Investment Review №345. Treasuries vs Stocks

Inflation Risks Move to the Fore

Markets Caught Between Inflation and Slowdown in Trade

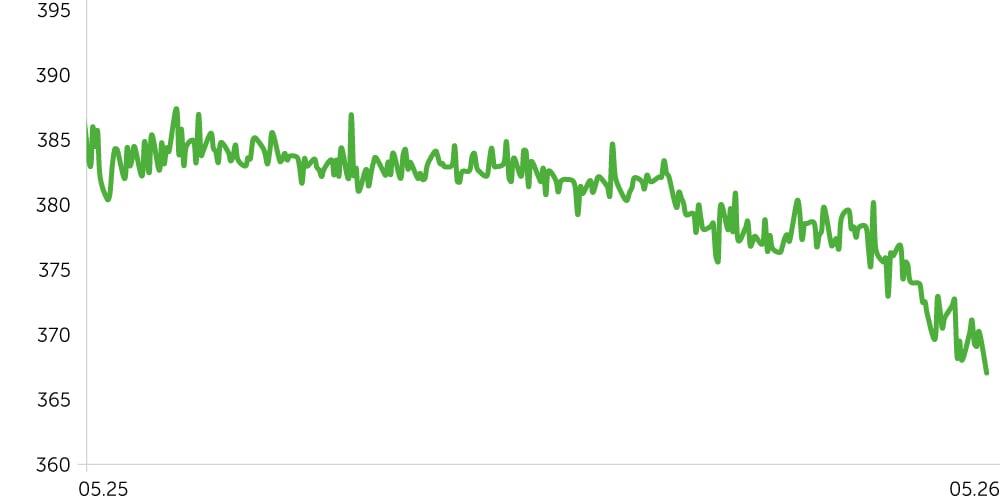

Telecom Armenia Stock Performance (Post-IPO)

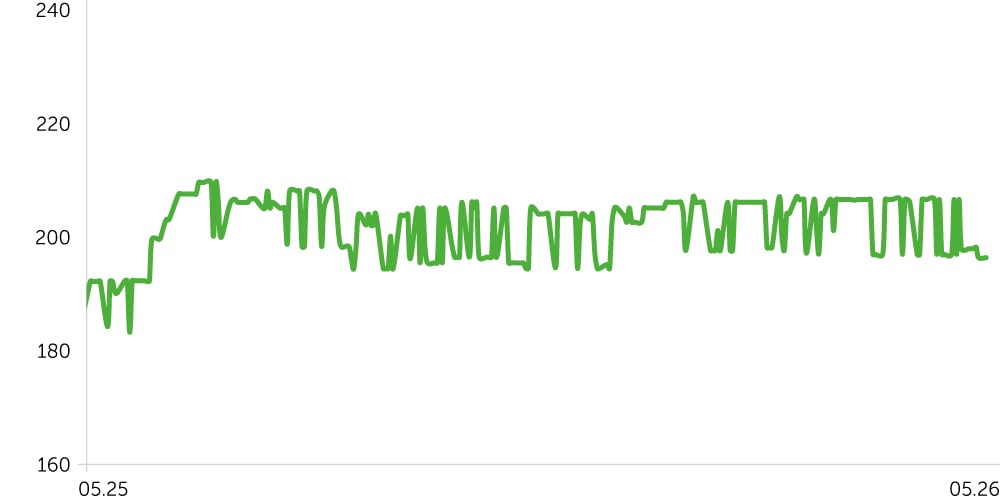

ACBA Bank: 1-Year Stock Trends

USD/AMD: 1-Year Dynamics

3-Year Corporate Bond Index (AMD) – Post-Update

From May 4 to 18, 2026, Armenia’s equity market experienced mixed trends amid mounting inflation pressures. Telecom Armenia (AMTL) edged down 0.3%, while ACBA Bank gained 2.6%, lifting its YTD return to 11.9%. ACBA continues to attract interest, likely supported by rising expectations of monetary tightening, which would bolster the bank’s interest income. The probability of a rate hike has increased as April inflation accelerated, breaching the upper bound of the Central Bank’s 3% ±1 pp target band. As expected, price growth persisted, underpinned by external inflationary pressures stemming from global logistics disruptions linked to tensions in the Middle East. Macro data suggests a modest cooling in trade/business activity: in March, foreign trade contracted on weaker exports, widening the trade deficit, while domestic trade was broadly flat as wholesale volumes declined.

The 3-year Corporate Bond Price Index was stable, indicating a wait-and-see stance amid rising inflation risks and an unchanged CBA refinancing rate. That said, higher odds of near-term tightening alongside persistent price pressures could weigh on local fixed-income prices. The dram appreciated by 1.4% despite signs of a wider trade deficit, likely supported by stable FX inflows from other sectors and an 11.7% increase in non-commercial remittances in March.

Economic Updates

Between May 4 and 18, 2026, the macro statistics flow was limited. Key data included maintaining the refinancing rate at 6.5% despite annual inflation accelerating to 5.3% YoY, and a broad-based decline in both external and domestic trade activity.

- Armenia’s inflation accelerated to 5.3% YoY in April (+1.3% MoM), up from 4.5% a month ago and above the expected 4.7%. The deviation from the CBA’s 3% ±1 pp target band widened, signaling mounting price pressures. Food remained the key driver (+9.5% YoY; +2.8% MoM), while service prices rose 2.6% YoY and were flat MoM. Externally, ongoing Middle East tensions continue to buoy oil prices (above $100/bbl). This mix of data could prompt the regulator to tighten monetary conditions in the near term.

- Armenia’s foreign trade turnover fell 6.8% YoY and 13.1% MoM in March 2026, pointing to cooling momentum. March’s exports declined 12.6% YoY and 19.9% MoM, while imports were down 3.2% YoY and 8.7% MoM. As a result, the trade deficit widened to $451m. Given recent media reports of restrictions on imports of Armenian-made goods (flowers, food, etc.) into some markets—and suspensions of sales via marketplaces such as Wildberries and Ozon—the deficit could widen further in the near term, exerting mild pressure on the dram and overall economic activity.

- Domestic trade turnover rose just 0.2% YoY in March, a marked slowdown from prior months (+5.6% in February) though a strong seasonal 14.1% MoM increase was recorded. The wholesale segment (63.6% of total) contracted 3.4% YoY despite a 14.2% MoM gain, while retail remained solid (+8.1% YoY; +14.1% MoM). Weakness in wholesale may reflect one-offs but warrants monitoring; if sustained, it would signal some cooling in domestic consumption.

Corporate News

Electric Networks of Armenia reported procurement savings of over AMD 4.5bn (~$12.2m) under its 2026 investment program (total program budget is AMD 46.7bn (~$127m)). That said, uncertainty around potential nationalization persists, keeping the company’s bond yields under upward pressure.

Two-Week Outlook

Between May 22 and June 1, 2026, market focus will center on a heavy slate of April macro data and revised figures for Q1. Key releases include the Q1 GDP growth rate (forecast: +4.1% YoY) and the April economic activity index. The latter may come in softer, judging by already released monthly data, but this probably reflects transitory factors and is unlikely to have any material impact on investor sentiment.

May CPI, April trade balance, and several related indicators are also on the calendar. Inflation will attract the most attention; if price pressures remain elevated, expectations for the rate path/monetary policy could become more volatile. The impending risk of monetary tightening may weigh on market sentiment, particularly across debt instruments.