Investment Review №344. A Commitment to Techno-Optimism

In a State of Fluctuation

The Turbulent External Environment Has Led to Mixed Performance Among the UAE's Sector Indices

DFM General Index: 1-Year Dynamics

Abu Dhabi Securities Exchange Index: 1-Year Dynamics

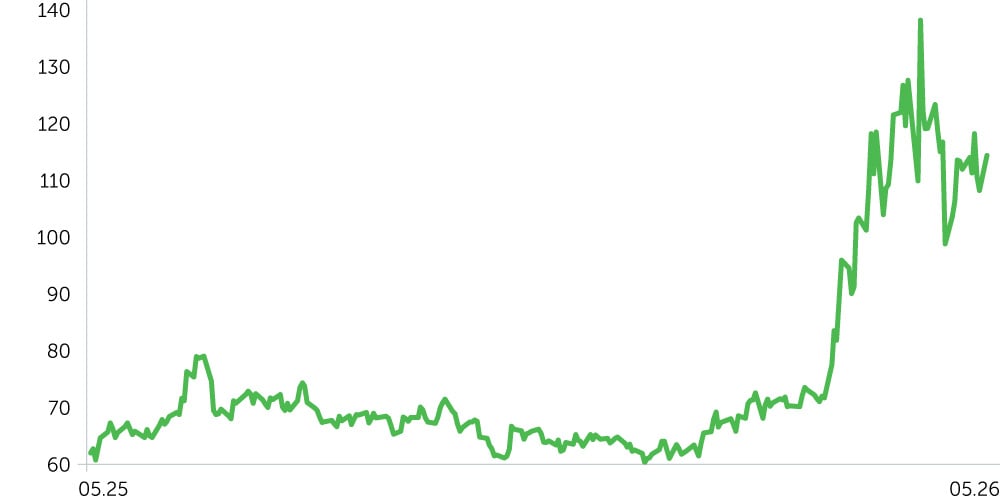

Yield, Forward Rate 1m10y, UAE, 1-Year Dynamics

Brent Oil, 1-Year Dynamics

Between April 20 and May 4 2026, UAE equities traded mixed. The DFM Index declined 1.4%, falling from 5,862 to 5,780, while the ADX Index eased 0.2% from 9,842 to 9,821. By comparison, the S&P 500 advanced 1.3%, while Brent surged 10.5% from $103/bbl to $114/bbl. Oil prices were supported by Donald Trump’s comments signaling willingness to maintain the blockade of Iranian ports, alongside rising discussion of potential military escalation scenarios. The relatively weak performance of local benchmarks despite the sharp move higher in crude suggests profit-taking in the most liquid UAE names following the strong rebound seen in early April, while elevated commodity prices continued to underpin selective interest in energy-linked equities. May 4 marked a renewed escalation in the regional conflict. The UAE reported intercepting multiple missiles and drones, alongside a fire incident in Fujairah. Markets responded with an immediate risk-off move: in the first trading session following the attacks, the DFM Index fell 0.9% to 5,729, while the ADX Index declined 0.3% to 9,791. Brent’s concurrent rally further reinforced how even short-lived escalation episodes continue to feed directly into UAE risk pricing and sector rotation dynamics.

Sector performance was uneven. Energy was the clear outperformer over the two-week period, delivering average returns of +9.4%: ADNOC Drilling rallied 22.48%, ADNOC Gas gained 6.27%, while Dana Gas lagged, declining 4.55%. The sector was supported by Brent’s rally to $114/bbl by May 4, alongside growing market focus on the UAE’s potential oil production expansion and the associated long-term CapEx opportunity set across upstream and midstream assets. Consumer staples was the weakest-performing sector, posting average returns of -5.56%: Agthia Group declined 4.30%, while Spinneys 1961 Holding fell 6.45%. The move points to mounting pressure on defensive consumer names amid capital rotation into more cyclical segments and rising geopolitical volatility, with investors during the period prioritizing liquidity and near-term earnings catalysts. Real estate also came under pressure, with the sector posting average returns of -3.12%: Emaar Properties declined 5.06%, Emaar Development fell 4.74%, and Aldar dropped 6.29%. The pullback reflects a cooling phase following the sector’s earlier rally, despite still-supportive fundamentals in Dubai’s residential market. Financials delivered average returns of -1.3%, although performance dispersion within the sector was significant. ADCB gained 8.53% and Ajman Bank advanced 2.13%, while ADIB declined 11.66%, Emirates NBD fell 5.76%, and FAB lost 4.66%.

