Двухнедельный обзор фондовых рынков №348. Сезонная рокировка

Corporate News in Focus of Our Analysts

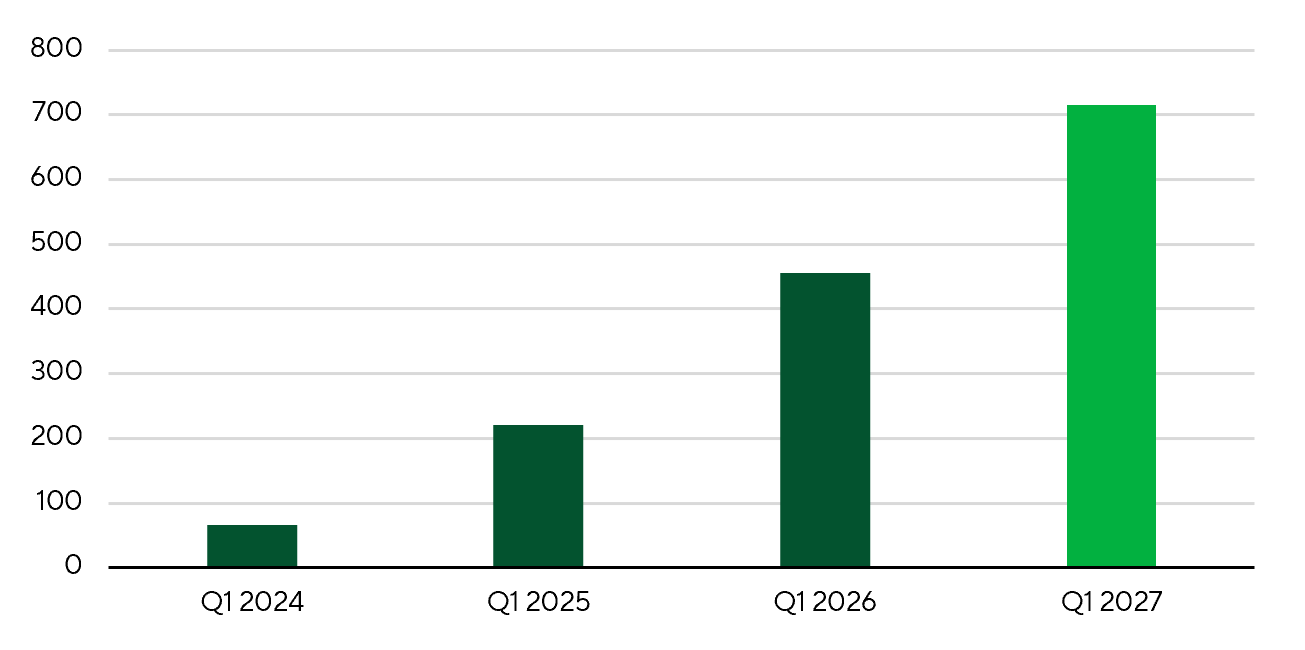

Apple

During the second week of June, Apple (AAPL) hosted its annual WWDC 2026 conference. While the company unveiled no major hardware updates, management provided additional detail on its AI roadmap, though investors were left without a definitive timeline for commercial rollout. The event also marked the final WWDC under Tim Cook, who is scheduled to hand over the CEO role to John Ternus on September 1. The leadership transition is expected to increase Apple's focus on hardware innovation and AI development. The centerpiece announcement was Siri AI, a next-generation assistant powered by Apple Foundation Models 3 (AFM 3) and the broader Apple Intelligence architecture. Apple explicitly described the models as proprietary systems developed in partnership with Google rather than a rebranded version of Gemini. While the economics of the partnership remain undisclosed, media reports suggest Apple pays Google approximately $1.0bn annually. Siri AI was introduced in beta without a firm public launch date. Availability in the EU and China is expected to be delayed due to ongoing regulatory discussions. Apple also outlined a tiered monetization framework for advanced cloud-based AI capabilities.

