Investment Review №330. Profit favors the bold

Review as of October 8

Global Perspective

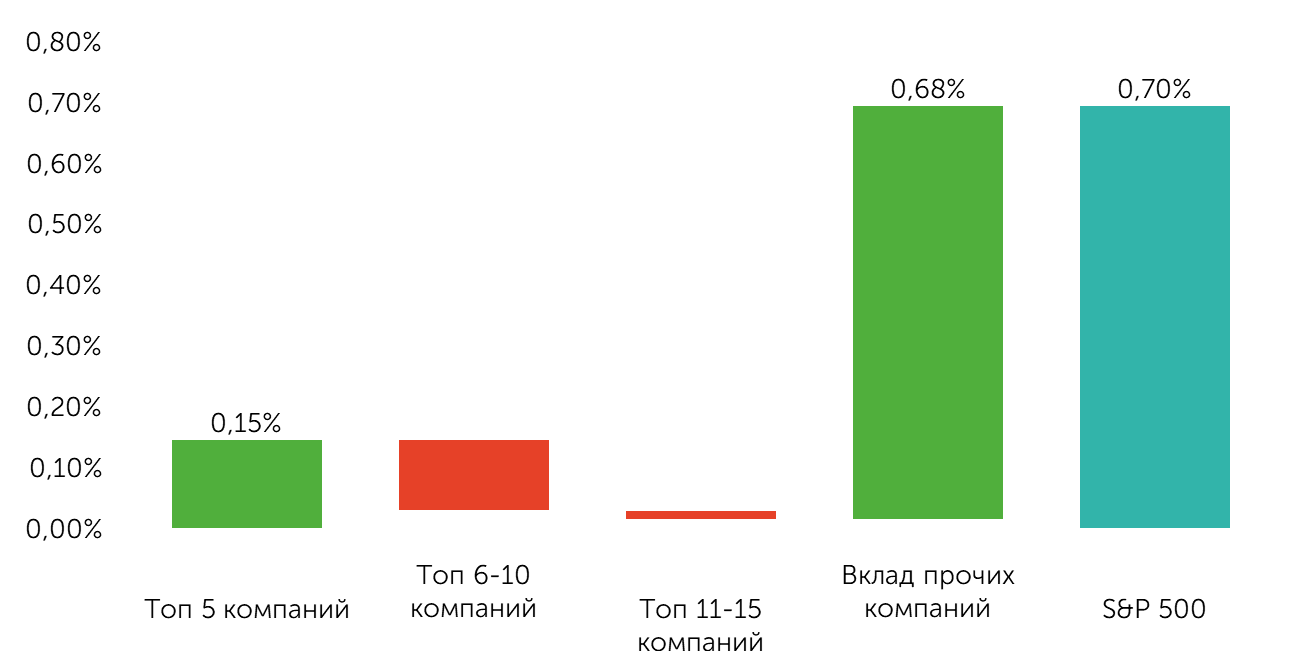

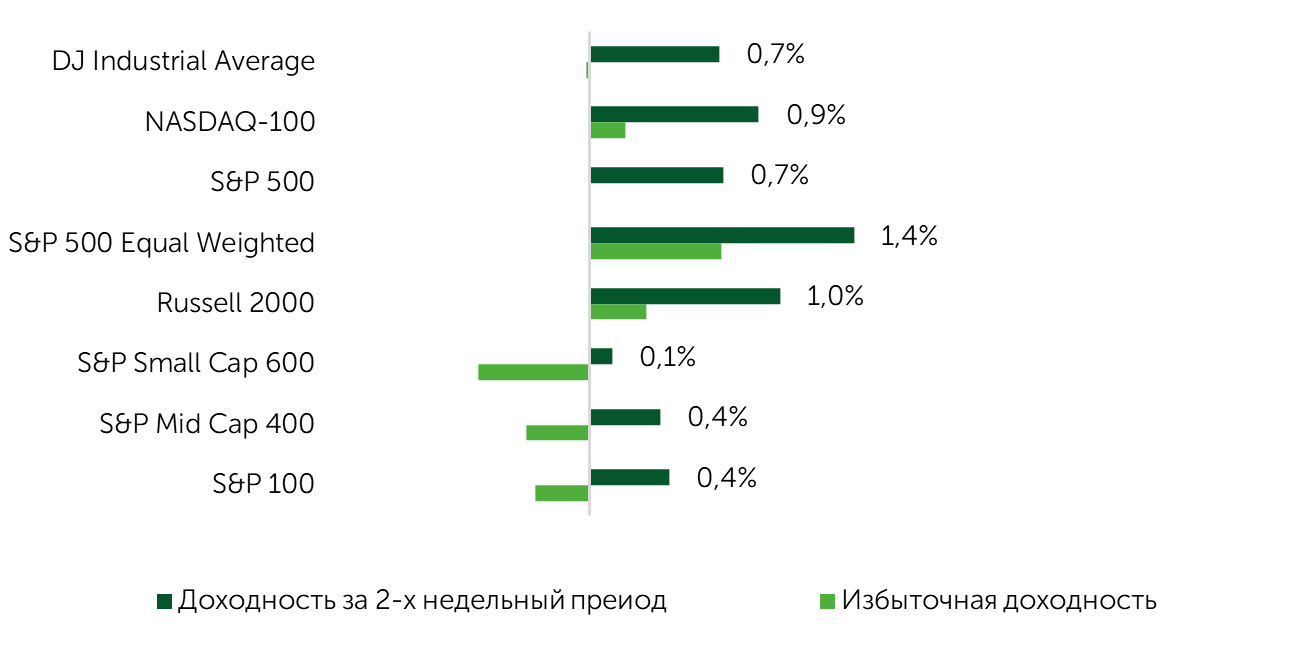

Over the two-week period, all major U.S. equity indices ended in positive territory. The S&P 500 gained 0.7%, mirroring the performance of the Dow Jones Industrials, while the Nasdaq 100 added 0.9%. Notably, market rotation occurred primarily within the largest-cap names. The S&P 100 posted an excess return of -0.3%, reflecting weak performance from the top 15 companies by market cap, which contributed virtually nothing to the S&P 500’s overall movement during the period. At the same time, excess returns for small- and mid-cap stocks were also negative—at -0.6% and -0.3%, respectively.

Change in employment by company category (year-on-year, ADP data)

Source: FactSet, Freedom

Excess returns of major US stock indices

Source: FactSet, Freedom

The U.S. government shutdown has officially begun. Interestingly, markets rallied from the last week of September through early October, largely shrugging off potential risks tied to the temporary halt in government operations—including delays in macro data releases and possible pressure from credit rating agencies. Instead, investor focus remained on macroeconomic trends and corporate fundamentals. Bulls also found support in historical data, which shows that shutdowns are typically short-lived and have minimal long-term economic impact—any losses during the period are often quickly reversed once the government reopens. Statistically, dip-buying ahead of or during a shutdown has often proven to be a favorable entry point for long positions.

