Investment Review №332. The Bulls switched to big tech

On the green wave

Positive macroeconomic data supported instrument prices on local stock markets

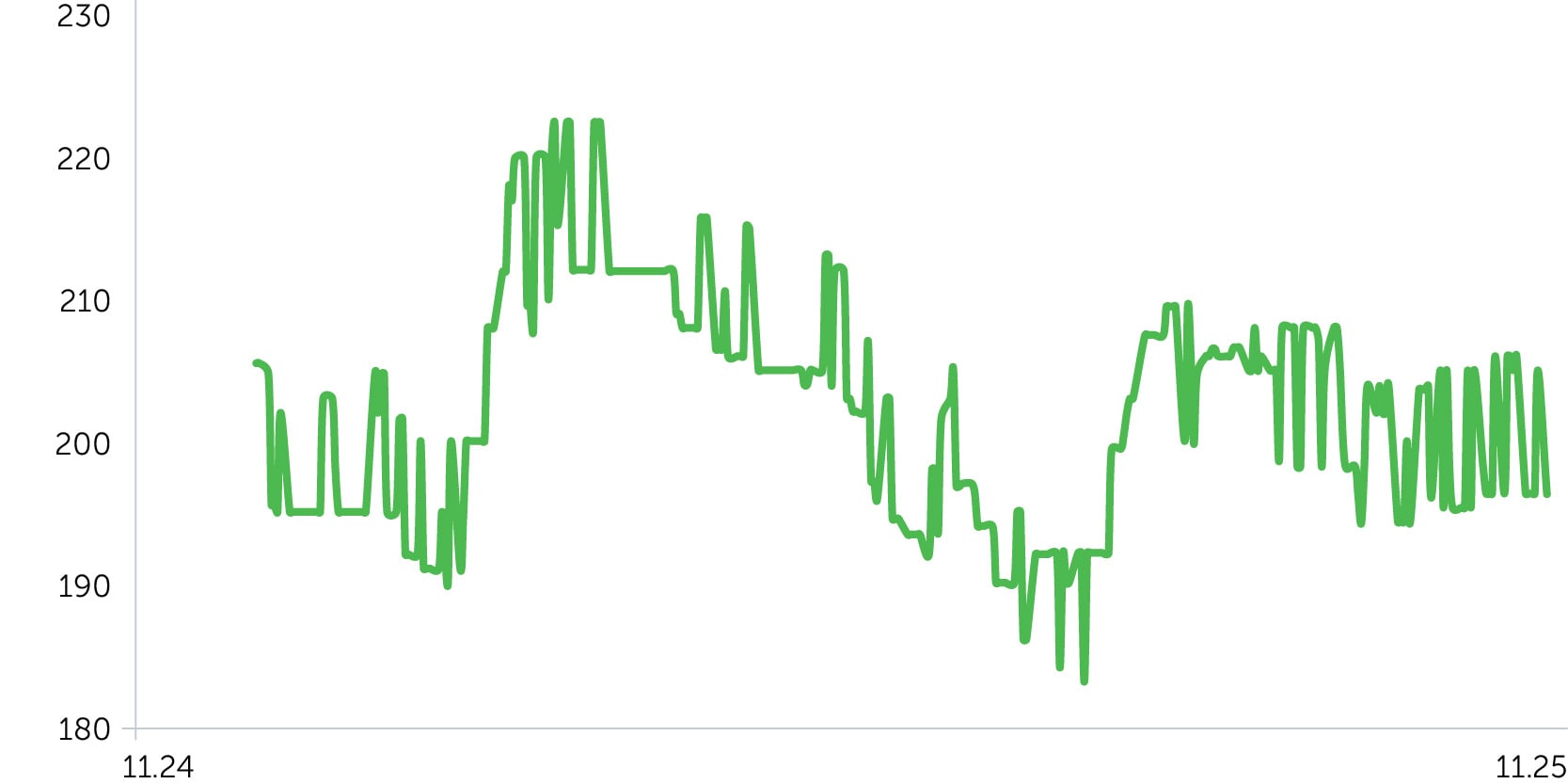

Telecom Armenia: 1-Year Stock Trends

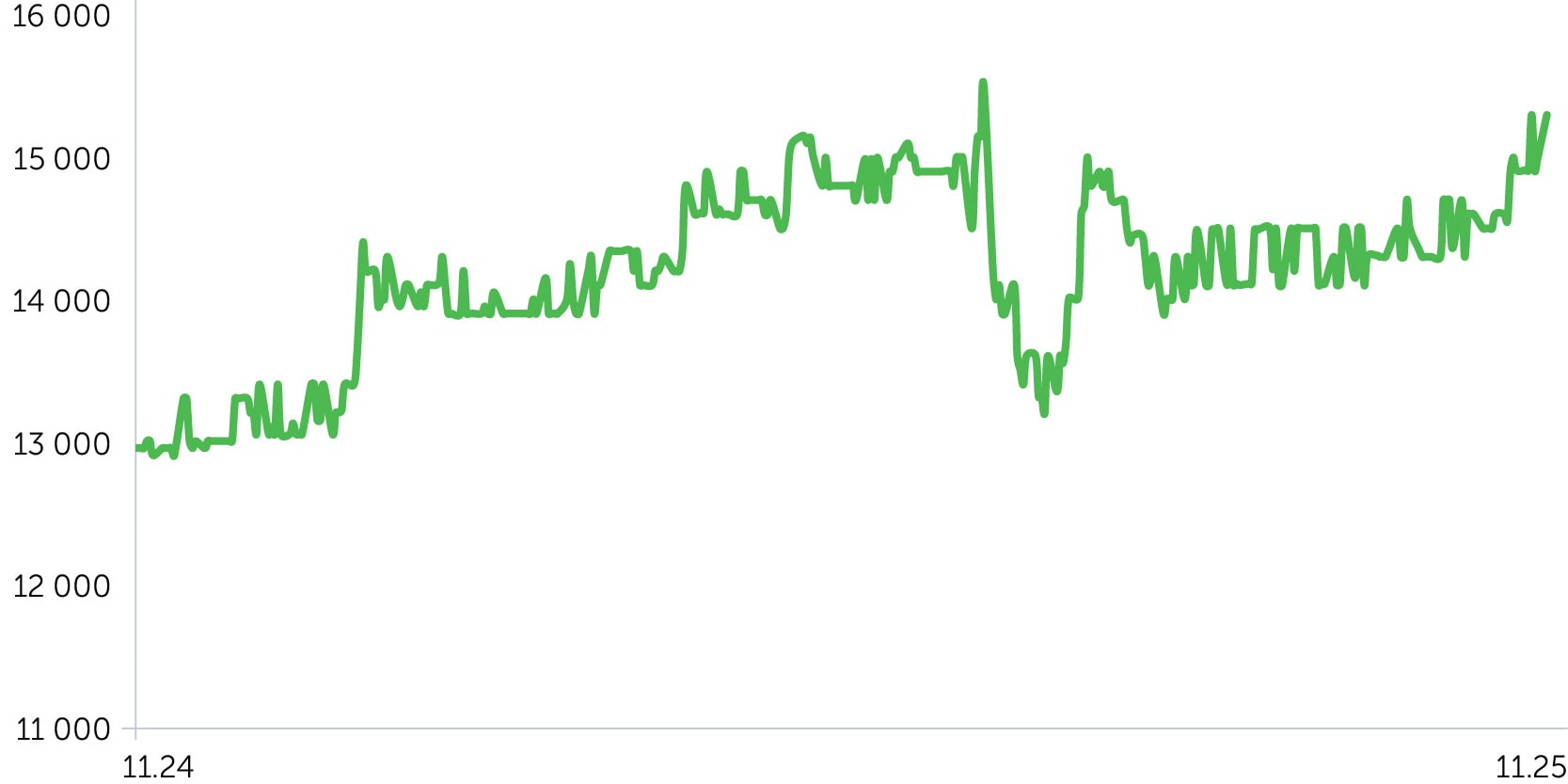

ACBA Bank: 1-Year Stock Trends

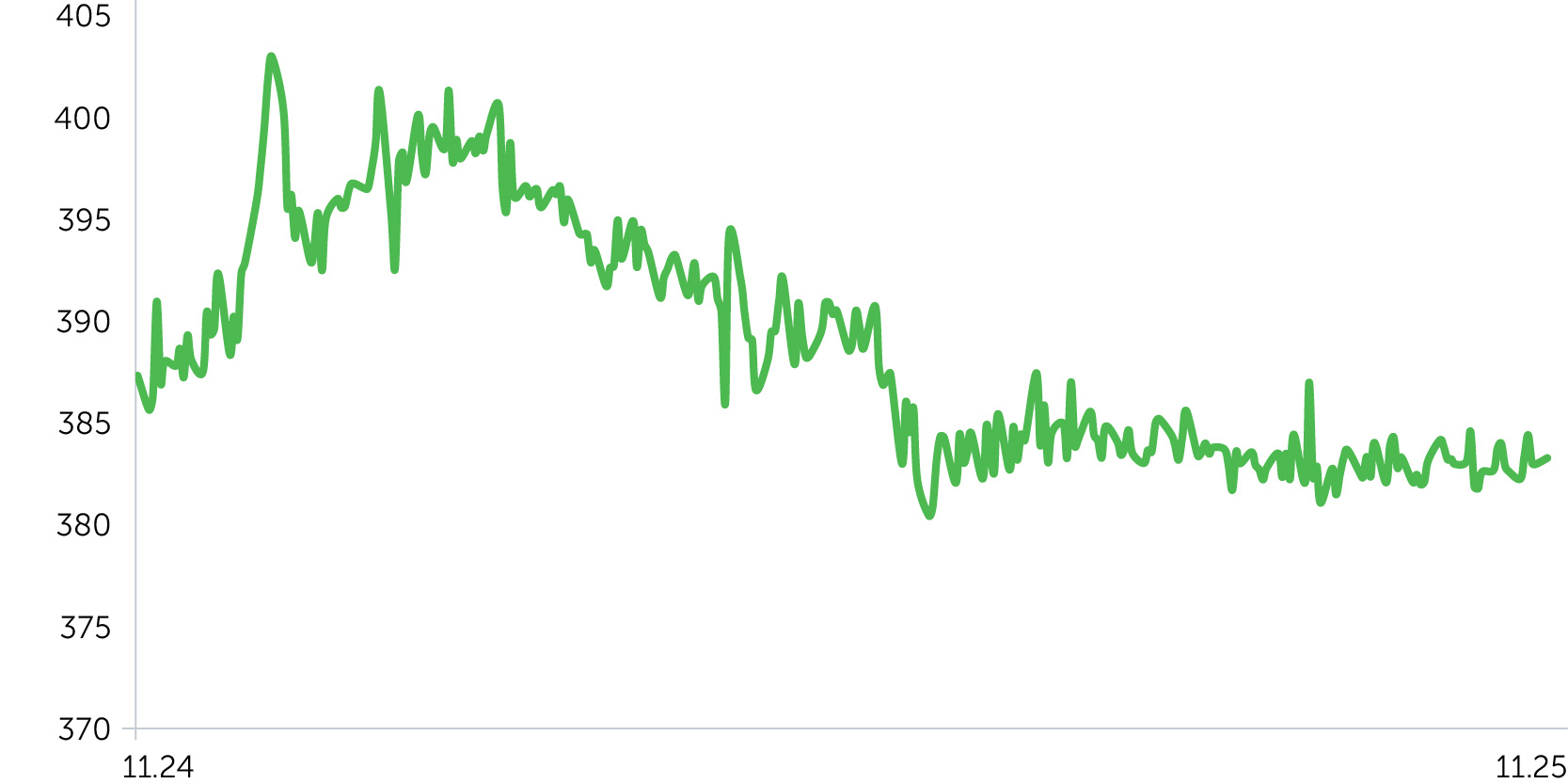

USD/AMD: 1-Year Dynamics

Between October 20 and November 3, 2025, shares of Acba Bank (ACBA) rose by 4.8%. The rally was likely driven by improved market sentiment following stronger-than-expected economic activity data for September, stable interest rates supported by the Central Bank of Armenia’s decision to keep its policy rate unchanged at 6.75%, and a steady recovery in key macroeconomic indicators. These factors may have strengthened investor interest in the banking sector. However, shares of Telecom Armenia (AMTL) remained flat over the period, likely due to the absence of meaningful catalysts and the fact that business activity in the services and consumer sectors lagged behind other industries. Tell Cell (TLCL) shares declined by 4.5% during the period, marking a 15% drop since the company’s IPO in 2024. The weakness is likely due to fundamental pressures on TLCL’s operations, which continue to weigh on its stock performance.

The price index of three-year corporate bonds denominated in drams remained stable, trading within the recent months’ range and posting a modest gain of 0.1%. The increase reflects a neutral monetary policy stance and inflation remaining within the central bank’s target range. The trend was also supported by a general decline in the domestic yield curve in recent weeks, reflecting global sentiment toward emerging markets and a possible reduction in perceived country risk.

