Investment Review №336. Choosing a direction

UAE market. A territory of stability

Geopolitical turbulence did not lead to a significant correction in the UAE stock markets.

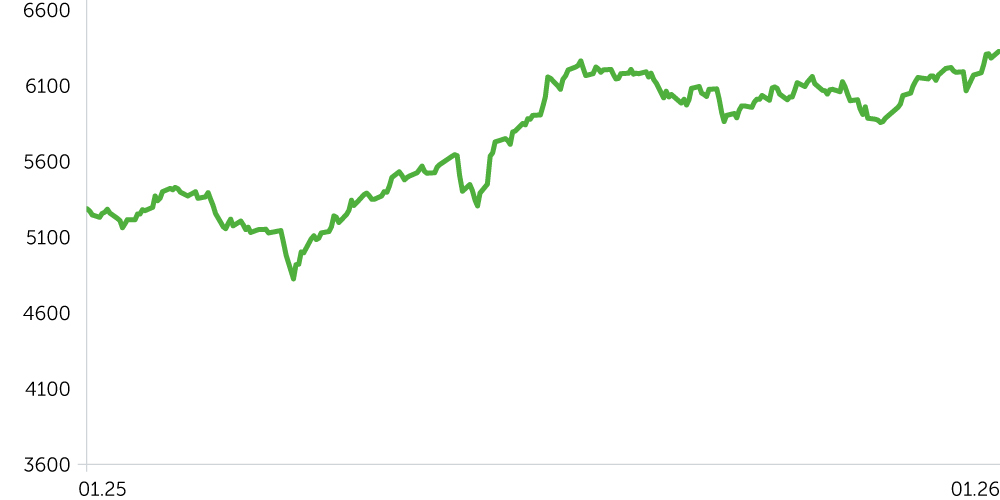

DFM General Index: 1-Year Dynamics

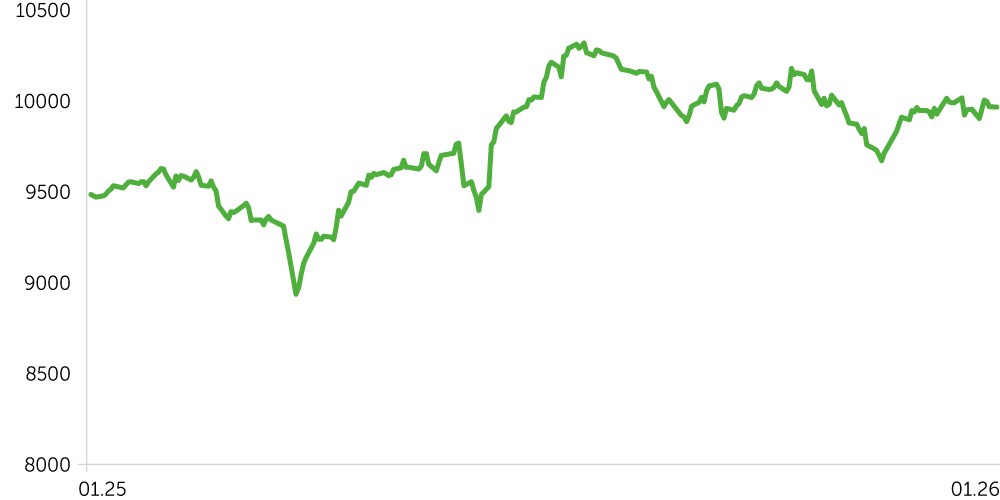

Abu Dhabi Securities Exchange index, 1-Year

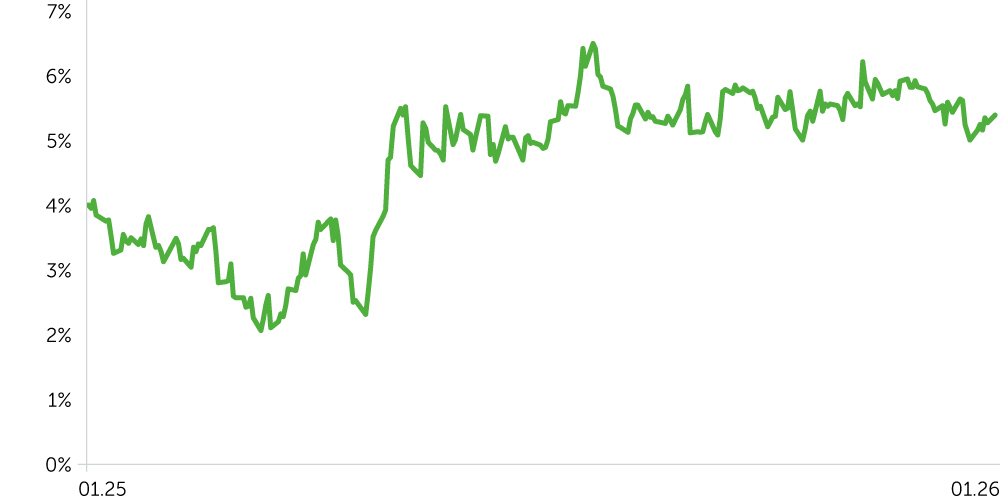

Yield, Forward Rate 1m10y, UAE, 1-Year Dynamics

Brent Oil, 1-Year Dynamics

- Between December 30, 2025, and January 12, 2026, UAE stock markets delivered mixed performances. The year began amidst heightened geopolitical tensions between the U.S. and Iran. The Dubai Financial Market (DFM) Index rose by 2.1% to reach 6,268 points, while the FTSE ADX General Index slipped 0.5% to 10,008 points. Over this period, Brent crude oil prices strengthened by 1.6%, climbing from $63 to $64 per barrel. For context, the S&P 500 Index gained 1% for the same period, reflecting moderate optimism in global markets.

- The Utilities sector was the primary underperformer, declining by 8.35%. Shares of Abu Dhabi National Energy Company (TAQA) plunged 12.18%, in response to the U.S. military operation in Venezuela. The Energy sector also faced pressure, losing 3.82%, with ADNOC Drilling shares decreasing by 5.13%. Despite negative geopolitics, the Real Estate sector showed resilience, recording an average gain of 1.77%. Emaar Development stock advanced 6.15% amid announcements of new large-scale projects and the relaunch of the Dubai Creek project. The Industrial sector also closed the period higher (+0.99%), driven primarily by Air Arabia’s impressive 11.94% rally.

- Yields on UAE Treasury bonds declined by 24 basis points, from 5.51% to 5.27%. Meanwhile, yields on 10Y U.S. Treasuries edged up by 2 basis points to 4.33%. As a result, the yield spread narrowed to 94 basis points, moving closer to historical averages. Interestingly, despite ongoing geopolitical tensions and negative price movements in oil stocks, investors continue to review the region’s credit risk favorably. This suggests a sustained shift in sentiment around the structure of the UAE economy.

Economic Updates

- Regime Change in Venezuela. The capture of President Maduro and the commencement of a power transition in Venezuela have set conditions for the country’s return to the global oil market. For the UAE, this introduces a long-term competitor; however, in the short term, the market is reflecting speculative price growth amid ongoing uncertainty. Analysts estimate that, given the current market surplus, investments in Venezuela’s oil sector are unjustified for now. Nevertheless, the very fact of a change in leadership fundamentally shifts the balance of power within OPEC+.

