Investment Review №331. At zero

Review as of October 20

Global Perspective

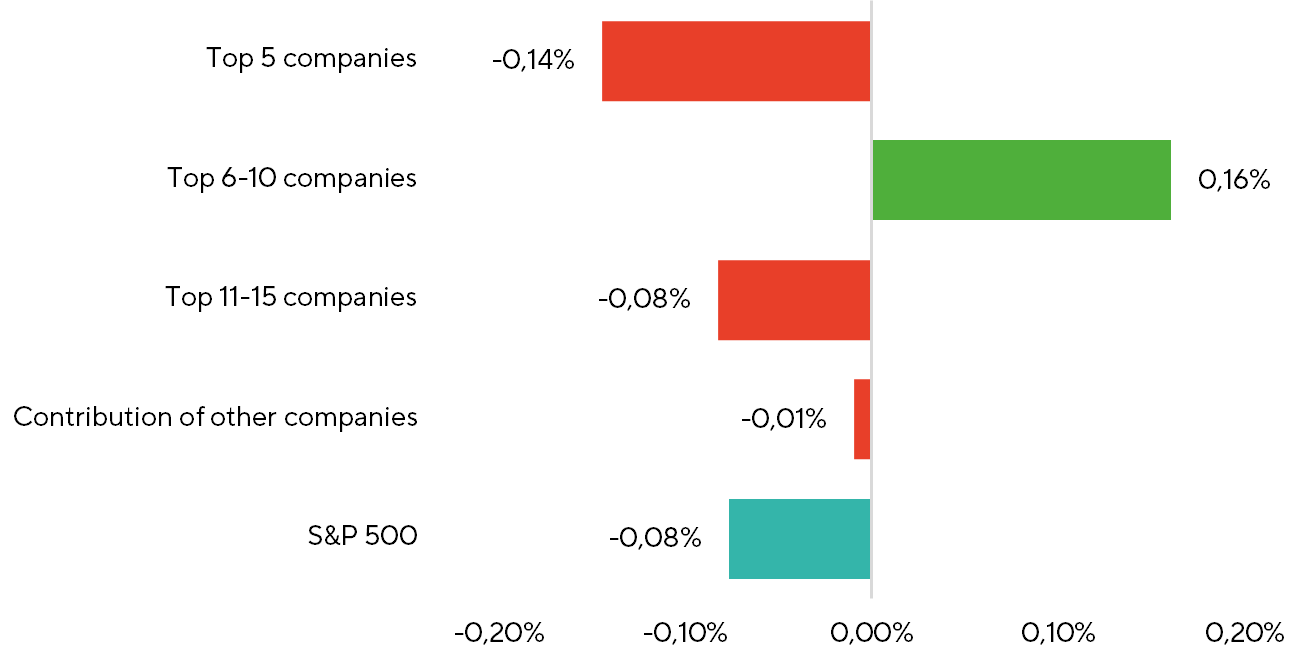

Over the two-week period, major indices displayed mixed performance: the S&P 500 declined by 0.1%, the Nasdaq 100 gained 0.7%, and the Dow Jones Industrial Average ended flat. Notably, horizontal rotation stalled, with the contribution of companies outside the top 15 remaining near zero. In contrast, the Russell 2000 small-cap index delivered positive excess returns, rising by 0.6%.

