Investment Review №336. Choosing a direction

Corporate News In Focus of Our Analysts

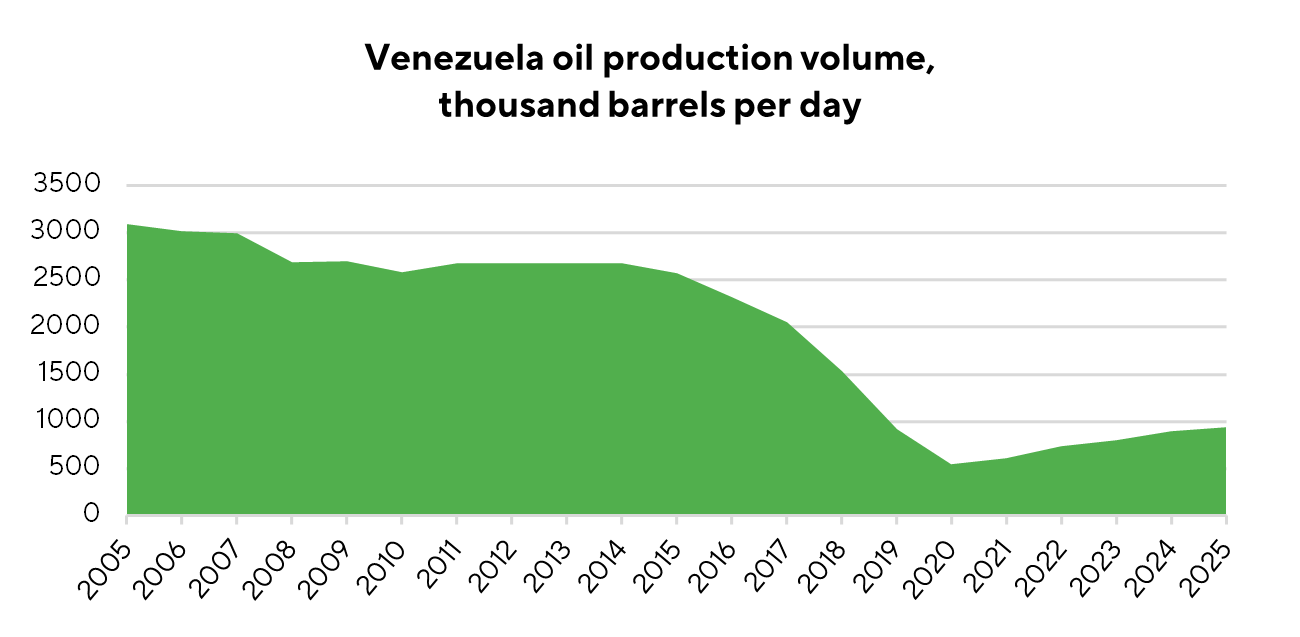

COP as a Potential Beneficiary of Venezuelan Uncertainty

The reported abduction of Venezuelan leader Nicolás Maduro by U.S. forces triggered a wave of optimism around a potential recovery of the country’s oil and gas sector. In our view, however, this optimism is overstated. With oil prices remaining low and the market facing a supply glut, investment in Venezuela’s energy sector looks economically unjustified. The idea floated by Donald Trump of subsidizing U.S. companies to develop Venezuela’s oil industry appears unrealistic and difficult to implement.

That said, one U.S. oil major could benefit directly from a regime change. ConocoPhillips could finally receive the compensation awarded to it in excess of $8 billion, equivalent to roughly 7% of the company’s current market capitalization. The claim stems from the 2007 nationalization of its assets, when the company refused to transfer control to the state and declared the move an illegal expropriation. In 2019, an international arbitration tribunal ordered Venezuela to pay $8.7 billion in damages. As a result, ConocoPhillips stands out as the primary potential beneficiary of any change in power in Venezuela. Freedom Broker’s target price for the stock is $125, with a Buy recommendation.