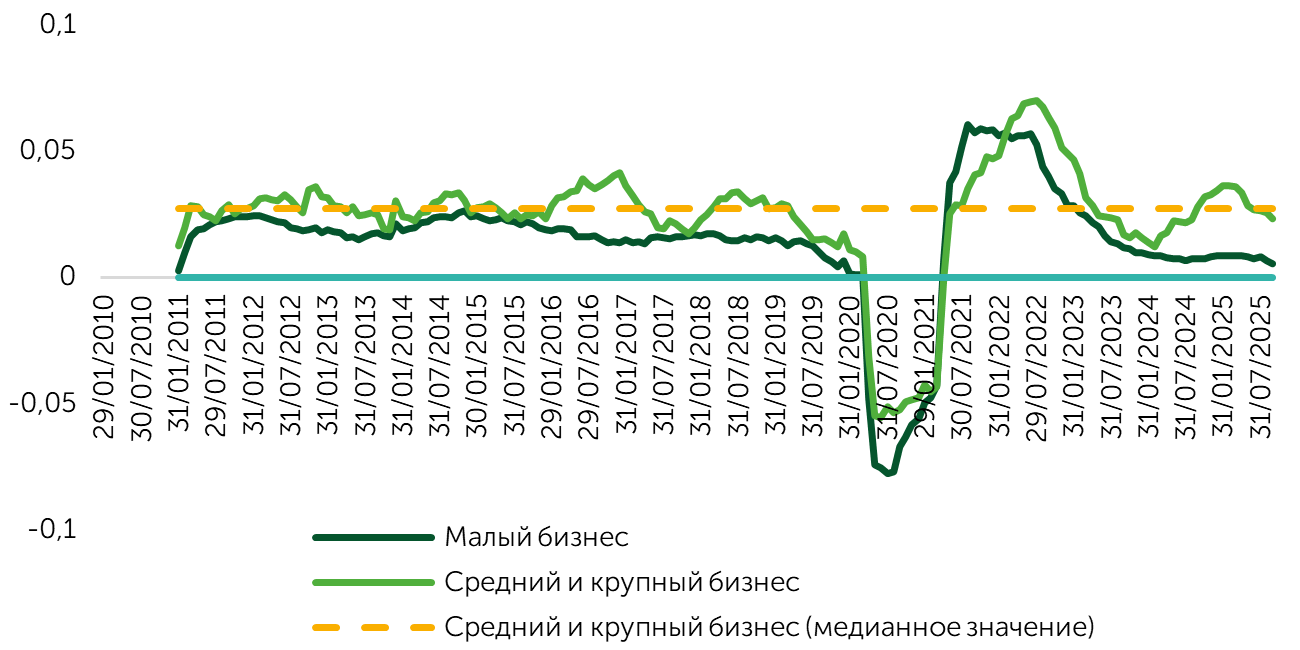

The state of the labor market—particularly trends in employment—remains a cornerstone for market sentiment. Markets rallied on the back of weaker-than-expected private payrolls data. According to ADP, private payrolls declined by 32,000, while the consensus had anticipated an increase of 52,000. Additionally, the previous reading was sharply revised down from 54,000 to just 3,000. The positive market reaction reflects sustained confidence that the economy will continue to maintain a delicate balance despite slower hiring, supported by the absence of widespread layoffs and improving consumer spending trends. It is also worth noting that, given labor market softness among small businesses, we expect hiring activity to recover in the coming quarters—supported by positive earnings trends and improving overall sentiment in the small business segment, as reflected in recent NFIB surveys.

Returns by stock group over the last two weeks

Source: FactSet, Freedom

Recent PMIs support the view that hiring trends currently show little correlation with broader economic activity. Specifically, S&P Global PMIs largely exceeded expectations, while ISM data painted a mixed picture but pointed to improving employment conditions in the non-manufacturing sector.

In a landscape marked by a limited flow of macroeconomic data and earnings reports, the market’s focus remained firmly on corporate developments among the largest players in the AI sector. Notably, the initial positive reaction to the $100 billion deal between NVIDIA and OpenAI was later reassessed—investors grew increasingly skeptical about the sustainability of OpenAI’s business model and its ability to attract market funding, with some analysts dubbing NVIDIA the last remaining capital source.

In the penultimate week of September, the market experienced increased speculation about the valuations of several leading AI companies, alongside growing concerns about the sustainability of the investment cycle and potential risks tied to its cyclical nature. This pressure weighed on major tech stocks, including Oracle, whose shares experienced a multi-week correction despite the company reporting record infrastructure cloud order volumes. With no clear signs of a slowdown in the AI investment cycle, investors began buying into the late-September dip—boosted by the $14 billion NVIDIA-Meta deal and OpenAI’s ongoing demonstration of resilience and adaptability. Notably, OpenAI announced partnerships with Etsy and Shopify, enabling users to make purchases via chatbots. Recent data from Micron’s report highlighted not only positive idiosyncratic factors specific to the company but also underscored sustained strong demand for AI hardware solutions, as emphasized by the company’s management.