The Armenian dram remained stable against the U.S. dollar (+0.2%). If the trend of rising net exports continues, a moderate appreciation of the national currency can be expected going forward, assuming other conditions remain unchanged.

Economic Updates

Between October 20 and November 3, 2025, Armenia’s macroeconomic dynamics were marked by a pickup in external trade flows—particularly exports—and accelerating economic activity, especially in construction, manufacturing, and services. These trends point to a continued stable growth trajectory for the Armenian economy. Meanwhile, the Central Bank maintained its wait-and-see approach, once again leaving the policy rate unchanged amid steady inflation conditions within the target range.

- Armenia’s Economic Activity Index rose by 10.5% year-over-year and 9.8% month-over-month in September, significantly outperforming expectations of a 6.0% annual increase. The growth was primarily driven by strong momentum in construction (+22% y/y), manufacturing (+10.1% y/y), and services (+7.9% y/y). Industrial output showed improvement in September, rising by 10.1% year-over-year and 5.1% month-over-month, mainly driven by a rebound in several manufacturing segments. The construction sector accelerated its growth to 22% y/y and 6.7% m/m. Meanwhile, the services sector declined by 2% y/y in September, although it has remained in positive territory since the beginning of the year, reflecting some volatility in consumer and business services. That said, risks of a slowdown in construction persist amid price adjustments in the local real estate market.

- Armenia’s net exports in September came in stronger than expected, improving from -$357 million to approximately -$285 million. Exports declined by 24.4% year-over-year (vs. -40.8% in August), but rose 11.9% month-over-month. Imports fell by 19.5% y/y (vs. -28.3% in August) and edged down 0.2% m/m. Overall, the data points to a gradual normalization of monthly dynamics and a moderation in the pace of year-over-year declines. The continued double-digit contraction in external trade on an annual basis is largely attributed to the high base effect from 2024, when the country was actively used as a transit hub for the re-export of (semi-)precious metals, primarily from Russia.

- As expected, the Central Bank of Armenia kept the refinancing rate unchanged at 6.75%. Overall, rate stability—combined with moderate inflation and accelerating economic activity—supports real interest rates in the economy and may stimulate demand in fixed-income markets.

- Net foreign direct investment (FDI) inflows into the Armenian economy totaled AMD 47.95 billion in the first half of 2025, implying an increase to 0.6% of annual GDP—up from a historic low of nearly 0.3% of GDP in 2024. The funds were primarily directed toward the mining industry, aviation, and wholesale trade. While the recovery in FDI inflows is a positive signal, the current level still lags significantly behind regional peers and Armenia’s own historical benchmarks. For comparison, Azerbaijan attracted $3.2 billion in FDI during the same period (+8.2% y/y), equivalent to roughly 4.5–5% of annual GDP. Georgia recorded $763.8 million in inflows in the first half of 2025, amounting to approximately 3.5–4% of annual GDP. The weakness in Armenia’s FDI performance is partly explained by ongoing geopolitical uncertainty, the relatively small size of the domestic market, and limited diversification of investment inflows.

Corporate News

D. Kazinyan, former acting CEO of Electric Networks of Armenia (ENA), pointed to the potential revocation of the company’s license on political grounds. The administrative proceedings initiated by the Public Services Regulatory Commission (PSRC) on July 18 are expected to conclude by November 18. If the license is revoked, under the Energy Law, the owner must be offered a buyout at market value with a 15% premium. The news may negatively impact investor sentiment and put pressure on ENA’s bond prices, although much of the downside risk is likely already priced in.

Two-Week Outlook

Between November 7 and 17, a limited set of macroeconomic data releases is expected in Armenia. However, the potential publication of revised or updated statistics is unlikely to materially affect the assessment of the current economic environment.

The key release will be the third-quarter GDP data, which is expected to show an acceleration in growth from 4.6% to 5.9% year-over-year. Market participants will be closely watching the performance of individual sectors. Should GDP growth exceed expectations, it could have a positive impact on market sentiment. Investors will closely monitor changes in the sectoral composition of GDP, with construction, services, and industry acting as key growth drivers. Additional market signals include the Central Bank’s stable monetary policy—maintaining the benchmark rate at 6.75%—and subdued inflation below expectations, both of which may support demand for equities and fixed-income instruments in the local market.