Investment Review №344. A Commitment to Techno-Optimism

Corporate News in Focus of Our Analysts

Apple

Apple (AAPL) reported a strong Q2 FY26 print on April 30, beating expectations across all key metrics and topping it with a more aggressive-than-expected forward guide for the next quarter. Margins remained resilient despite ongoing component shortages and input cost inflation, though management acknowledged some incremental pressure building later in the year, currently outweighed by robust top-line momentum. The company continued to gain share in key markets, most notably China, where growth materially outpaced the broader industry. This supports a more constructive medium- to long-term outlook, with both revenue and EPS trajectories warranting upward revision. A key strategic overhang—and potential catalyst—remains the transition to John Ternus as CEO, succeeding Tim Cook. The incoming leadership is viewed as more technically driven and execution-aggressive, closer in style to Steve Jobs, potentially sharpening Apple’s response to rapid technological shifts. However, execution risk rises materially in early tenure, and leadership transitions typically embed a higher risk premium and near-term volatility in valuation as investors reprice governance uncertainty.

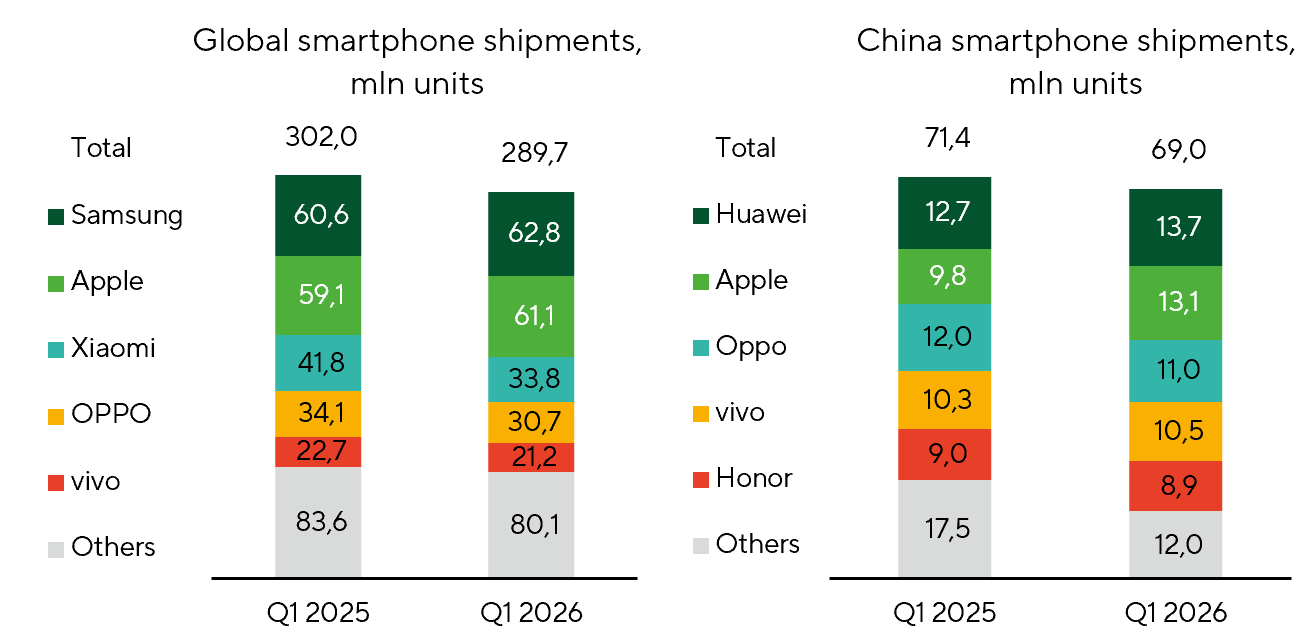

Smartphone supplies.