Contribution to the S&P 500 index dynamics by group

Source: FactSet, Freedom Broker

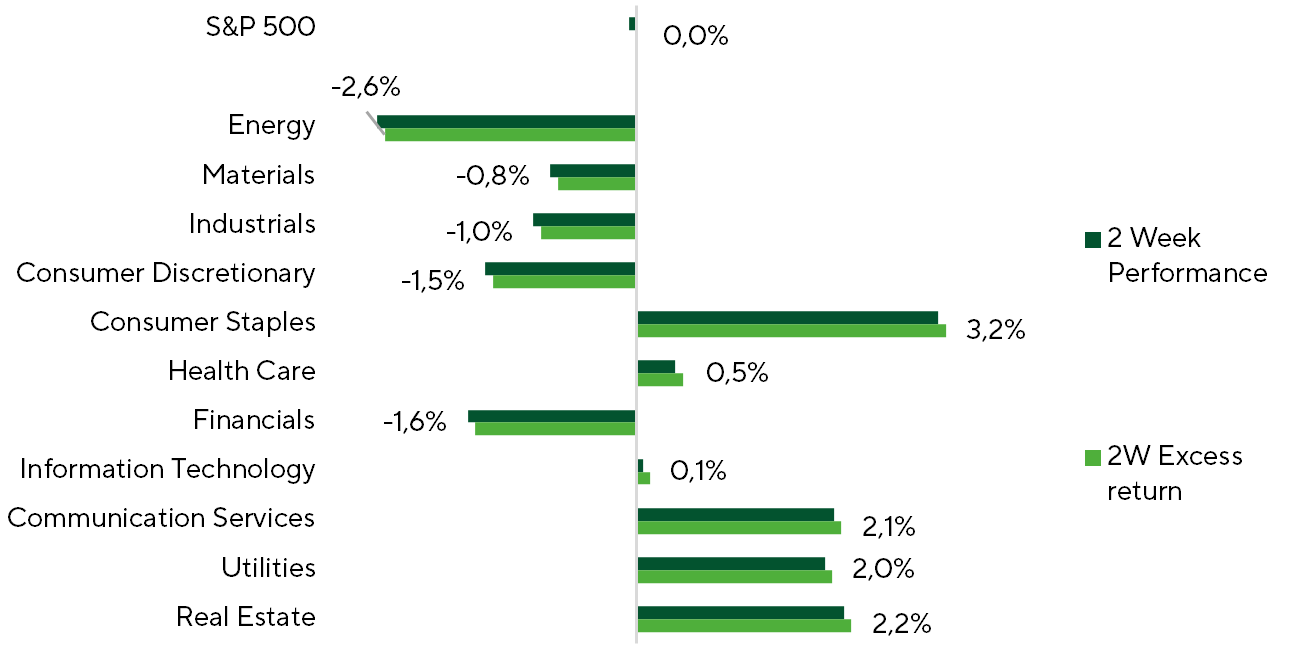

Excess returns of major US stock indices

Source: FactSet, Freedom Broker

The U.S. government shutdown continues, significantly limiting the release of macroeconomic data. As a result, markets have primarily focused on political developments and the beginning of the earnings season.

Trump remains the foremost newsmaker in the U.S., and arguably globally. His remarks on Friday, October 10, triggered a sharp sell-off in U.S. equities. He warned of the possible imposition of an additional 100% tariff on Chinese imports, in retaliation to China’s export restrictions on rare earth materials—key components for the production of a range of high-tech products. Interestingly, despite the sharp market decline, it was not accompanied by significant outflows from equity ETFs. The 100 largest Equity ETFs saw a modest loss of only $1.7 billion. The subsequent market reaction to the news was predictable—investors aggressively bought the dip throughout the following week.

Corporate Background

One of the key triggers once again came from developments in the AI market. On October 13, OpenAI and Broadcom officially announced a partnership, under which Broadcom will supply OpenAI with chips worth approximately $100 billion over the next few years, according to Citibank estimates. On Tuesday, October 14, another tech giant, Oracle, announced plans to deploy 50,000 AMD GPUs (Instinct MI450) in the second half of next year. This move underscores the continued trend of major cloud and AI providers increasingly turning to AMD products. Notably, AMD had already secured a deal with OpenAI for chip supplies. Despite weaker quarterly results from European giant ASML, with both revenue and profit falling short of expectations, management's comments that they do not anticipate revenue to decline below 2025 levels provided a boost to investor sentiment.

