Двухнедельный обзор фондовых рынков №348. Сезонная рокировка

Improved Macro Outlook Supports Local Assets

Improving macroeconomic data and forecasts are sustaining investor interest in local assets

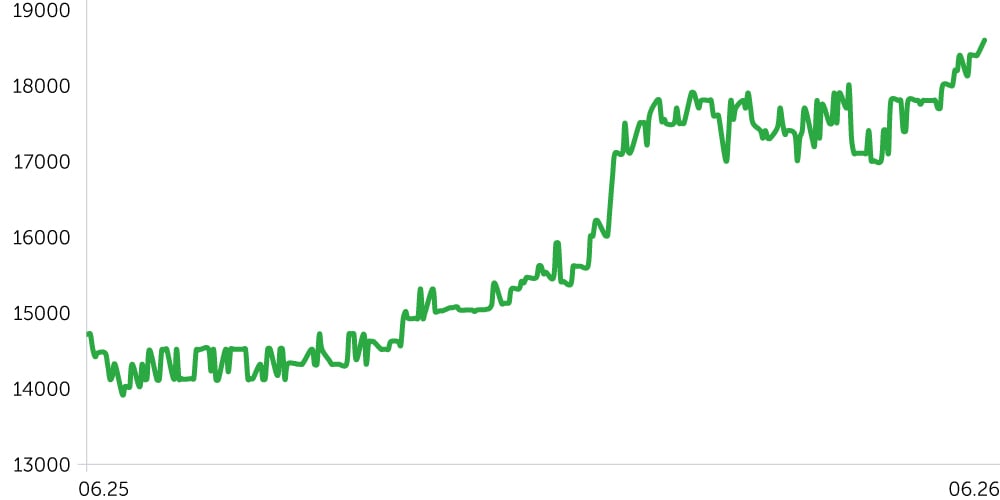

Telecom Armenia Stock Performance (Post-IPO)