Source: IDC, Freedom Broker

Intel

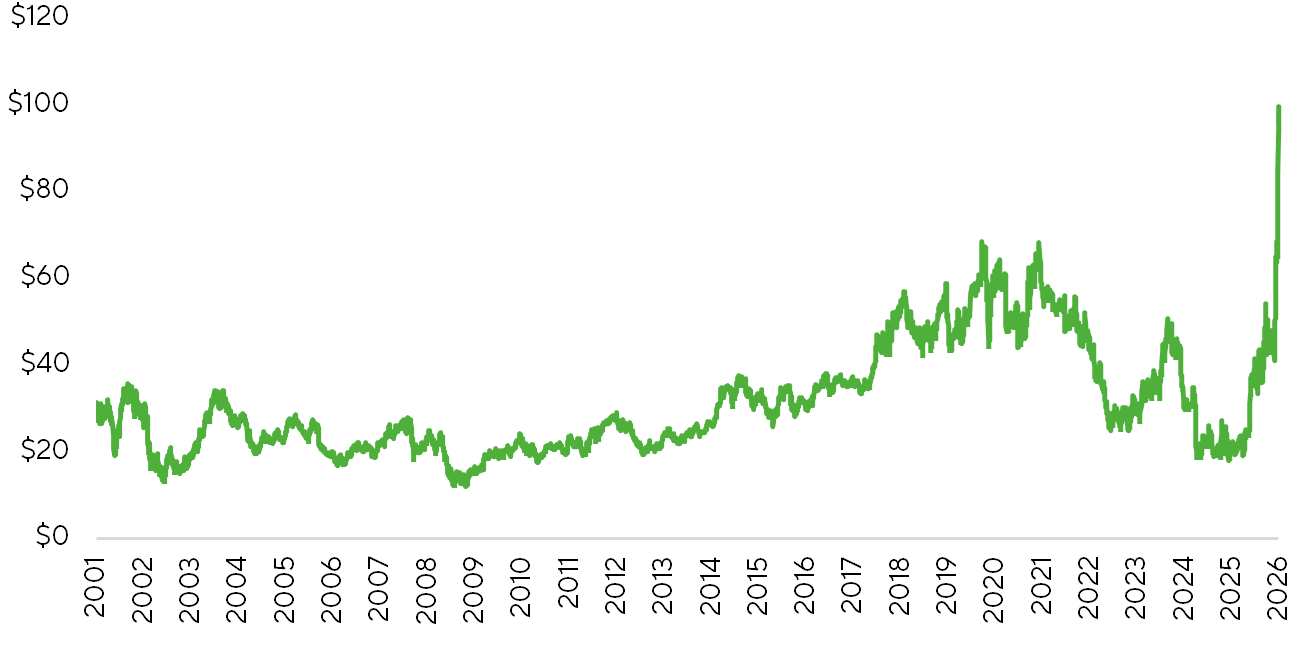

Intel (INTC) reported a strong Q1 FY26 print on April 23, marking a convincing inflection point in the “new Intel” narrative under Lip-Bu Tan. The company materially beat expectations on revenue, gross margin, and EPS, while management guidance notably reinforced—rather than undermined—investor conviction for the first time in several quarters. Demand continued to run ahead of supply across all business lines, with a structural shift toward AI-related revenue (~60% of total, +40% YoY) providing both a coherent growth narrative and tangible commercial validation. The Data Center & AI (DCAI) segment remained the primary driver of upside, supported by multi-year agreements with Google on CPUs and ASICs, a CPU supply contract for NVIDIA DGX Rubin systems, and collaboration with SambaNova. Momentum in the foundry business also strengthened, with yield on the 18A node tracking ahead of plan and early signals from 14A remaining encouraging. Guidance for advanced packaging was upgraded from “hundreds of millions” to a “multi-billion” opportunity. Strategic partnerships under the Terafab initiative with SpaceX, xAI, and Tesla, alongside increasingly credible speculation around Apple, added incremental upside optionality. INTC shares surged to their highest levels in 25 years.