Access to higher usage limits will require subscriptions such as iCloud+ or Apple One, with indications that enhanced AI allowances may vary across subscription tiers. Investor reaction was muted. Despite greater visibility into Apple's AI strategy, the absence of concrete deployment milestones weighed on sentiment, sending AAPL shares down 3.6% on June 9.

Cumulative Apple Intelligence Capable iPhone Shipments, mln units

Sources: Counterpoint Research, Freedom Broker

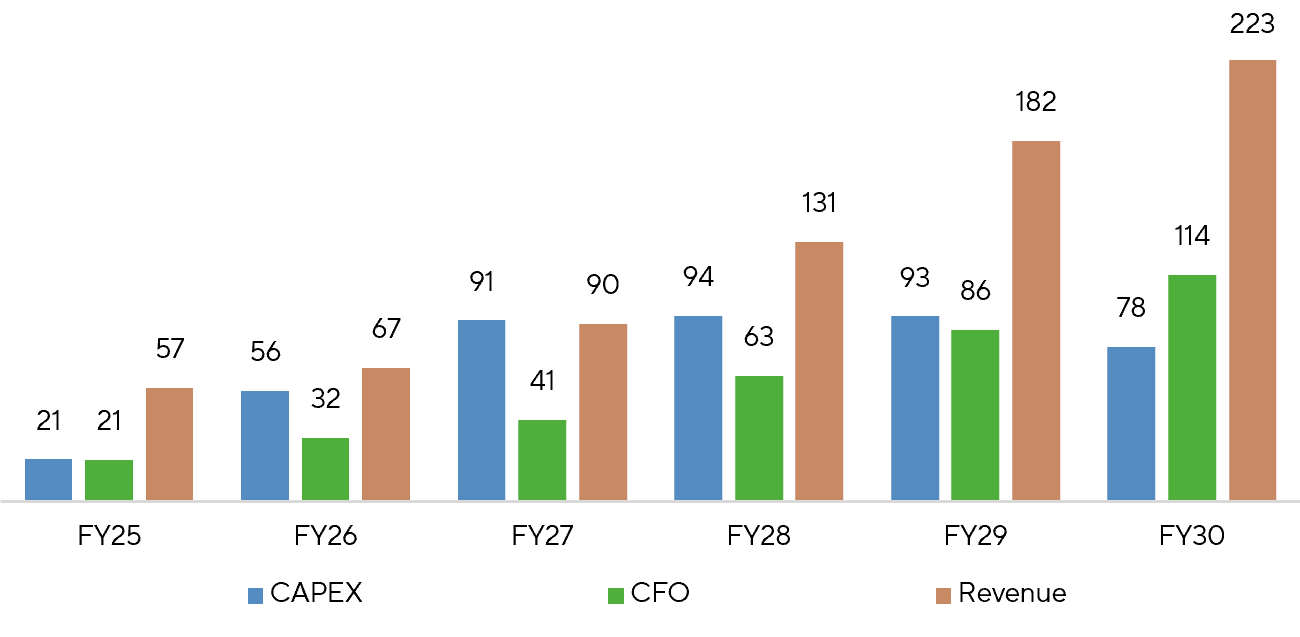

Oracle

On June 10, Oracle (ORCL) reported quarterly results that exceeded expectations for both revenue and earnings while significantly expanding its RPO backlog to a record $638bn. Cloud infrastructure revenue accelerated to 93% YoY growth, overshadowing weaker trends in legacy software and hardware businesses. The core investment thesis remains Oracle's ability to convert its unprecedented contract backlog into revenue despite rising equipment and data-center construction costs. Management plans to invest approximately $90bn–$95bn in capex during FY27, above prior estimates, reflecting higher component costs and new customer commitments. The company has also introduced financing structures involving customer-owned equipment and customer prepayments to reduce funding requirements. As a result, Oracle expects to fund only about $70bn of FY27 capex with its own resources, including approximately $40bn to be raised in capital markets during calendar 2027. Guidance for 1Q27 and FY27 revenue and EPS was in line with or slightly above expectations, while management reiterated its long-term financial targets. ORCL shares fell 8.5% on June 11, which we view as a reasonable market response to another increase in planned capex.