Sources: statbase.org, OPEC

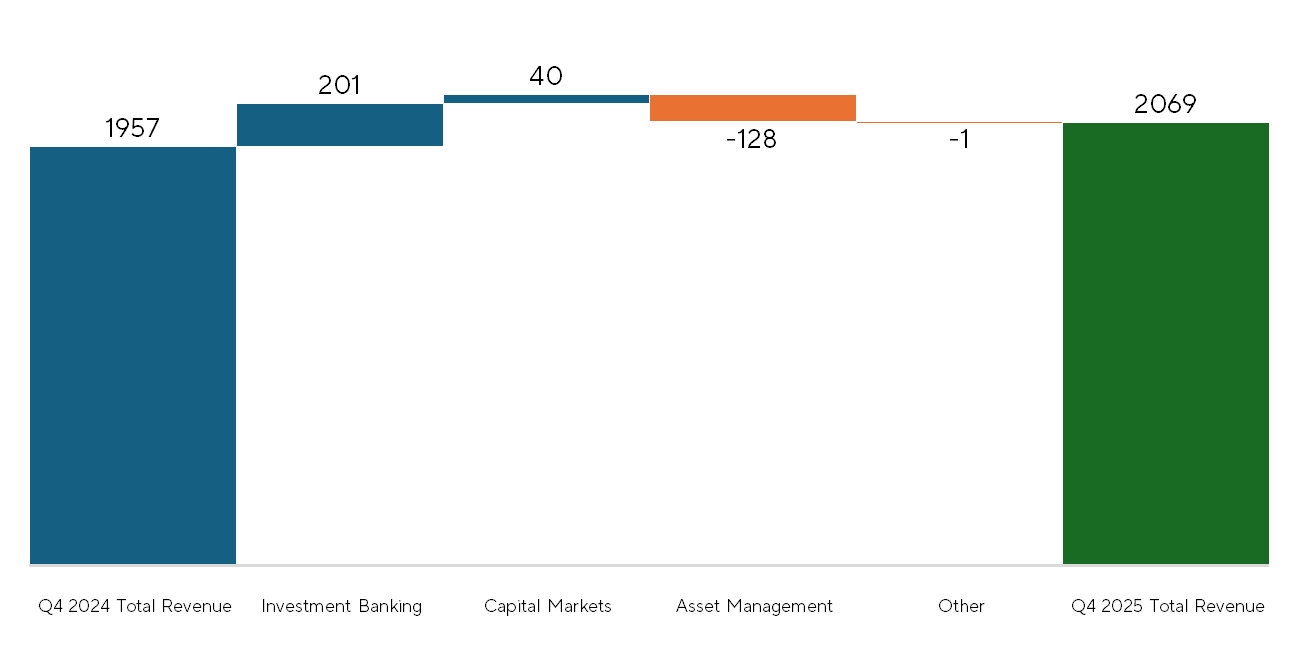

Jefferies Financial Group (JEF): Q4 FY2025 Results

Jefferies reported mixed results for the fourth quarter of fiscal year 2025 relative to market expectations. Total revenue came in at $2.07 billion, up 5.7% YoY and above consensus, while EPS was $0.87, slightly below expectations. The earnings miss was driven by a one-off item: a $30 million pre-tax loss related to the revaluation of the company’s investment in the Point Bonita fund, in which Jefferies holds a stake. Excluding this effect, adjusted EPS amounted to $0.96, up 5.5% YoY, pointing to solid underlying operating performance across the core businesses.

Investment banking was the main growth driver. Segment revenue rose to $1.19 billion, up 20% YoY, supported by market share gains and a favorable market environment. Advisory revenues were the second-highest in the company’s history, reflecting strong client activity. Equity underwriting also provided meaningful support, with a large portion of full-year revenues generated in the fourth quarter.

Capital markets revenue totaled $692 million, up 6% YoY. Equity trading revenues increased 18% YoY, while fixed income revenues declined 14% YoY amid continued pressure in credit markets. Asset management performance remained weaker, reflecting lower investment returns, including the impact from the Point Bonita fund.

Jefferies Revenue by Segment: YoY Change

Source: Jefferies Financial Group, Q4 FY2025

JNJ and ABBV Join the Price Agreement with the Trump Administration

On January 8, 2026, Johnson & Johnson (JNJ) entered into a voluntary agreement with the Trump administration to lower drug prices in exchange for an exemption from import tariffs. On January 13, AbbVie (ABBV) signed a similar agreement. For both companies, the arrangement is strategically important, as it protects them from potentially significant tariff pressure in return for relatively limited and manageable price concessions, largely concentrated in the Medicaid segment that has already been discounted. Previously in 2025, JNJ had estimated potential tariff costs, primarily related to its Medicaid business, at about $400 million. The pharmaceutical tariff exemption allows the companies to avoid substantially larger financial losses and helps reduce uncertainty over margins in key divisions.