Share price dynamics of Intel Corp. (INTC) over the past 25 years, $

Source: FactSet, Freedom Broker

UnitedHealth, Molina Healthcare, Centene Corporation, Humana, The Cigna Group

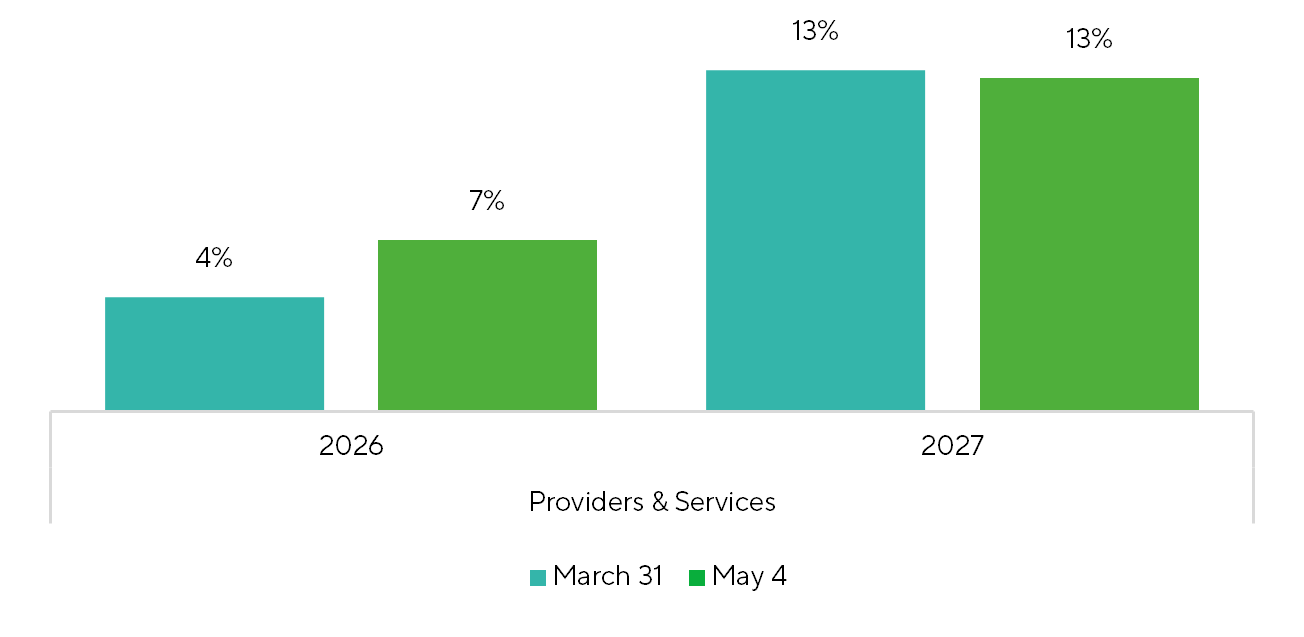

Healthcare Providers & Services delivered a better-than-expected Q1 2026 earnings season, though underlying quality was mixed: strength in managed care contrasted with softness in hospitals and select service providers. The key positive surprise came from Medical Loss Ratio (MLR) performance among insurers, where major players—UnitedHealth Group (UNH), Molina Healthcare (MOH), Centene (CNC), Humana (HUM), and Cigna (CI)—all printed better-than-expected MLRs. The market read-through was constructive, suggesting premium pricing is finally catching up with underlying medical cost inflation. This drove a sharp re-rating across the group, with CNC and MOH both up 14% post-earnings. Hospital operators underperformed, with a weaker respiratory season weighing on utilization and driving softer admission trends—HCA Healthcare down 8.8% and Universal Health Services off 9.5%. Looking ahead to FY26, the sector’s key upside drivers remain pricing discipline among insurers, stabilization in Medicaid/Medicare margins, and incremental operating leverage. Offsetting these are persistent headwinds from MLR normalization and underlying cost inflation trends, ongoing regulatory uncertainty around ACA/Medicare frameworks, and continued volatility in hospital utilization patterns. The market has turned more constructive on FY26 EPS growth for the sector, and we maintain a positive stance into 2026.