Key Financials of Oracle Corp. (ORCL), $bn

Sources: FactSet, Oracle, Freedom Broker

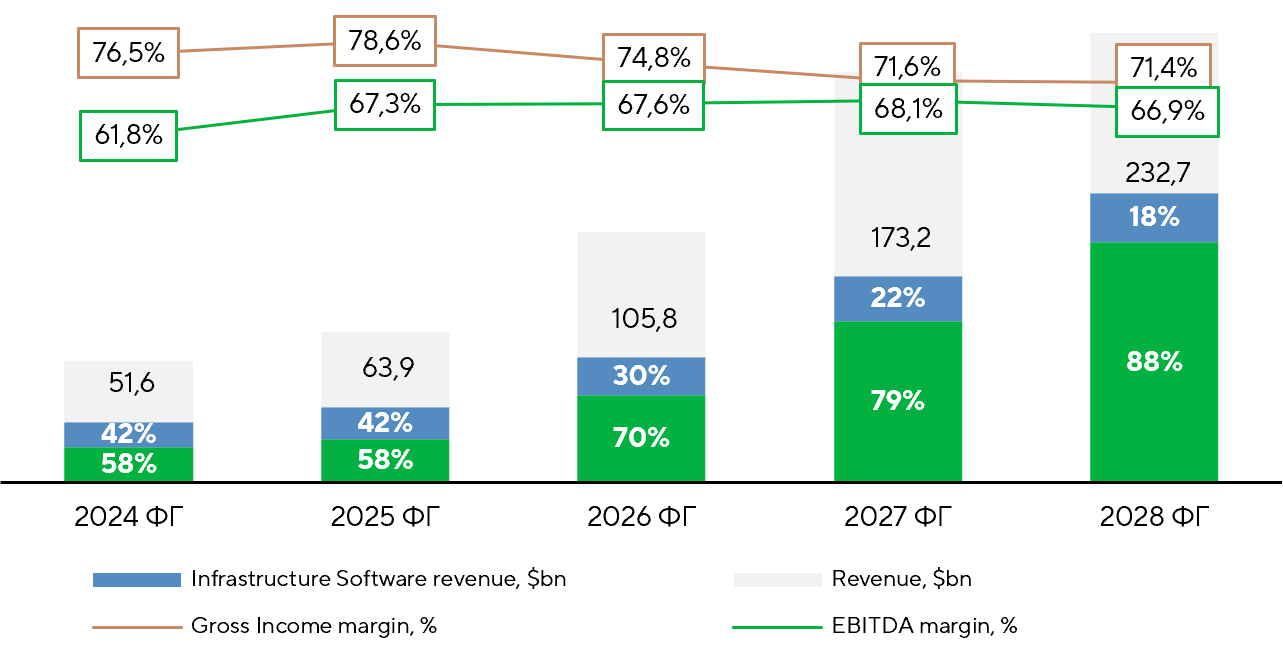

Broadcom

Broadcom (AVGO) delivered another record quarter, beating consensus expectations across revenue, EPS, and all major margin metrics. Custom AI accelerators and networking solutions remain the core growth engine, with management once again describing demand as "insatiable." The customer base among hyperscalers and leading AI labs continues to expand, while order visibility now extends through 2028. Investor concerns centered on two issues. First, management reaffirmed—but did not raise—its long-term AI targets. Second, guidance implies lower gross margin next quarter due to a shift in revenue mix. In our view, neither development signals a deterioration in fundamentals. Rather, the unchanged AI outlook reflects management's disciplined approach to guidance, while the expected margin pressure appears driven by mix effects rather than any structural decline in profitability. The recovery in non-AI semiconductor markets and accelerating software growth provide additional support. Growth in data-center CPU deployments is increasing demand for VMware products under core-based licensing models. Broadcom's new XPV financing platform, supported by Apollo and Blackstone, is helping fund compute infrastructure deployments and convert demand into revenue opportunities. Against this backdrop, the 12.6% post-earnings selloff on June 4 appears disconnected from underlying fundamentals.