Of the 17 pharmaceutical companies that received letters from the Trump administration in July 2025, 16 major industry players have signed the agreement. The only large company that has not yet joined is Regeneron (REGN). We expect REGN to ultimately sign it as well, given the unfavorable risk–reward profile of remaining outside the agreement.

| Company | Status | Signing date |

| Pfizer | Signed | 30.09.2025 |

| AstraZeneca | Signed | 10.10.2025 |

| Eli Lilly | Signed | 06.11.2025 |

| Novo Nordisk | Signed | 07.11.2025 |

| EMD Serono (Merck KGaA) | Signed | 16.10.2025 |

| Amgen | Signed | 19.12.2025 |

| Boehringer Ingelheim | Signed | 19.12.2025 |

| Bristol Myers Squibb | Signed | 19.12.2025 |

| Genentech (Roche) | Signed | 19.12.2025 |

| Gilead Sciences | Signed | 19.12.2025 |

| GSK | Signed | 19.12.2025 |

| Merck & Co. | Signed | 19.12.2025 |

| Novartis | Signed | 19.12.2025 |

| Sanofi | Signed | 19.12.2025 |

| Johnson & Johnson | Signed | 08.01.2026 |

| Abbvie | Signed | 13.01.2026 |

| Regeneron | Not signed |

Companies that joined the pricing agreement with the Trump administration

Source: Freedom Broker

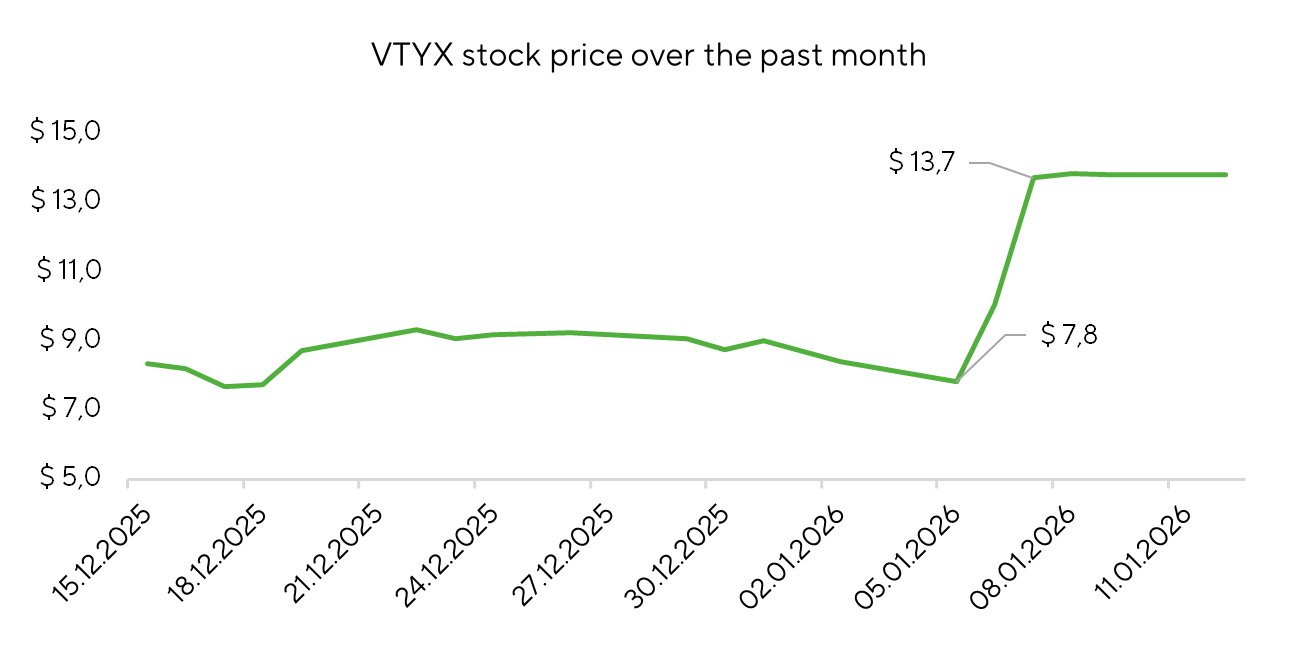

Eli Lilly Acquires Ventyx Biosciences (VTYX)

On January 7, 2026, Eli Lilly (LLY) announced it would acquire Ventyx Biosciences (VTYX) in an all-cash transaction valued at roughly $1.2 billion ($14 per share). The deal provides Lilly with a portfolio of oral anti-inflammatory drugs targeting key innate immune pathways and increases business diversification beyond its metabolic segment.

Ventyx’s lead asset is VTX3232, an oral, selective NLRP3 inhibitor currently in Phase II studies for Parkinson’s disease, obesity, and cardiometabolic indications. Tamuzimod (VTX002), a selective S1P1 receptor modulator that has completed a Phase II study for ulcerative colitis, adds further strategic value to the portfolio.

NLRP3 inhibitors are regarded as one of the most promising drug classes, with a cumulative addressable market estimated at over $100 billion across a wide spectrum of inflammatory and neurodegenerative diseases.