Changes in EPS Growth Expectations in Healthcare Providers & Services

Source: FactSet

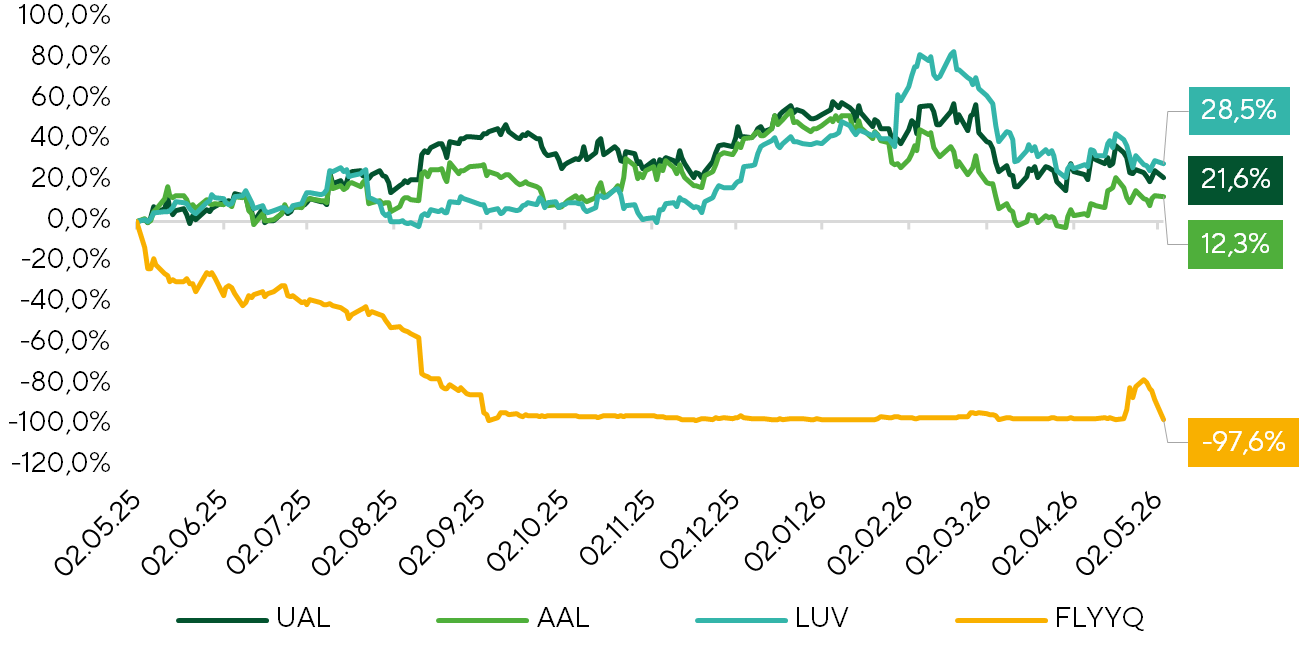

United Airlines, American Airlines, Southwest

U.S. airlines entered the Q1 2026 reporting season with unexpectedly resilient results despite a fuel-cost shock, though dispersion across carriers has widened as strategies diverge materially. United Airlines Holdings and American Airlines Group both posted revenue growth and margin expansion, supported by premium cabin strength and loyalty programs. Importantly, both carriers demonstrated pricing power by passing a meaningful portion of higher fuel costs through to passengers, while also initiating selective capacity reductions to defend unit profitability and sustain yield per seat. In contrast, Southwest Airlines is undergoing a more structural model shift. The carrier delivered record quarterly revenue and a return to profitability, driven less by traffic expansion and more by aggressive monetization of ancillary offerings—premium seating with additional legroom, fare segmentation, and a stronger push into corporate demand. This shift has already translated into double-digit RASM growth and improved profitability, albeit still against a structurally lower load factor base.

Against this backdrop, Spirit Airlines highlights the downside of the ultra-LCC model. One of the oldest U.S. low-cost carriers and an early pioneer of the ultra-low-cost structure announced a full wind-down of operations, ceasing all flights on May 2, 2026. The decision marks the culmination of a prolonged financial deterioration: Spirit has not generated sustainable profitability since 2019, steadily accumulated leverage, and entered Chapter 11 bankruptcy protection twice—ultimately failing to execute a credible balance sheet and fleet restructuring.

The final catalyst was a sharp spike in jet fuel prices following the escalation of the Middle East conflict, which compressed already-thin unit economics. With an inherently low-margin, highly price-sensitive demand base, the model proved unable to absorb the cost shock. An attempt to stabilize the carrier via a $500m financing package ultimately failed after bondholders refused to participate, forcing Spirit—already in its second Chapter 11 process—into an orderly wind-down. All operations have since been terminated, with ~17k employees laid off, while customers are being offered cash refunds on purchased tickets, but without rebooking options onto alternative airlines.