--Key Financials of Broadcom, Inc. (AVGO)

Sources: FactSet, Broadcom, Freedom Broker

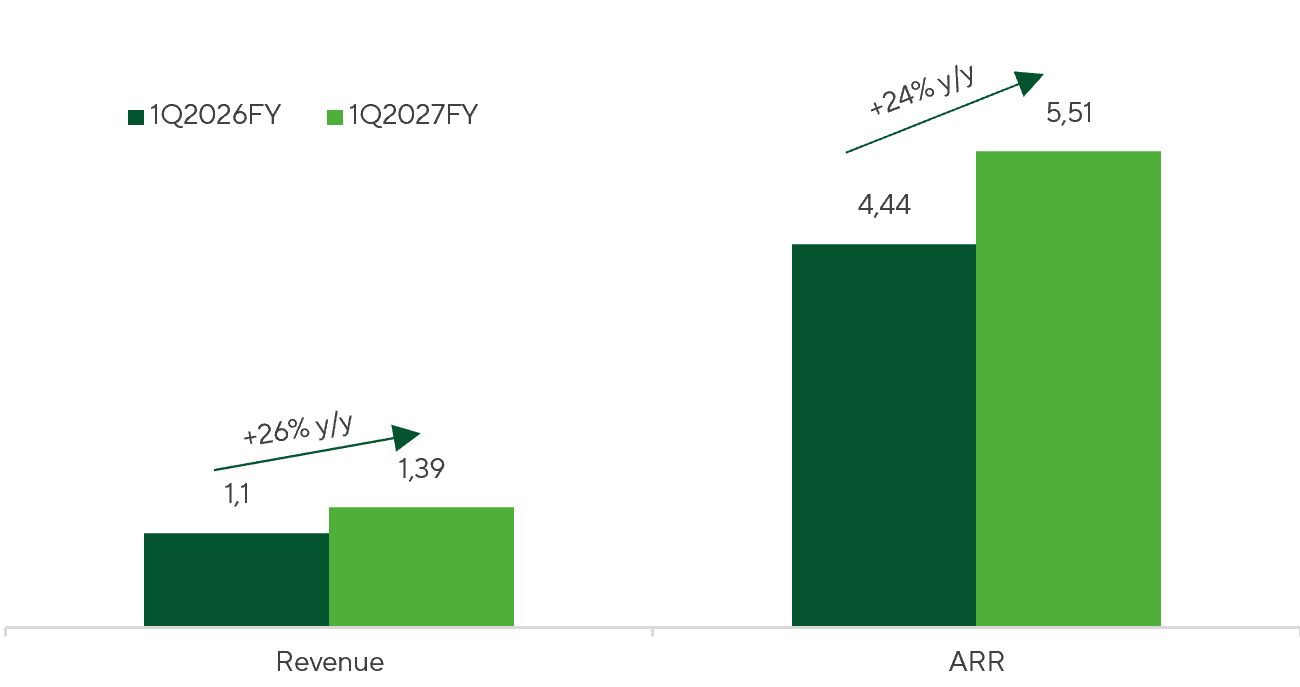

CrowdStrike

CrowdStrike (CRWD) continues to solidify its position as a category-defining cybersecurity platform. In Q1 FY27, revenue increased 26% YoY to $1.39bn, ARR reached $5.51bn, net new ARR totaled a record $256m, and non-GAAP operating margin expanded to 23.5%, underscoring the combination of robust demand, strong platform monetization, and growing operating leverage. The primary growth driver remains the consolidation of enterprise cybersecurity spending around the Falcon platform. Falcon Flex continues to accelerate deal velocity, deepen cross-sell penetration, and expand module adoption across customer environments, reinforcing CrowdStrike's platform-centric strategy and increasing wallet share among large enterprises. The next leg of growth is increasingly tied to AI. The proliferation of generative AI models and agentic workloads is creating entirely new attack surfaces, while the company has already established strong positions across cloud security, identity protection, data security, and AI-native environments, including its relationships with leading AI labs (Anthropic and OpenAI). Management's decision to raise FY27 revenue guidance to $5,915–5,959m suggests CRWD is entering the second half of the fiscal year with sustained demand momentum, increasing platform scale, and a clear runway for further penetration within its existing customer base.