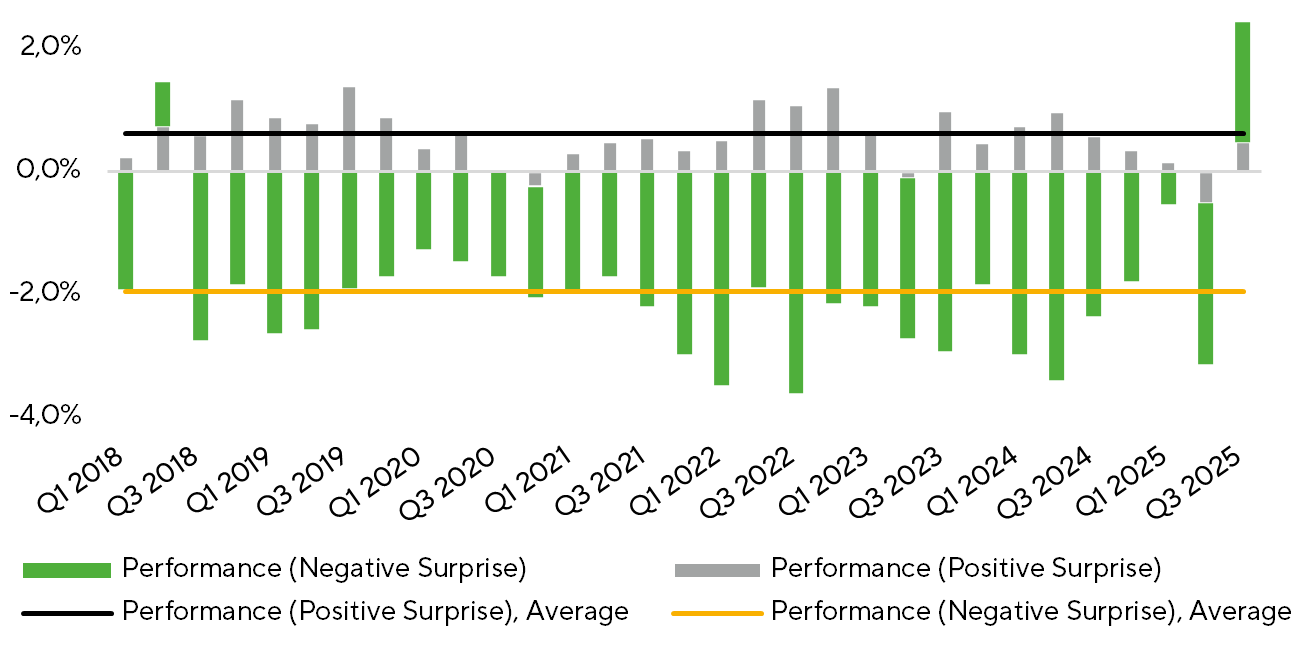

Overall, the start of the earnings season has been a key support factor for the broader market. The expected EPS growth for the companies that have reported so far stands at 8.5% for the current quarter. Additionally, there are signs of continued improvement in the profit growth composition. Specifically, 86% of companies reported positive EPS surprises, and 84% exceeded revenue expectations, both of which are above the historical averages. It is also worth noting that recent reports from major companies not only show a positive variance between expectations and actual results but also reflect a significant improvement in revenue and profit expectations for the current and next year. EPS expectations for 2025 and 2026 have been upgraded for 68% and 79% of companies, respectively, indicating that corporate quarterly results remain strong with no clear signs of deterioration or weakening profit momentum.

The reaction of stock prices to positive and negative earnings surprises

Source: FactSet, Freedom Broker

Most of the largest banks reported higher-than-expected revenue and profit figures. Despite some pressure on net interest margins at certain institutions, this was largely offset by non-interest income, driven by positive momentum in the capital markets sector, as well as growth in trading revenues and asset management profits. The asset quality at the largest banks continues to be solid, with only a few players seeing a slight uptick in non-performing assets. However, in percentage terms, these figures remain minimal. The strong performance from banks and their positive outlooks clearly signal a robust state of economic activity, something we have consistently pointed out in previous analyses.

In mid-October, markets faced renewed pressure due to the struggles of two regional banks, which had to write off loans to several borrowers. This sparked concerns over the broader quality of credit portfolios, particularly after recent bankruptcies in the auto lending sector. However, these worries were short-lived, and by the end of the week, markets had swiftly bounced back, reclaiming their losses.