AAL - $16, buy

UAL - $125, buy

LUV - $58, buy

Airline Carrier Stock Performance (YoY Change)

Source: FactSet

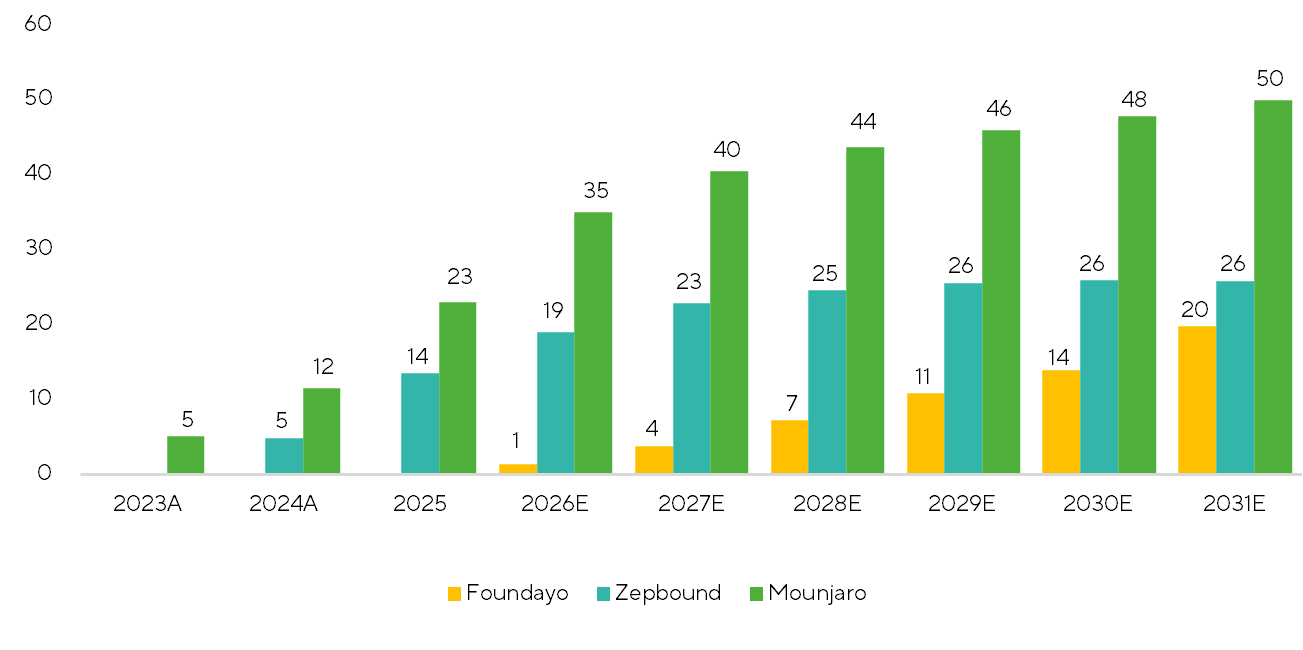

Eli Lilly

Eli Lilly’s (LLY) quarterly results once again exceeded even the most optimistic expectations. Revenue for the reporting quarter came in at $19.8 billion, up 55.5% year over year, and well above our forecast of $18.1 billion. Mounjaro sales reached $8.6 billion, up 125% year over year, significantly exceeding our estimate of $7.2 billion and serving as the main driver of the upside.

Mounjaro’s performance was so strong that it exceeded not only the analyst consensus by $1.4 billion, but even the market’s most bullish expectations. A strategically important development during the quarter was the approval of Foundayo, whose commercial launch had already begun in the second quarter. The non-incretin portfolio is also showing signs of recovery, supported by the momentum of newer drugs.

At the same time, the company is actively strengthening its base of long-term assets beyond GLP-1, stepping up its M&A activity and announcing the acquisition of four companies with a combined deal value of more than $20 billion. Following these impressive results, the company significantly raised its full-year guidance. Investors responded positively to the earnings release, with the stock rising more than 10% after the report.

Expected Sales of GLP-1 from LLY, billions $

Source: FactSet