Source: CRWD financial stetement

Financial results CRWD ($ bn)

Palo Alto Networks

Palo Alto Networks (PANW) exited Q3 FY26 with clear evidence of accelerating underlying demand. Revenue increased 31% YoY to $3.0bn, billings surged 61% YoY to $4.18bn, while Next-Generation Security ARR rose nearly 60% YoY to $8.13bn. The results reinforce ongoing platformization trends and provide elevated visibility into forward revenue generation. The near-term growth driver remains the global buildout of AI infrastructure. Rising network traffic, accelerated data-center construction, and increasing demand for high-performance security architectures are already translating into record demand for both hardware and software firewall solutions. Additional upside is supported by a broader platform expansion strategy following the acquisitions of CyberArk and Chronosphere. These assets strengthen PANW’s positioning across identity security, observability, and AI-agent protection, while early integration progress is helping sustain operating efficiency despite some pressure on gross margins. Overall, PANW continues to stand out as one of the most direct public-market beneficiaries of the enterprise AI investment cycle, combining rapid recurring revenue expansion, deeper platform penetration, and increasing exposure to the security requirements of next-generation AI infrastructure.

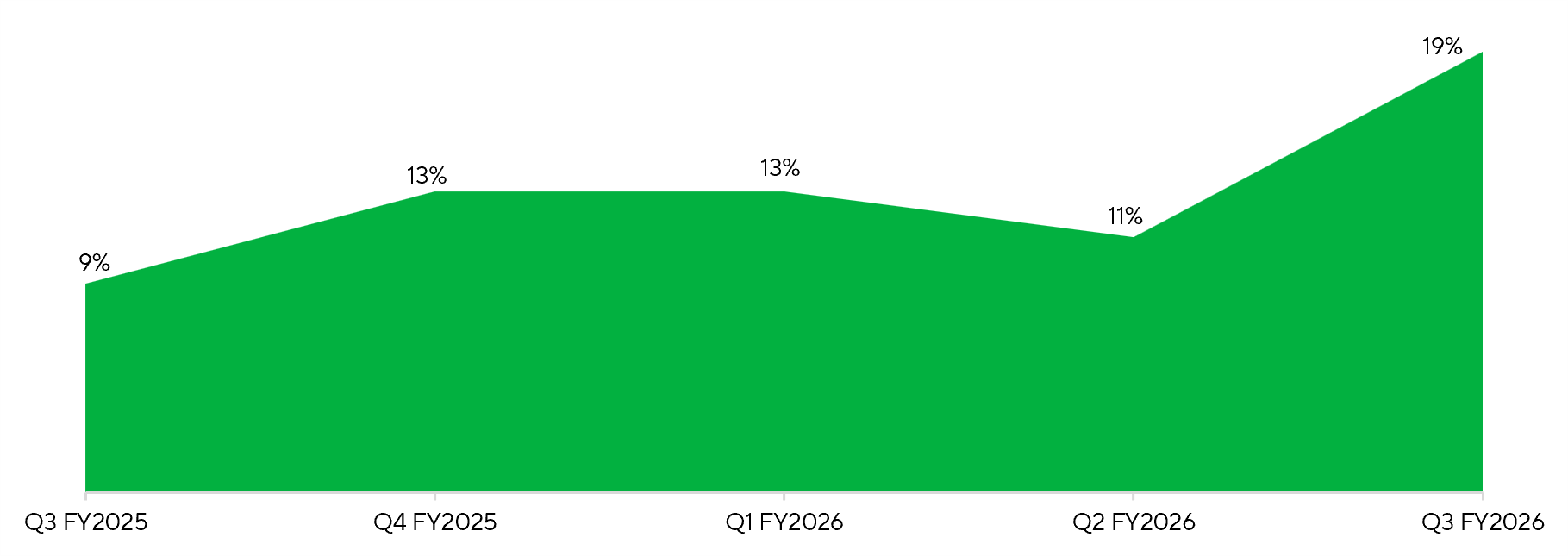

TTM Firewall Bookings Growth, y/y

Source: Palo Alto Networks IR presentation