Источник: Freedom Broker, FactSet

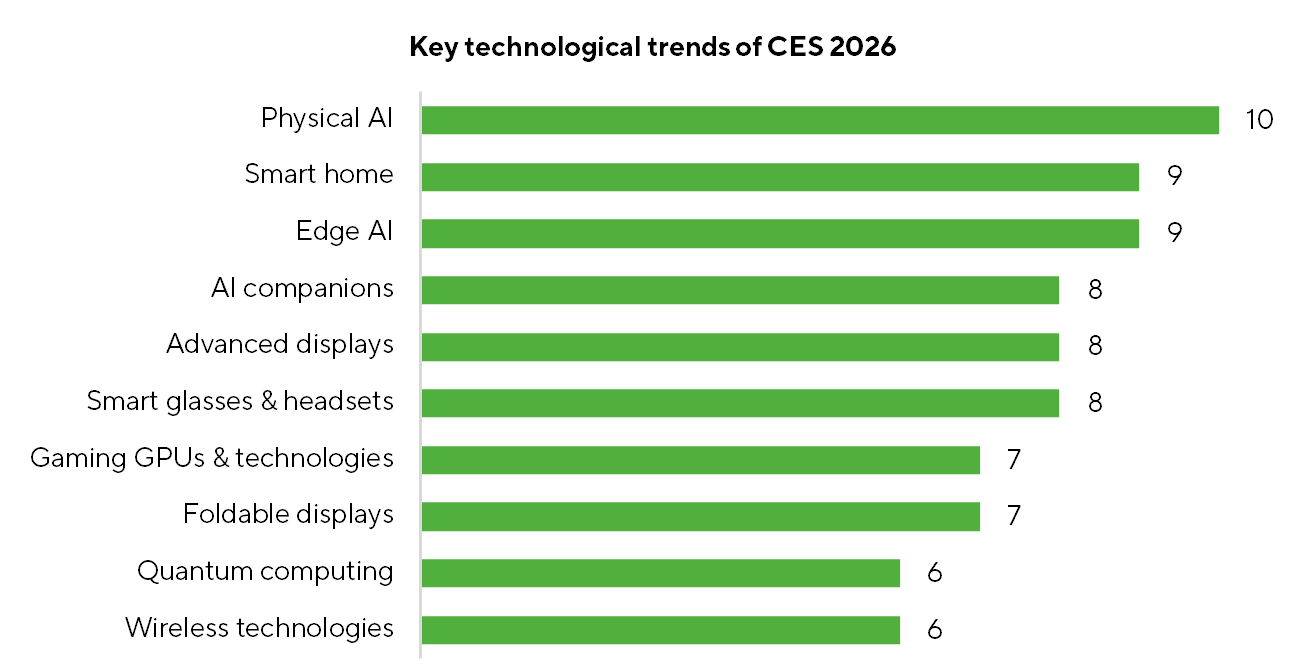

Consumer Electronics Show (CES) 2026

CES 2026 in Las Vegas, which concluded on January 9, highlighted the ongoing transformation of the technology industry. The show crystallized three key trends: a shift from cloud-based AI to edge AI to reduce latency and enhance privacy; the evolution of AI from a tool into an autonomous background system; and explosive growth in “physical AI,” spanning everything from autonomous vehicles to industrial robots. At the same time, it was notable that Dell stepped back from AI marketing, stating that consumers “don’t buy based on AI” and suggesting the term is rather confusing. While there was no shortage of new devices on display, our focus was on what Nvidia, AMD, and Intel brought to the show. Nvidia concentrated on enterprise AI and software innovation rather than consumer GPUs. The company did not announce any new gaming graphics cards, and the launch of its Super models has been postponed indefinitely. Instead, Nvidia introduced its Alpamayo platform for L4 autonomous transport and unveiled a new version of DLSS 4.5 with Dynamic Multi Frame Generation technology. Intel finally took the wraps off its Core Ultra Series 3 (Panther Lake) processors, the first consumer platform based on the Intel 18A (1.8 nm) process designed and produced in the U.S. Intel expects a 60% uplift in multithreaded performance, a 77% improvement in graphics performance, and a 2x increase in AI acceleration compared with Core Ultra Series 2. AMD made only a modest update to its lineup, introducing Ryzen AI 400 Series (Gorgon Point) processors, still based on the Zen 5 architecture and a 4 nm process. By the end of 2026, both companies are slated to unveil their new architectures, setting the stage for a much more intense competitive battle.

Sources: CES 2026, Perplexity, Freedom Broker