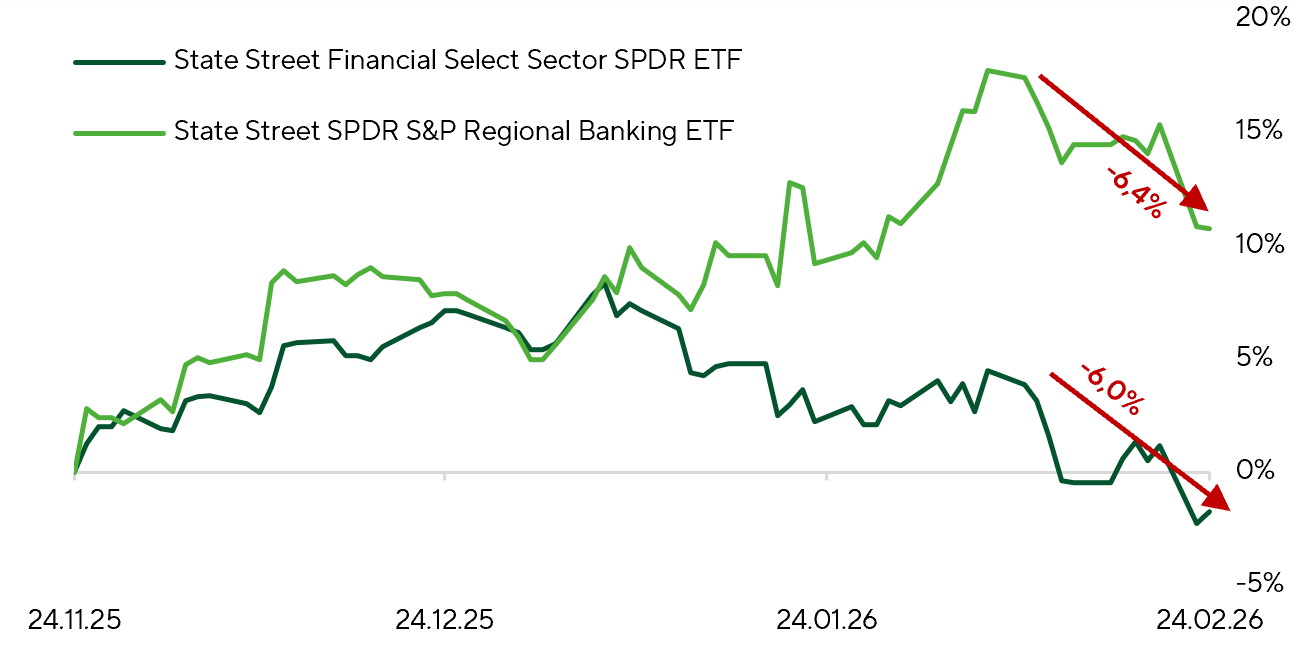

Financials showed the weakest breadth, with pressure concentrated in large-cap banks. The sector had already been lagging since the start of the year, but the pullback has accelerated notably in recent weeks. Investors are still searching for a clear catalyst behind the deterioration in sentiment. In our view, part of the weakness reflects the broader AI narrative. While tangible fundamental risks to banks remain limited for now, uncertainty over how AI could reshape financial services, lending models, and competitive dynamics is adding a layer of caution and psychological overhang.

Normalized Returns of Large Financials (XLF) and Regional Banks (KRE) Over the Past Three Months

