Двухнедельный обзор фондовых рынков №348. Сезонная рокировка

Nothing but Positives

Despite ongoing external uncertainty, the UAE’s stock market indices posted moderate gains

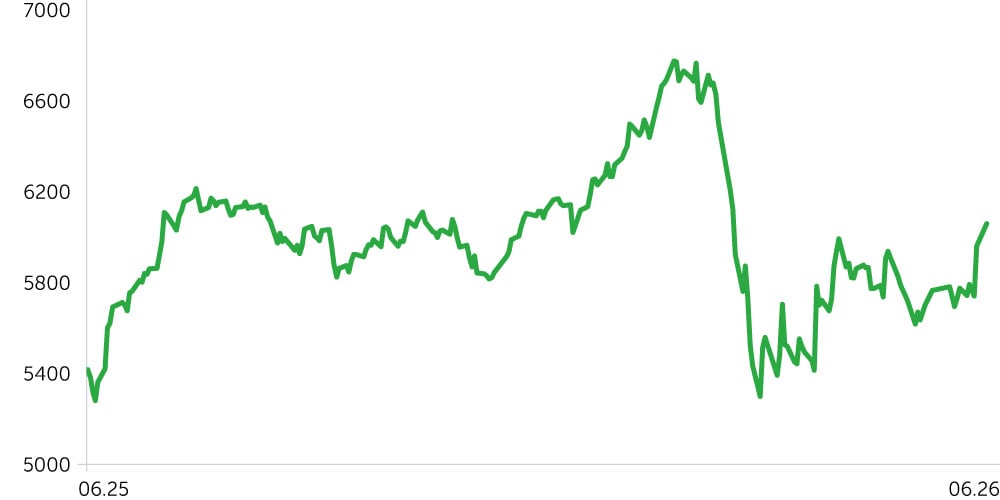

DFM General Index: 1-Year Dynamics

Abu Dhabi Securities Exchange Index: 1-Year Dynamics

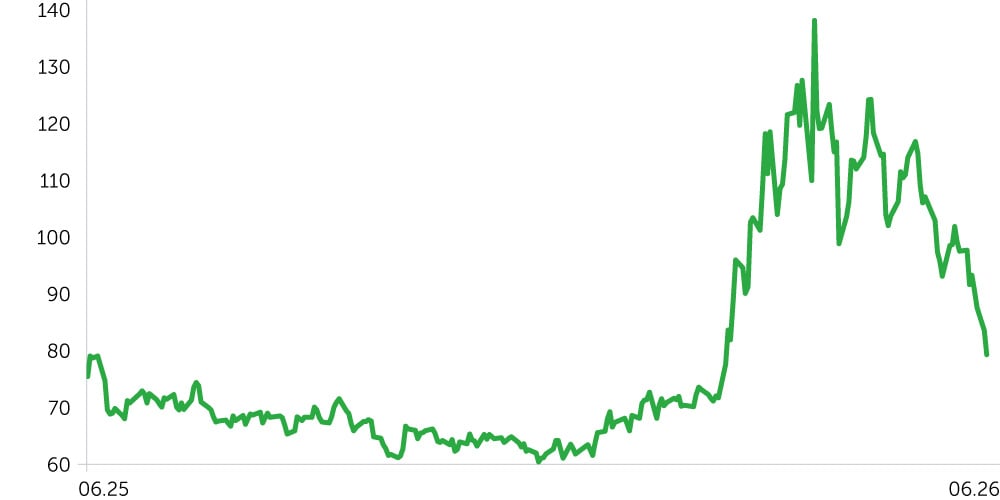

Brent Oil, 1-Year Dynamics

Over the two-week period from June 2 to June 16, 2026, UAE equity indices posted steady gains, supported by easing geopolitical tensions and expectations of a reopening of the Strait of Hormuz. Local exchanges observed a public holiday on Monday, June 15, for the Islamic New Year (1448), so Tuesday, June 16, was the final trading day of the review period. The Dubai Financial Market General Index (DFMGI) rose 5.6% to 6,055 from 5,732, while the Abu Dhabi Securities Exchange General Index (ADXGI) gained 3.6% to 9,963 from 9,621. The advance was broad-based and included a sharp move higher on June 12, with Dubai up 3.8% and Abu Dhabi up 2.7%, on expectations of a U.S.–Iran peace agreement. By comparison, the S&P 500 dropped 1.3% to 7,511 from 7,610 over the same period, while Brent crude fell 19.4% to $79 per barrel from $98 amid optimism around negotiations related to the Strait.

Sector performance in the UAE was uniformly positive over the period, with all sectors closing higher. Utilities led (+11.60%), followed by Real Estate (+6.99%) and Energy (+5.72%), signaling broad risk appetite and rotation into cyclicals. Abu Dhabi National Energy (TAQA, +13.79%) and DEWA (+7.42%) drove Utilities. Real Estate gains were broad-based: Emaar Development (+7.46%), Aldar Properties (+7.28%), Emaar Properties (+7.14%), and Alpha Dhabi (+6.82%). In Energy, ADNOC Gas (+6.38%) and ADNOC Drilling (+5.69%) outperformed. In Industrials and Logistics (+5.34%), notable movers included Air Arabia (+13.95%), Dubai Taxi (+9.00%), and Gulf Navigation Holding (+8.40%), whereas Aramex declined 3.24%. Financials (+4.20%) were supported by Abu Dhabi Commercial Bank (+12.92%), Emirates NBD (+11.21%), Investcorp Capital (+10.27%), Abu Dhabi Islamic Bank (+8.72%), and First Abu Dhabi Bank (+8.38%). Consumer Discretionary (+4.34%) and Consumer Staples (+3.77%) also closed higher, led by Americana Restaurants (+5.10%) and Spinneys (+6.84%). Communication Services was the most subdued performer (+3.45%), with e& and du up 3.90% and 2.09%, respectively.