Market Focus

The next week and a half promise to be action-packed for the markets. Attention will focus on macroeconomic data releases—some of which are expected despite the ongoing government shutdown. According to FactSet, key inflation and labor market data scheduled for release next week will be critical for assessing the Federal Reserve’s next steps, with the central bank’s meeting expected at the end of the month. Additionally, the corporate earnings season for the largest U.S. banks will effectively kick off midweek. Investors will zero in on lending trends, portfolio quality, and commentary on the capital markets—especially given that M&A activity has already hit the $1 trillion mark this year.

The shutdown issue could take center stage in the coming weeks, potentially injecting heightened uncertainty and volatility into the market. Currently, investors must navigate in an environment lacking a significant portion of macroeconomic data. However, the core thesis remains unchanged—buying the dips caused by the shutdown tends to be a sound strategy, as historically, shutdowns have often provided attractive entry points for initiating long positions.

Overall, we expect October to be a strong month for equities. A secondary tailwind for the bulls may come from a seasonal statistical pattern—historically, when markets avoid a pullback in September, October tends to deliver stronger performance. Despite several uncertainties and headwinds, the overarching “Goldilocks” narrative remains intact—while the market has adjusted its expectations, the return to a disinflationary trajectory still underpins the base case. Our take on the labor market is this: the protracted slowdown in hiring poses a risk, but at the same time, it nudges the Fed toward policy easing—a dynamic that favors markets over the medium term. Labor market softness remains evident in the small-cap space—typically one of the primary beneficiaries of lower interest rates—and is showing signs of strengthening earnings momentum.

The earnings season is likely to be a major catalyst for the market in the weeks ahead. Overall, expectations remain robust—EPS growth over the past three months has shown a strong pattern, suggesting potential resilience in profit momentum for the current year. However, we believe the market may be highly sensitive to the absence of any “wow” factor. Consequently, we advise steering clear of stocks with stretched valuations.

Small-Cap Stocks

Over the past two weeks, the small-cap segment showed moderate gains: the Russell 2000 index (ETF: IWM) rose 1.0%, while investor interest continued shifting toward micro-cap stocks within the Russell Microcap index (ETF: IWC), which gained 2.1%.

Despite the positive price movement, the breadth of the rally remained limited—only 38.2% of companies in the Russell 2000 posted positive returns. Meanwhile, the rotation between “Value” and “Growth” factors persisted: the proportion of advancing stocks within the iShares Russell 2000 Value ETF and iShares Russell 2000 Growth ETF stood at 36.4% and 42.0%, respectively.

Over the next two weeks, the U.S. government shutdown could become a key factor for the small-cap segment. Potential delays in the release of critical macroeconomic data—specifically on the labor market and inflation—may force the Fed to make a “blind” interest rate decision (expected on October 29) without the usual data-driven guidance. The regulator is unlikely to hold rates steady and is expected to deliver an “insurance cut.” This outlook is reinforced by the futures market—FedWatch indicates a 92.5% chance of a 25-basis-point rate cut. However, if negotiations between Republicans and Democrats stall, the narrative of a “blind” Fed decision could persist and gain traction, injecting additional volatility into the markets.

According to predictive market data from Polymarket, the probability of the government shutdown ending between October 27 and November 3 is estimated at 19%, with 49% of participants expecting it to end sooner, and the remaining 32% anticipating a resolution after November 3. Notably, the share of the latter scenario has been growing significantly in recent days.

Technical Analysis of the Broad Market

The present technical setup indicates a Moderate Negative outlook. The RSI oscillator continues to hover around the 70 level, while the S&P 500 remains tightly pressed against the upper boundary of its ascending channel, indicating that a healthy short-term pullback is quite expected. On the other hand, market breadth indicators do not suggest an overheated sentiment. Specifically, the proportion of stocks with RSI above the threshold level stands at 8% (the threshold being 20% or higher). Similarly, the share of companies whose prices are at their four-month highs remains relatively low, around 20% (with a threshold above 40%). Thus, there is still room for growth, but the risk balance is deteriorating.

Expected Trading Range

We expect the S&P 500 Index to trade within the 6,600–6,850 range.