Investment Review №334. Customer return

UAE market Cooling period

An ambiguous external backdrop and oil price correction sent local stock indices into negative territory.

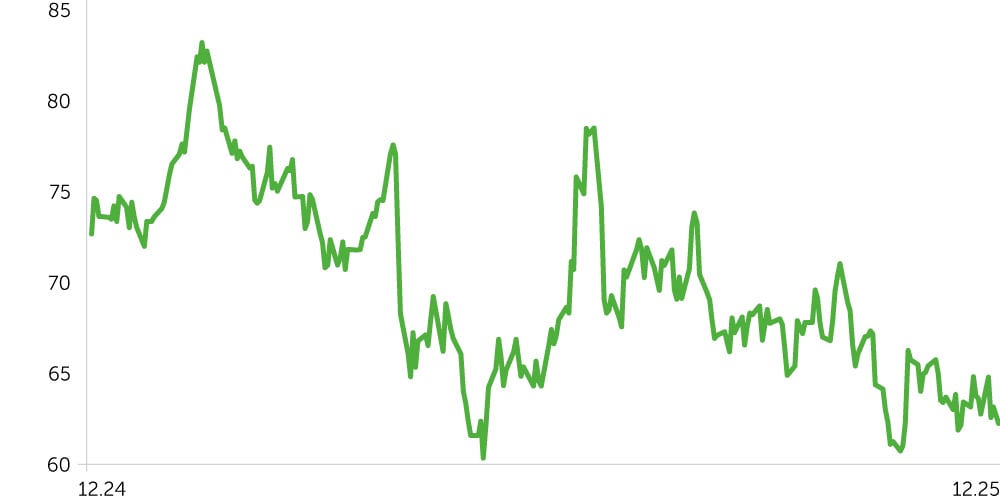

Between November 18 and December 1, 2025, UAE equity markets posted moderate declines, pressured by weakness in global stock markets and a modest pullback in oil prices. The DFM General Index (DFMGI) fell 2.0%, while the FTSE ADX General Index (FADX) lost 1.7%. Over the same period, Brent crude slipped 1.4% to $62.3 per barrel, reflecting demand concerns amid expanded OPEC+ quotas. By contrast, the S&P 500 advanced 2.6% during the same timeframe, highlighting a divergence between UAE markets and major developed‑market benchmarks.

Sector performance was mixed during the two-week stretch. The Financials sector declined an average of 1.5%, while Energy fell 2.45%. The defensive Utilities sector also slipped 2.85%, broadly in line with the overall market. The exception was Consumer Staples (food products), which posted an average gain of 3.31%, supported by Agthia Group (+11.94%). Most major banks came under pressure: First Abu Dhabi Bank (FAB) dropped 6.82%, Emirates NBD Bank fell 5.79%, and Abu Dhabi Islamic Bank lost 6.84%. The weakness reflected both profit‑taking after strong 3Q gains and a reassessment of risks tied to large capital transactions, notably RBL Bank investments

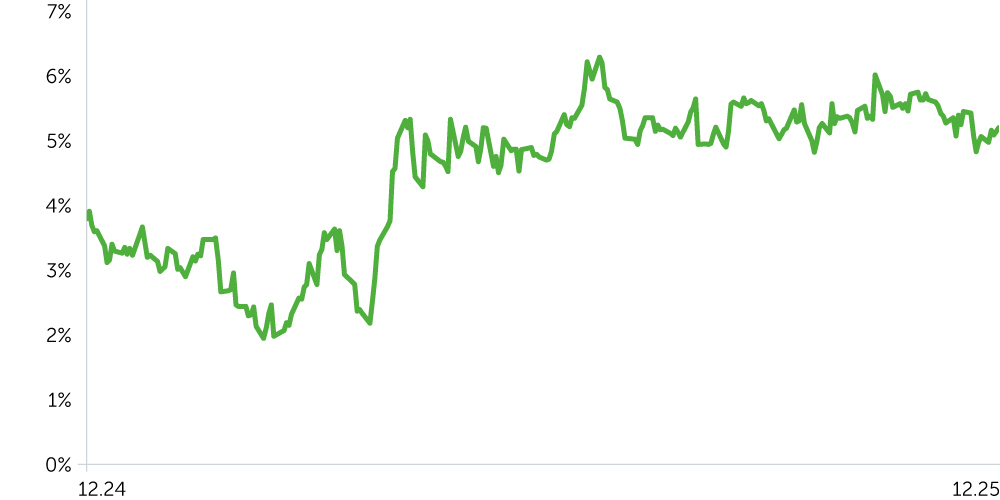

Yields on UAE Treasury bonds fell 22 basis points to 5.27%, while U.S. Treasuries edged down 3 basis points to 4.27%. The resulting 19‑basis‑point narrowing of the UAE–U.S. spread reflects a decline in the risk premium for the UAE market, supported by stable macroeconomic dynamics in the region.

DFM General Index: 1-Year Dynamics

Abu Dhabi Securities Exchange index, 1-Year

Yield, Forward Rate 1m10y, UAE, 1-Year Dynamics

Brent Oil, 1-Year Dynamics

Economic Updates

- The President of the UAE approved a debt-relief initiative for 1,435 citizens, totaling AED 475.154 million, through the Defaulted Debts Settlement Fund. The measure reduces household leverage and has the potential to improve the quality of retail loan portfolios in the medium term. It also supports social stability and indirectly benefits the consumer lending segment of major banks such as First Abu Dhabi Bank (FAB), Emirates NBD, and ADCB.

- OPEC+ confirmed its decision to suspend further increases in oil production quotas for January–March 2026. Members noted that the previously reduced volume of 1.65 million barrels per day could be restored depending on market conditions. The next meeting is scheduled for January 4, 2026.

Corporate News

- ADNOC Gas (ADNOCGAS: −3.3%) signed a landmark 20‑year natural gas supply agreement with EMSTEEL, valued between $3.5 billion and $4.2 billion. The deal secured stable deliveries of low‑carbon natural gas to support operations and future growth for one of the region’s largest steel producers.

- First Abu Dhabi Bank (FAB: −6.82%), the UAE’s largest bank, partnered with the UAE Embassy in London to hold its first career forum for Emirati students studying in Europe. The event, held on November 29–30, aimed to connect students with leading UAE companies and provide pathways to employment through elite graduate programs.

- Emaar Properties (EMAAR: −1.48%), a major real estate developer, is moving forward with new projects in Dubai, signaling confidence in long-term property demand. New initiatives, including Dubai Square in the Dubai Creek area, focus on creating large-scale residential and commercial zones with advanced infrastructure.

Two-Week Outlook

Uncertainty is still running high in the oil market, and geopolitical events could move prices further. Fundamentally, the risks lean toward lower crude prices. OPEC+ has boosted quotas by 2.88 million barrels a day since the start of the year, with production steadily increasing in November and December. Last week, WTI crude rose 2.9%, driven by geopolitical tensions and technical factors.

The balance of risks for UAE equities currently leans positive. Growing odds of a December Fed rate cut provide an additional tailwind. Continued strength in the non-oil economy and solid corporate earnings are rebuilding the foundation for interest in local dividend names. Nevertheless, over the next two weeks we expect largely neutral dynamics in the DFM and ADX indices. Technically, the correction remains in force: the DFMGI has slipped below its 50-day moving average, yet the bounce from the 5,800 support level raises the possibility of an upside reversal following the recent extended decline.