Source: FactSet, Freedom Broker

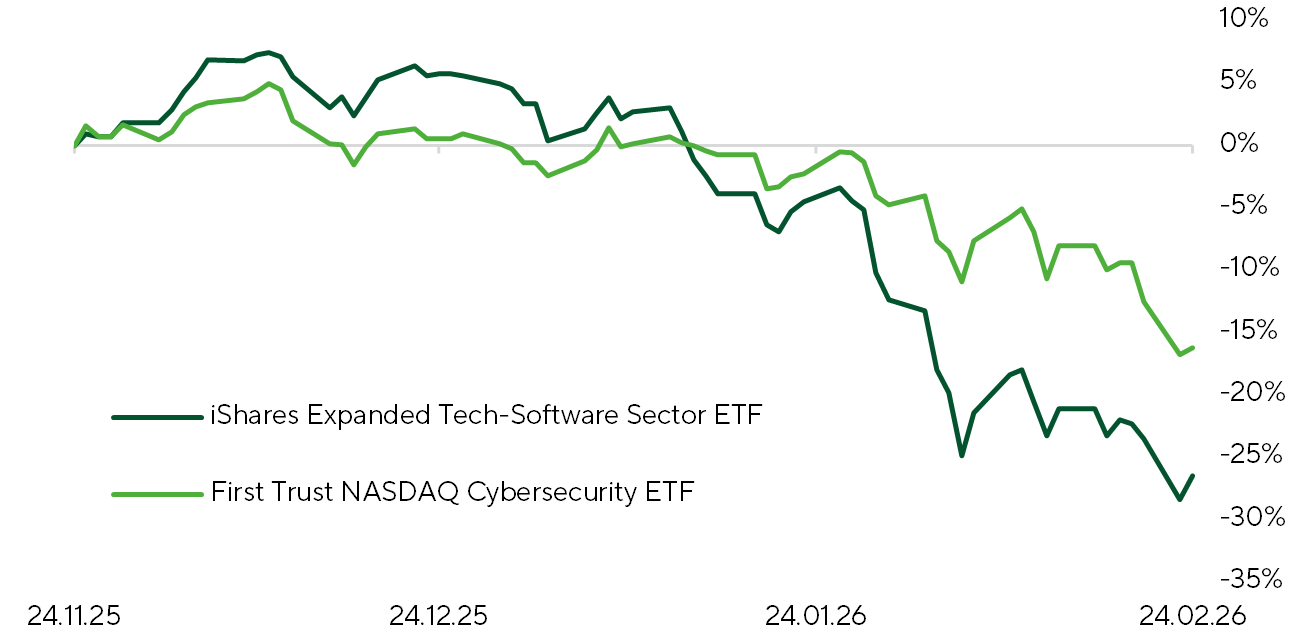

IT has also emerged as a clear laggard. In early February, software stocks became ground zero for a sharp selloff after headlines about new tools from Anthropic reignited fears that AI agents could begin displacing traditional software functions. We have tentatively characterized this shift as the “end of the jobs-and-screens era,” as investors started to question whether the SaaS model — long a core growth engine for the sector — could face structural pricing pressure from increasingly autonomous AI. The correction has continued over the past two weeks. The iShares Expanded Tech-Software Sector ETF has fallen another 7.8%, taking its year-to-date decline to roughly 25.8%.

Cybersecurity has also come under pressure following the launch of Anthropic’s Claude Code Security product, which triggered broad selling across the space. The First Trust NASDAQ Cybersecurity ETF dropped 9.9% over the same period. We believe the drawdown may be opening selective long-term opportunities, but the medium-term outlook will hinge on how quickly AI-native security capabilities from players such as Anthropic and OpenAI evolve. Ahead of earnings, we reiterate Buy ratings on CrowdStrike (CRWD) with a $550 price target and on Zscaler (ZS) with a $320 target. In our view, the market reaction rests on an oversimplified premise that AI capable of scanning code for vulnerabilities renders traditional cybersecurity obsolete. In practice, many of the most damaging attacks (credential theft, phishing, insider activity, or DDoS) bypass code quality altogether. At the same time, AI-accelerated development is likely to drive explosive growth in applications and cloud workloads, expanding the attack surface and sustaining demand for specialized security platforms.

Normalized Performance of Software (IGV) and Cybersecurity (CIBR) Segments Over the Past Three Months

Source: FactSet, Freedom Broker

The political backdrop remained intense. On February 20, the U.S. Supreme Court ruled that tariffs imposed under IEEPA were unlawful, stressing that the authority to levy duties lies with Congress and that the power to “regulate imports” does not automatically include the power to tax them. The decision applies only to IEEPA-based tariffs; the issue of refunding previously collected revenues (about $170 billion) will be handled through administrative channels. In response, Donald Trump announced new tariffs under Section 122 of the Trade Act, initially set at 10% with the option to increase them to 15% for up to 150 days, while maintaining USMCA exemptions. The removal of IEEPA tariffs lowers the effective rate from 13.6% to roughly 6%, but the new measures push it back into the 10–12% range. From a market standpoint, the net effect appears broadly neutral. Tariff risks were already largely priced in, and the economy has begun to adapt. The primary impact is likely to be higher short-term volatility and elevated political uncertainty rather than a structural shift in market dynamics.

On the macro front, the period featured several key releases, including the January employment report, inflation data, and the advance estimate of Q4 2025 GDP. Labor-market conditions remained solid. The unemployment rate fell to 4.28% versus expectations of 4.4%, underscoring resilient hiring despite a more accommodative policy backdrop. Inflation also surprised to the downside: headline CPI rose 0.17% MoM vs. a 0.3% consensus, while core CPI (excluding food and energy) increased 0.29% MoM. On a year-over-year basis, inflation stood at 2.4%, with core at 2.5%, reinforcing the ongoing disinflation trend.

The advance estimate of Q4 GDP came in weaker than expected at 1.4% annualized vs. forecasts near 2.8–3.0%, largely reflecting a drop in government spending during the shutdown. We view this as a temporary drag and, all else equal, continue to see the economy operating in a “Goldilocks” regime in the first half of 2026.