Fed Policy Background

Comments from certain Fed officials did not serve as a major market trigger. However, statements from Williams, Waller, and Paulson, all expressing support for further rate cuts, helped reinforce the narrative of a proactive and accommodative policy stance by the Fed. This continues to be an important factor supporting market sentiment at present.

Market Focus

Over the next one and a half weeks, key events for the market will be the earnings reports from major U.S. companies, with a significant portion of these results expected to be released at the end of the month, including reports from members of the Magnificent Seven. In light of several recent deals among the largest tech companies, earnings reports from the big tech giants will be particularly significant, as they provide insights into the state of demand for cloud infrastructure and capital investment plans. As a result, we believe investor attention and nervousness around these companies' results could be heightened. Another factor driving market attention to the earnings reports of the Big Tech companies is their significant contribution to overall market profit dynamics. Moreover, these companies continue to show a strong trend of improving expectations.

Another key event for the market remains the Fed’s meeting at the end of October. The market is pricing in a 99% likelihood of a 25-basis-point rate cut at the upcoming meeting, with a similar probability of an additional rate cut following the December meeting. The most favorable outcome for investors would be confirmation of the narrative that economic activity remains at a sustainable level, coupled with signals of uncertainty in the labor market. In the absence of new data from the BLS, labor market assessments are expected to remain unchanged. It is unlikely that we will hear any new guidance regarding the regulator’s expectations for the current and next year. However, comments on how the Fed might act under conditions of sustained economic activity and a lack of progress in core inflation could be significant. Notably, the trajectory of supercore inflation remains a potential risk factor for market sentiment.

Overall, we maintain our previous market thesis and expect the S&P 500 to reach 6,900 points by the end of this year and 7,500 points next year. This outlook is supported by the continued stability of key factors: resilient profit dynamics, the ongoing narrative of policy easing, and expectations for improved business activity in the coming year. Despite periodic spikes in bearish headlines about a potential bubble in the tech sector, we maintain a more balanced approach, emphasizing that the higher multiples in the IT sector, relative to historical decade averages, are primarily a function of the structural acceleration in growth within the segment, rather than a detachment of investors from reality.

Small-Cap Stocks

Over the past two weeks, small-cap benchmark indices displayed a mixed performance. The micro-cap segment, led by the Russell Microcap Index (ETF: IWC), posted the strongest gain, rising 2.1%, while the Russell 2000 (ETF: IWM) saw a more modest increase of 0.5%. On the other hand, the financially stable small-cap segment, represented by the S&P Small Cap 600 Index, experienced a slight decline of 0.3%.

Despite the heightened volatility in October, market participants have been actively buying the dips, allowing small-cap indices to reach new historical highs. Specifically, on October 15, the Russell Microcap index closed at an all-time high for the first time since March 2021. However, the breadth of the rally remained limited, with only 43% of companies in the Russell 2000 and 41% in the micro-cap segment showing positive performance.

Investor focus shifted to the start of the Q3 2025 earnings season. Over the past two weeks, 34 companies from the Russell 2000 and 18 from the S&P Small Cap 600 reported their results. Early reports have been positive, with EPS expectations improving. As of October 20, the EPS growth for the S&P 600 is projected at 11.2% year-over-year (up from 10.8% in September), while the Russell 2000 is expected to see 9.1% growth (compared to 8.5% previously).

Over the next two weeks, investor attention will remain focused on earnings reports, with the pace of releases accelerating. Results are expected from 225 companies in the S&P Small Cap 600 and 468 firms in the Russell 2000. An additional factor that could influence market sentiment will be the upcoming Fed decision on interest rates. The futures market currently assigns a 96.7% probability of a 25-basis-point rate cut.

Broad Market Technical Analysis

Recent market pullbacks led to some improvement in the technical picture for the index, as S&P 500 prices moved away from the overbought zone (according to RSI) and approached the lower boundary of the ascending channel. This can be seen as a normal market reaction following an extended period of growth. At the same time, we do not see any signs of a potential deterioration in market dynamics moving forward, given the absence of technical triggers or negative signals from breadth indicators or sentiment.

Expected Trading Range

We expect the S&P 500 to move within the range of 6,600 to 6,850 points.