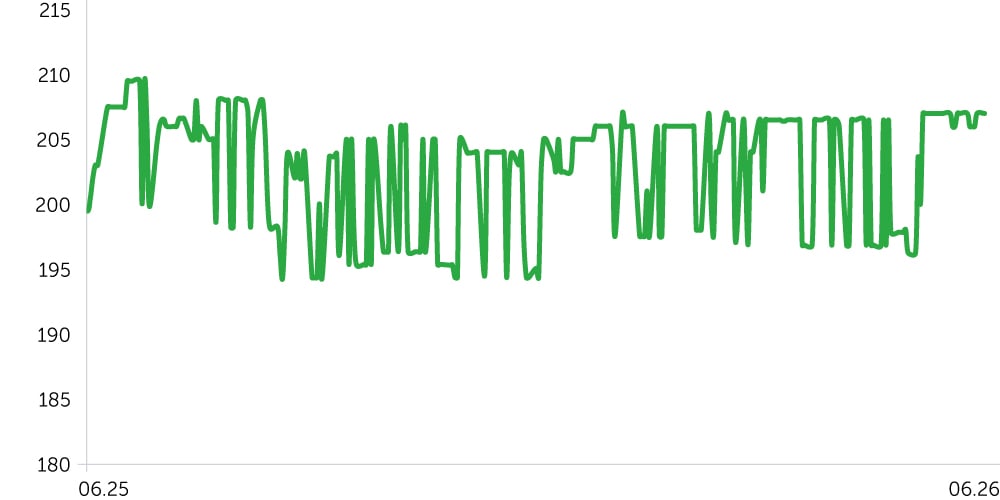

ACBA Bank: 1-Year Stock Trends

USD/AMD: 1-Year Dynamics

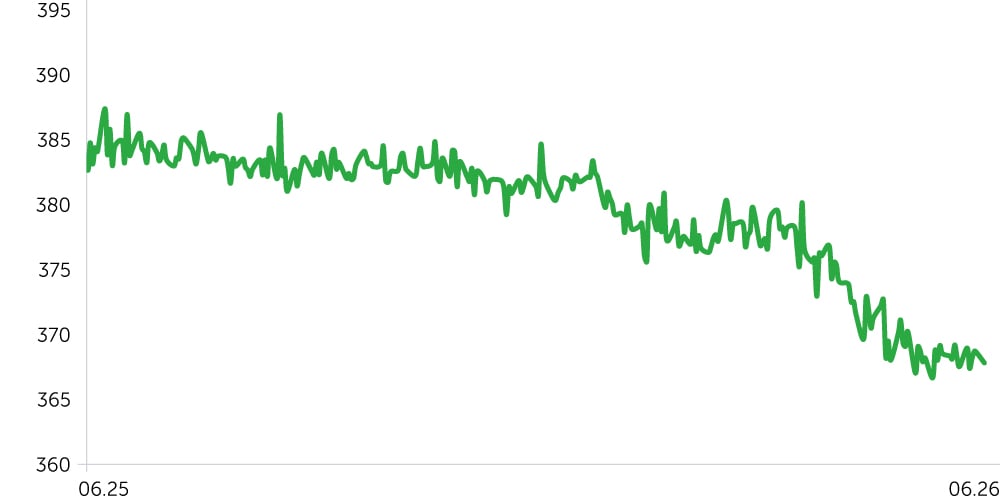

3-Year Corporate Bond Index (AMD) – Post-Update

Between June 1 and 15, 2026, the Armenian market delivered mixed performance. Telecom Armenia (AMTL) was unchanged, consolidating recent gains (+5.5% over the prior month), while ACBA Bank (ACBA) rose 3.3%, continuing to outperform the market. Sentiment was likely supported by May’s inflation slowdown and favorable geopolitical developments in the Middle East, which together, in our view, materially reduced the likelihood of a rate hike at the Central Bank’s next meeting. Another supportive factor was the World Bank’s upward revision to its 2026 GDP growth forecast for Armenia, despite an expected slowdown in Europe and Central Asia—underscoring the resilience of domestic demand. In addition, May data indicate a notable pickup in liquidity and trading volumes across both equity and bond markets, a constructive sign for the local market overall.

Meanwhile, the debt market saw a modest pullback: the 3Y Corp Bonds Index declined 0.8%, likely reflecting profit-taking after the prior rally and greater caution amid heightened external inflation risks—most notably elevated oil prices over the period. The dram’s stable exchange rate against the U.S. dollar likely helped anchor market sentiment. Looking ahead, Russian restrictions on imports of certain Armenian goods could introduce additional volatility. Given Russia’s importance as an export destination, any decline in FX inflows could increase market volatility and exert some medium-term pressure on the dram.

Economic Updates

From June 1 to 15, 2026, macro data releases were limited. In this context, market participants focused on two themes: signs of disinflation and Armenia’s parliamentary elections, which could materially shape expectations for foreign and domestic economic policy—and, by extension, market dynamics.

- Inflation in Armenia moderated to 4.2% YoY in May (after surging to 5.3% in April), placing it just above the upper bound of the Central Bank’s target band (3% ± 1 pp). The key driver was a decline in food prices (-2.3% MoM), although food inflation remained elevated on a yearly basis (+6.4% YoY). Non‑food prices rose moderately (+0.5% MoM; +2.1% YoY), while services increased +0.2% MoM and +2.7% YoY. In our view, the data meaningfully reduce the probability of a near-term refinancing-rate hike and support a wait-and-see stance from the Central Bank. Moreover, the recent easing in Iran–U.S. tensions and the potential reopening of trade routes after the anticipated memorandum is signed—factors that have already resulted in softer oil prices—should be disinflationary for Armenia. However, any disinflationary effect from recently introduced Russian trade restrictions is expected to be relatively short-lived.

- The World Bank raised its GDP growth forecast for Armenia to 5.3% in 2026 (from 4.9% in January), 5.1% in 2027, and 5.0% in 2028. This upgrade stands out against a projected slowdown to 2.1% for the Europe and Central Asia region in 2026 and a weaker global outlook of 2.5% amid ongoing conflict in the Middle East. The Bank also flags risks for energy‑importing economies given higher oil price assumptions—particularly highly import-dependent economies such as Armenia. Overall, we see the revision as an affirmation of domestic growth resilience and a modestly positive signal for the market.

- Armenia’s equity market capitalization rose 27.4% in May to above AMD 478.8bn (~$1.30bn) amid a sharp pickup in activity: stock trading volumes jumped 960% YoY to more than AMD 2.1bn (~$5.7m). The debt market also showed solid momentum: primary placements of government bonds exceeded AMD 38.1bn (~$103.5m), and secondary trading surpassed AMD 8.3bn (~$22.6m). Corporate bond turnover grew 41% YoY to over AMD 11.5bn (~$31.3m). Repo volumes increased 221% YoY to AMD 19.8bn (~$53.8m). These figures point to improving liquidity and broader investor engagement in local capital markets—developments we view as moderately constructive for medium‑ to long‑term performance.

Corporate News

On June 15, 2026, IDBank launched a public offering of two bond tranches: AMD 2.5bn (approximately $6.8m) and USD 5m. The AMD-denominated tranche has a 3-year maturity and a 10% annual coupon, paid semiannually. The USD-denominated tranche matures in 27 months and bears a 5% annual coupon, paid quarterly. The subscription period runs until November 15, 2026, for the AMD tranche and August 15, 2026, for the USD tranche.

Two-Week Outlook

Between June 19 and 29, the key catalyst will be the market reaction to the Central Bank of Armenia’s refinancing-rate decision. May activity data and other statistical releases are also due. Inflation has slowed but remains slightly above the upper bound of the target range, reducing the likelihood of near-term policy tightening. In our base case, we expect the rate to be left unchanged, as external inflationary pressures have eased following reports of a cease-fire arrangement between the U.S. and Iran. Should a U.S.–Iran memorandum be signed, it would imply the reopening of the Strait of Hormuz to commercial shipping. Against this backdrop, Brent crude futures have fallen by more than 15% over the past five sessions to roughly $80 per barrel. That said, in our view, the risk of further escalation has not been fully extinguished.

Under these conditions, the tone of the central bank’s communication will be critical for the local market. It will also be shaped, albeit indirectly, by domestic demand and geopolitical developments in Armenia and the broader region.