The 10-year UAE proxy government bond yield decreased to 4.72% at the period end from 5.06% at the start (−33.7 bps), while the 10-year U.S. Treasury yield edged down from 4.53% to 4.51% (−2 bps). Consequently, the UAE–U.S. 10-year spread narrowed from ~53 bps to ~21 bps, reflecting a faster decline in local yields as the geopolitical risk premium normalized.

Economic Updates

- According to final data from the Federal Competitiveness and Statistics Centre, reported by state agency WAM, the UAE’s real GDP grew 6.2% in 2025 to $517.3bn, with non-oil GDP rising 6.8% to $408.4bn. Growth was driven by construction (+11.1%), financial services and insurance (+10.4%), real estate (+7.9%), and transportation (+7.8%). Non-oil foreign trade increased 26%, surpassing $1tn for the first time.

- The S&P Global UAE PMI rose to 52.6 in May 2026 from 52.1 in April. While still above the 50.0 mark—indicating continued, albeit modest, expansion in the non-oil private sector—April’s reading was a near four-year low. The closure of the Strait of Hormuz resulted in the steepest lengthening of delivery times since April 2020.

- Abu Dhabi’s real estate regulator, ADREC, froze rent increases effective June 2, 2026, imposing a zero rent-increase cap (versus the standard 5%) on residential, commercial, and industrial leases. The move followed a 15% rise in new rents across Abu Dhabi over the past year and a 23% increase in investment zones, straining affordability.

- Separately, on May 1, 2026, the UAE formally withdrew from OPEC and OPEC+, removing quota constraints on production. As part of its independent strategy, ADNOC announced approximately AED 200bn ($55bn) in project contracts for 2026–2028, though actual output in the region remained constrained by the situation in the Strait of Hormuz.

Corporate News

- On June 11, Emaar Properties unveiled an AED 200bn (~$55bn) master plan for a district spanning over 4.5 million sq m, built under the “20‑min city” concept, designed for nearly 150k residents and divided into five zones. Founder Mohamed Alabbar called it the company’s “most ambitious dream.” In 1Q26, Emaar’s revenue rose 23% to AED 12.4bn, and real property sales increased 16%. Following the announcement, the developer’s shares were among the market’s top performers (Emaar Properties: +7.14%; Emaar Development: +7.46%).

- From June 1 to 12, Emirates NBD conducted a mandatory tender offer to acquire up to 26% of India’s RBL Bank at ₹282.38 per share (~$2.98). The Reserve Bank of India approved the acquisition of up to 74% of RBL Bank, with a minimum stake of 51% and voting rights capped at 26%. The bank plans to invest roughly $3bn, primarily via a preference issue priced at ₹280 per share (~$2.96), marking the largest foreign investment in India’s banking sector to date.

- On June 1, e& signed a binding agreement to sell a 12.5% stake in Careem Technologies to Uber for $100m in cash, reducing its holding from 50.03% to 37.53% and moving to equity‑method accounting. The deal implies an equity valuation for Careem of roughly $1.6bn.

- ADNOC Gas reported 1Q26 net profit of $1.1bn despite disruptions in the strait; it declared a quarterly dividend of $941m payable in June 2026 and guided to $400–600m [AS1.1]in net profit for 2Q26. The stock rose 6.38% over the period.

- Abu Dhabi Ports, via its subsidiary Black Caspian, raised the price of its mandatory tender offer for Egypt’s Alexandria Container and Cargo Handling to EGP 27.47 per share (~$0.54), triggering an approximately 8% rally in the stock on June 12.

- Dubai Holding became the largest shareholder in Emaar Properties with a 29.73% stake after acquiring a 22.27% holding from ICD.

Two-Week Outlook

Uncertainty in the oil market remains elevated, with developments around the Strait of Hormuz still the primary driver of prices. Over the past week, WTI fell 6.3% to $84.90 per barrel—a two‑month low—on expectations of a potential U.S.–Iran understanding. That optimism looks premature: the memorandum’s text has not been released and may not be signed until Friday, June 19, 2026. Moreover, the document would be a roadmap rather than a final agreement, outlining talks over the next 60 days. The sides remain far apart on core points, including Iran’s nuclear program, maritime traffic through the Strait of Hormuz, and Tehran’s support for Hezbollah and Hamas.

In our base case, a renewed escalation would likely lift WTI above $110 per barrel; conversely, de-escalation and a reopening of the strait would prompt a sharp correction. If the current “double blockade” persists, we would expect a gradual increase in prices.

Near term, three factors should remain the key drivers for the UAE market: oil price dynamics and the situation in the Strait of Hormuz; the sustainability of second‑quarter 2026 corporate earnings; and the speed at which the geopolitical risk premium on local assets normalizes. Solid results from the ADNOC Group, as well as banking, real estate development, and logistics, should sustain interest in large‑cap UAE names. In a more cautious scenario, rising global rates or a sharper-than-expected oil correction following de-escalation could spur a rotation into defensives and a period of index consolidation after the recent rally.