Market Focus

Geopolitics remains the market’s primary swing factor and a key driver of positioning. Energy continues to price in a growing risk premium. The Energy Select Sector SPDR Fund is up more than 23% year to date and, despite a modest two-week pause (+2.0%), remains the top-performing sector of 2026. This strength stands out given weak 4Q25 earnings across the industry and a persistent global oil surplus. Crude prices are reflecting the same dynamic. WTI has risen more than 15% year to date, largely on escalating conflict risk.

Prediction markets reinforce that view. Polymarket currently assigns a 60% probability to a direct U.S.–Iran confrontation by end-March (up from 41%) and 68% by end-June (up from 55%). The repricing has been rapid, with some market participants anticipating potential U.S. strikes within weeks. Market outcomes will depend heavily on the nature of any escalation. A limited strike focused on military assets or leadership would likely produce a short-lived spike in oil followed by stabilization, with minimal spillover to broader risk assets. By contrast, damage to Iran’s oil and gas infrastructure, retaliation against regional producers such as Saudi Arabia or the UAE, or disruption of shipping through the Strait of Hormuz could push WTI above $100 per barrel. Such a scenario would likely re-ignite inflation concerns, weigh on global growth, and trigger a broader equity selloff.

We see little strategic incentive for the U.S. or Israel to target energy infrastructure directly, making Tehran’s response the key uncertainty. Even in an escalation scenario, Washington would likely seek to limit a sustained oil price spike. Duration is critical. A short, contained conflict would materially reduce the risk of lasting macro or market damage, while a prolonged disruption would carry significantly higher downside for both growth and risk assets. We view the military buildup in the region as consistent with a scenario of a rapid, time-limited strike aimed at achieving strategic objectives while avoiding major disruption to energy markets.

Another dominant theme is the evolution of the AI narrative. Investors are increasingly focused on the risk of structural disruption to established business models, with pressure now visible beyond IT and extending into Financials. Any signals about AI’s impact on corporate earnings are being scrutinized cautiously. In this context, upcoming reports from CrowdStrike Holdings, Inc. and Broadcom Inc. carry outsized importance, offering perspectives from software and hardware sides of the AI ecosystem.

CrowdStrike (CRWD) reports March 3. The stock is down roughly 20% over the past month amid the AI-driven selloff in cybersecurity. While Anthropic’s Claude Code Security release triggered sector-wide panic, we expect the net impact of generative tools on CrowdStrike’s long-term revenue trajectory to be neutral to positive. These technologies do not replace the company’s core platform; instead, they escalate the cyber arms race and should drive incremental demand for comprehensive protection. Consensus expects revenue of about $1.29–1.30 billion and adjusted EPS near $1.10. For SaaS companies, however, annual recurring revenue remains the key indicator. If net new ARR proves resilient despite macro headwinds, the stock could respond quickly. Management’s fiscal-2027 outlook will be the primary catalyst. Given the recent drawdown, expectations appear conservative, leaving room for a short-covering rally if pipeline momentum improves. Our 12-month price target for CRWD is $550.

Broadcom (AVGO) reports March 4 and will provide a read-through on AI infrastructure demand. Recent results from key customers, including Alphabet and Meta on custom AI silicon and Microsoft and Amazon on networking equipment, point to continued aggressive capital spending. Taiwan Semiconductor Manufacturing Company has likewise raised industry growth forecasts and accelerated capacity investment. Media speculation about a potential loss of Broadcom’s Google TPU program appears overstated in our view. Google’s internal efforts remain behind schedule, and Broadcom has already secured the contract for the next TPU generation. The company also continues to develop custom solutions for major hyperscalers, including OpenAI and Meta. After the recent correction, AVGO shares appear oversold and positioned for recovery; our speculative two-month target is $379.

On the macro side, attention will shift to February labor-market data (March 6) and CPI inflation (March 11). January releases indicated continued disinflation alongside resilient employment. For now, macro factors are taking a back seat to geopolitics and the reassessment of technology sector risks. If upcoming data broadly match consensus expectations, the market response is likely to be limited.

Broad Market Technical Analysis

In February, the S&P 500 tested the 6,780–6,800 support zone twice and rebounded, holding above its 100-day moving average, currently near 6,830. The index has not closed below this level since May 2025, reinforcing its importance as a key dynamic support. RSI remains slightly above the neutral 50 level, pointing to consolidation rather than a clear directional trend. Our base case calls for a renewed push toward 7,000 and higher. That said, breadth has softened somewhat, with the share of stocks trading above their 200-day moving average slipping to about 63–64% from 65–67%. A decisive break below 6,720 would tilt the risk balance to the downside.

Expected Trading Range

We expect the S&P 500 to trade within a 6,720–7,050 range.