Investment Review №328. Waiting for change

Unscheduled sale

By the end of the first ten days of September, local exchange instruments had moved into the red.

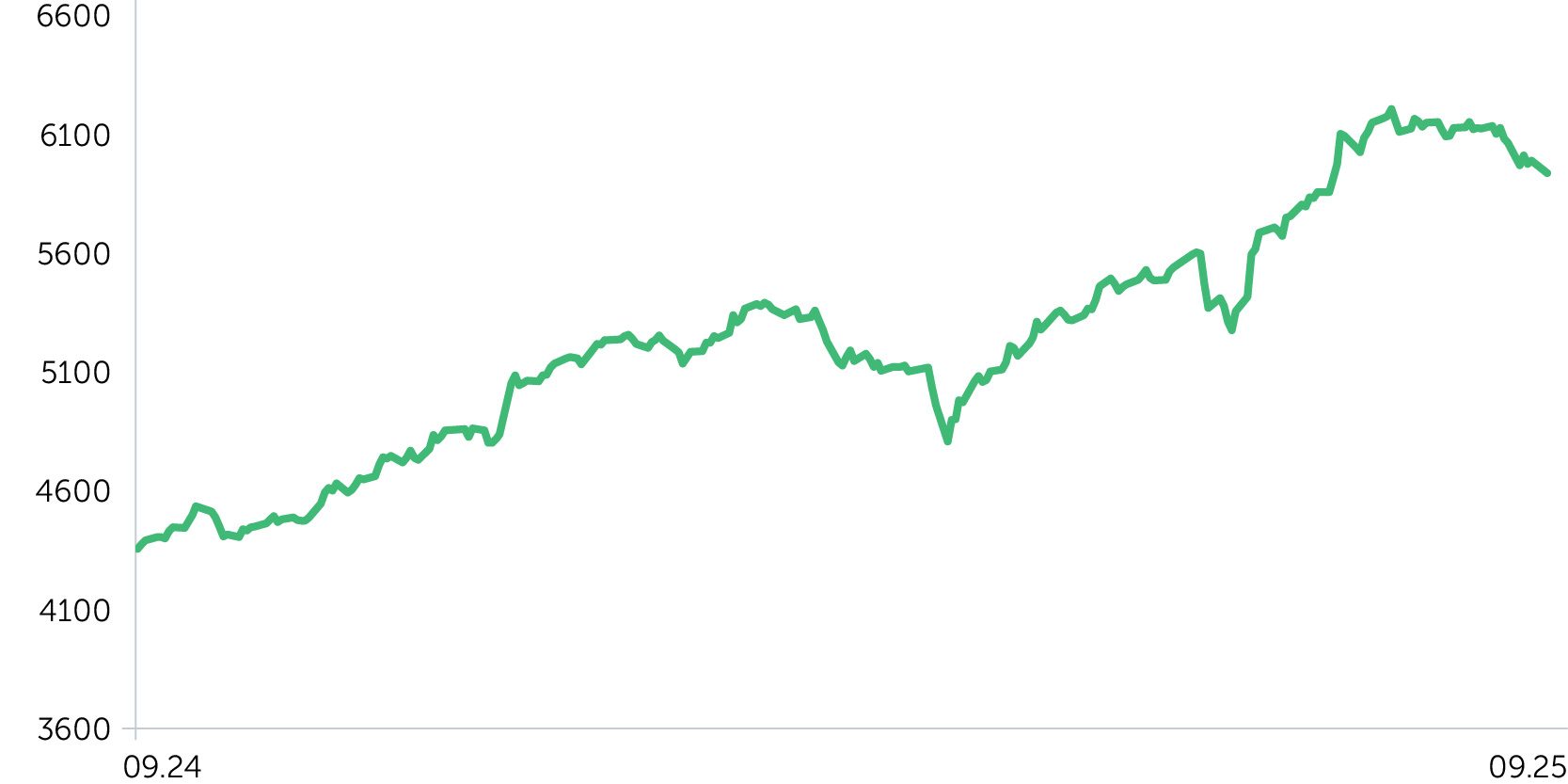

DFM General Index: 1-Year Dynamics

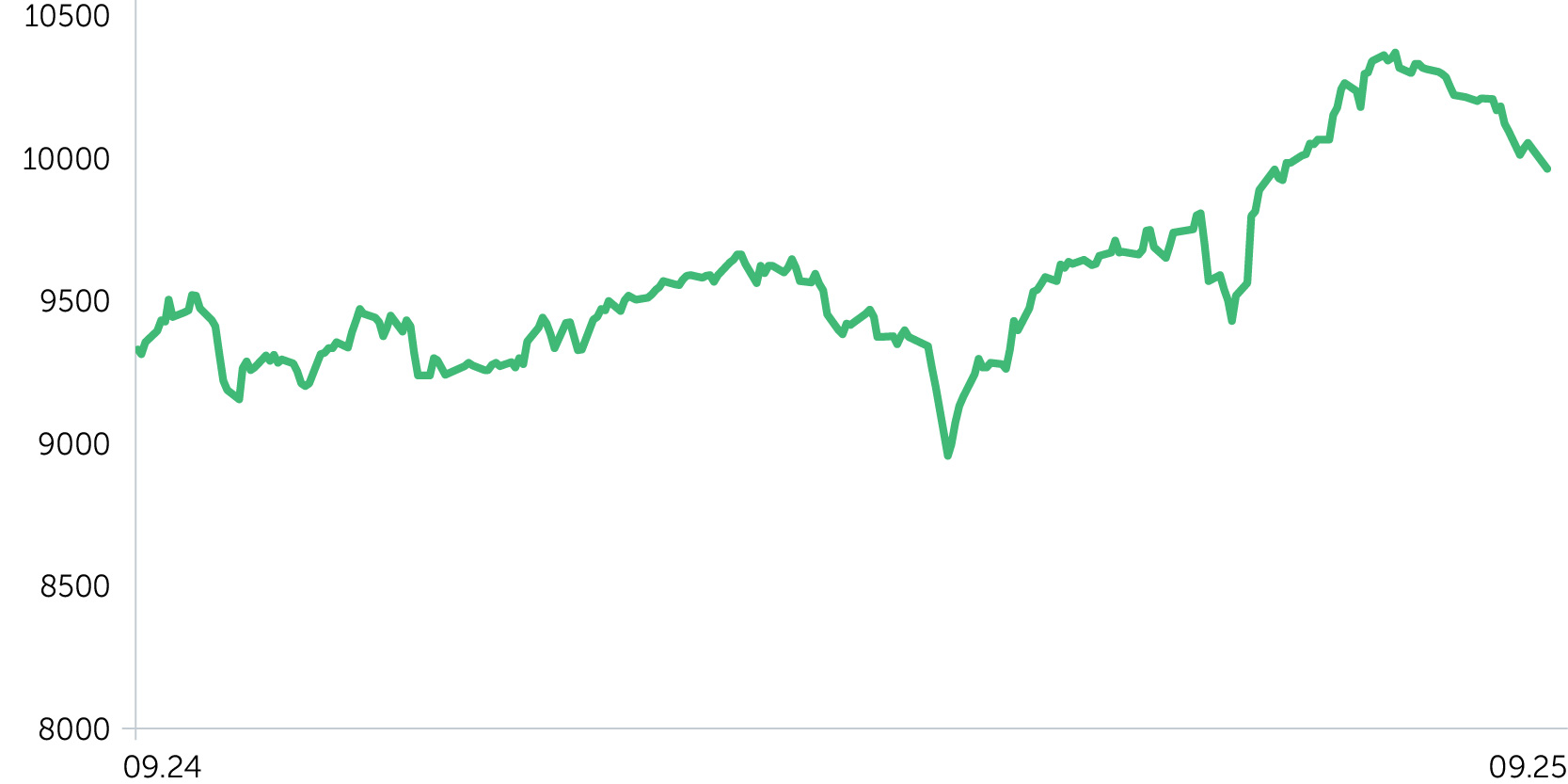

Abu Dhabi Securities Exchange Index: 1-Year Dynamics

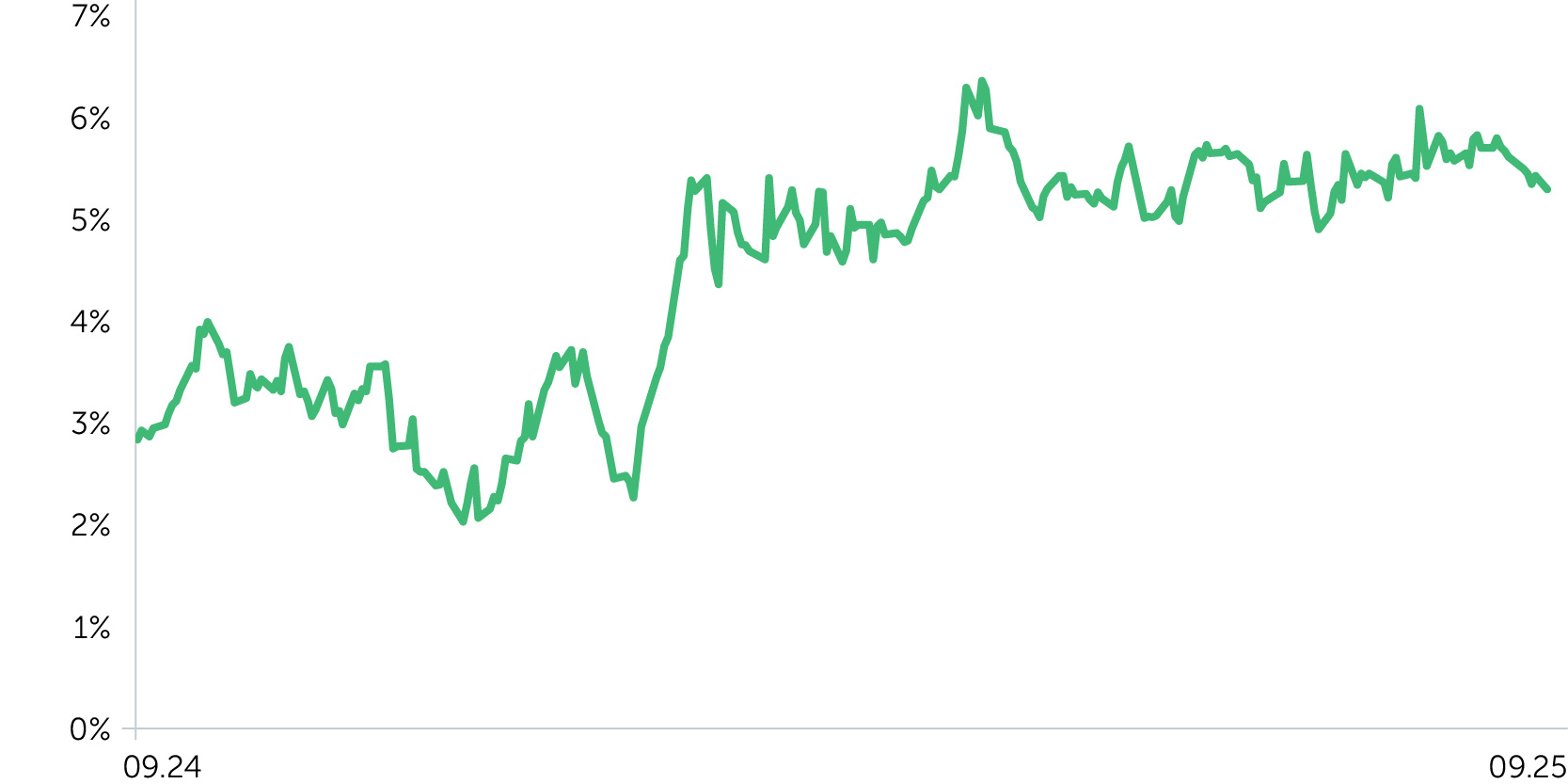

Yield, Forward Rate 1m10y, UAE, 1-Year Dynamics

Brent Oil, 1-Year Dynamics

Between August 26 and September 8, 2025, UAE equity markets declined by an average of 2.9%. The Dubai Financial Market (DFM) dropped 3.3%, while the Abu Dhabi Securities Exchange (ADI) fell 2.4%. Over the same period, Brent crude prices lost 4.0%. Market trends closely mirrored the movement in oil prices during these weeks, and even positive signals regarding the Fed’s rate trajectory failed to provide meaningful support.

Sector performance was mixed. Financials declined by an average of 2.2%, while Utilities advanced, gaining approximately 2.75%. Among large-cap names, Abu Dhabi National Energy Company (TAQA) saw a notable increase of 4.2%, driven by strategic acquisitions and