UAE sovereign proxy yields compressed to 4.30% from 4.82%, while 10Y U.S. Treasuries climbed to 4.50% from 4.39%. The UAE-U.S. spread compressed to -20bps, reflecting a narrowing regional risk premium amid improving external sentiment and sustained demand for Middle Eastern fixed-income assets.

Economic Updates

- Corporate news flow remained a key driver of local market performance during the period. UAE equities were supported by strong quarterly earnings, most notably from ADCB, where both net interest income and bottom-line profit materially outperformed broader sector trends. The results reinforced that, for large-cap banks, investor focus remains centered on earnings quality and margin resilience rather than purely on the direction of interest rates.

- According to Dubai Financial Market data released on April 30, net profit rose 43% YoY in Q1 2026. Beyond DFM itself, the result serves as a proxy for sustained capital market activity in Dubai, underscoring continued momentum following a strong start to the year and persistent retail and institutional participation in local equities.

- UAE announced its exit from OPEC/OPEC+ effective May 1, keeping the country’s oil strategy firmly in global investor focus. The move represents a material hit to OPEC/OPEC+ market influence: UAE output stood at ~3.4m bpd in February 2026, equivalent to 11.9% of total OPEC production and 8.0% of OPEC+ output. Post-exit, OPEC+ share of global oil supply is set to decline from ~42% to ~39% (Feb 2026 basis). Earlier, UAE authorities indicated an ambition to raise production capacity toward ~5m bpd. Against this backdrop, the country’s exit from OPEC+ increases medium-term upside risk to global supply growth while structurally weakening the group’s ability to manage market balance. For local equities, the implication is broadly supportive for oilfield services and energy infrastructure names, while potentially capping oil price upside over the medium term. Meanwhile, OPEC+ continued to loosen output constraints. At the May 3 meeting, the group agreed to raise June quotas by 188k bpd, following prior increases of 206k bpd in April and May. At the current pace, cumulative quota hikes could extend through September 2026, implying a total increase of ~1.16m bpd.

Corporate News

- First Abu Dhabi Bank (ADX: FAB). FAB reported Q1 2026 net profit of $1.4bn, beating consensus at $1.2bn, despite a modest YoY decline off a high base. The print reinforces its defensive status as the UAE’s largest bank, demonstrating continued ability to outperform expectations even in a more volatile external backdrop, thereby limiting downside risk to sector multiples.

- Abu Dhabi Commercial Bank (ADX: ADCB). Net profit rose 37% YoY to $0.9bn in Q1, while operating income increased 18% YoY. Against this backdrop, ADCB emerged as one of the top performers among large-cap banks over a 2-week horizon, up 8.53%, consistent with a positive market read-through on strong results and likely reflecting expectations of further earnings upside alongside sustained asset quality strength.

- Emirates Telecommunications Group / e& (ADX: EAND). Q1 2026 consolidated revenue rose to $5.3bn (+15.1% YoY), with EBITDA reaching $2.3bn (+16.5% YoY). For the UAE’s largest telecom operator, this reinforces a shifting investment case—beyond the traditional defensive domestic business toward scaling international and digital assets. The 2-week share performance remained muted, with the Communication Services sector up just 0.66%.

- Emaar Properties / Emaar Development (DFM: EMAAR / EMAARDEV). Despite a 2-week pullback in share prices, the fundamental backdrop for Dubai’s flagship developers remains robust. The National, citing Dubai Land Department, reported Q1 Dubai property transaction value at $68.7bn (+31% YoY), with 60,303 deals (+6% YoY), while foreign investment rose 26% to $40.4bn. For Emaar, this signals continued strength in premium and off-plan demand conditions, even as near-term equity performance appears driven more by capital rotation out of real estate into energy names than by any deterioration in operating fundamentals.

Two-Week Outlook

Oil markets remain in a high-uncertainty regime, with price action increasingly anchored to developments around the Strait of Hormuz. A renewed military escalation would likely trigger a further upside spike in crude, while de-escalation would imply a sharp correction lower. In a sustained “dual blockade” scenario involving both U.S. and Iran positioning around the Strait of Hormuz, the base case shifts toward a gradual grind higher in oil prices.

On the near-term horizon, UAE markets will remain primarily driven by a combination of three key factors: the trajectory of oil prices, the strength of corporate earnings from large-cap benchmarks, and the pace of further normalization in local risk premia across asset classes.

In the base case, strong earnings momentum from leading UAE banks, alongside sustained high turnover in Dubai real estate, should continue to support demand in UAE large caps, while energy names are likely to remain relative outperformers as long as Brent holds near current levels. In a more cautious scenario, an upside move in global yields or a reversal in oil prices would likely trigger a rotation into defensive names and drive further index consolidation following April’s elevated volatility.