newly secured funding for projects in Saudi Arabia. Simultaneously, ADNOC Gas dipped 0.88%, while Abu Dhabi Commercial Bank (ADCB) dropped 12.10%. This descent followed Monday's issuance of over $1.5 billion in shares, marked down roughly 30% from the September 4 closing price.

UAE Treasury yields declined by 40 basis points, while U.S. Treasury yields fell by 17 basis points, broadly reflecting the medium-term trajectory of Federal Reserve policy rates. The spread remained broadly unchanged.

Economic Updates

- On September 7, OPEC+ agreed to boost oil production by 137,000 barrels per day starting in October.

- The dirham weakened approximately 8% against the British pound, making Dubai real estate more affordable for UK buyers. Developers such as Binghatti, Danube, Damac, and Aldar are capitalizing on this trend by opening sales offices in London and launching UK-themed projects. British investment in Dubai property surged 62% year-over-year in Q2 2025, surpassing Indian buyers to become the largest foreign investor group (Betterhomes).

- The UAE unveiled K2 Think — a compact yet powerful open-source AI model with 32 billion parameters, developed by MBZUAI and G42.

Corporate News

- Abu Dhabi National Energy Company (TAQA: +4.2%) successfully secured nearly $4 billion in funding to build two greenfield gas turbine power plants—Rumah 2 and Al Nairyah 2—in Saudi Arabia. These projects are being developed in partnership with JERA and AlBawani Capital, with a combined capacity of approximately 3.6 GW. Power purchase agreements (PPAs) were signed for a 25-year term.

- ADNOC Gas (ADNOCGAS: -0.88%) shares were added to the FTSE Emerging Index, a move expected to draw increased investor interest. The company could see capital inflows reaching up to $250 million ahead of the official index inclusion on September 22.

- Abu Dhabi Commercial Bank (ADCB: -12.1%) will raise up to AED 6.1 billion (approximately $1.66 billion) via a rights issue, offering up to 592.2 million new shares at AED 10.3 each. This price includes a nominal value of AED 1 plus a premium of AED 9.3 and represents a 30% discount to the September 4, 2025 closing price. Mubadala Investment Company, the bank's largest shareholder, reaffirmed its commitment by pledging all its shares to the offering.

Two-Week Outlook

The growing likelihood of stricter sanctions targeting Russia’s oil and gas sector, combined with seasonally weak hydrocarbon demand, is putting downward pressure on oil prices. As a result, energy sector equities are expected to trade sideways in the near term. In our view, much of the upside potential has already been priced in. U.S. import tariffs continue to weigh on global trade, while OPEC+ production quota increases could trigger a more pronounced decline in prices. Since the start of the year, quotas have risen by 1.9 million barrels per day (MMBD), with actual output (as of May) up by 0.6 MMBD. Meanwhile, interest in the local market continues to grow, supported by strong earnings across the financial sector. Given structurally low liquidity and a relatively small pool of publicly traded capital compared to developed markets, we believe foreign inflows could further bolster relative outperformance versus the S&P 500—provided geopolitical tensions in the region ease. We view the current market correction as temporary in nature, though it may persist over the next couple of weeks.