- Crisis in Iran. Protests against ruling ayatollahs, that began on December 28, 2025, escalated significantly by mid-January 2026, heightening risks in the region. For the UAE economy, this has a dual effect. On the one hand, potential sabotage of energy infrastructure and strikes in Iran could lead to a short-term supply shortage. On the other hand, if the protests succeed and sanctions are lifted, roughly 50 million barrels of oil currently held on tankers could flood the market almost immediately, with Iranian production likely to increase further within six months.

- Non-Oil Sector Remains Core to Stability. The UAE’s PMI stood at 54.2 in December. Although this represents a slight decline compared to November, the index remains steadily in expansion territory (above 50), supported by booming tourism and a robust inflow of investment. However, some companies have reported a decrease in demand from retail buyers.

Corporate News

- Emaar Properties (EMAAR: +2.1%): Founder Mohammed Alabbar confirmed plans to relaunch the Dubai Creek Tower megaproject with a redesigned concept. A tender for the project is expected to be announced within the next three months. Additionally, the company unveiled a new residential development, The Heights, with total investment comparable with Emaar’s largest masterplans.

- Emirates NBD (EMIRATESNBD: +3.66%) has completed a $1 billion issuance of environmentally friendly (“blue” and “green”) bonds.

Two-Week Outlook

In the global energy market, there is increasing uncertainty due to protests in Iran that began in late December 2025. In the short term, the risk of strikes by oil workers and sabotage at infrastructure poses a threat of supply shortages, which could drive oil prices higher. However, in case of a regime change in Tehran, long-term pressure on prices could materialize as sanctions are likely to be lifted and approximately 50 million barrels of Iranian oil, currently stored in tankers, may be released onto the market. Statistics from the U.S. Department of Energy also suggests a surplus: liquid hydrocarbons inventories surged by 8.4 million barrels, which is a negative signal for oil prices.

At the same time, the UAE’s major companies are set to release their Q4 2025 earnings at the end of January. Given the strength of the economy, we expect generally solid results across the corporate sector. This could serve as a positive fundamental driver, further contributing to a mixed outlook across segments of the UAE economy.

For the UAE equity market, the balance of risks appears broadly neutral. We believe robust performance in the banking and developer sectors will provide support for the DFM and ADX indices. However, volatility in oil prices—amid geopolitical tensions in Iran and Venezuela—could trigger a correction in energy stocks. Over the next two weeks, we expect neutral dynamics for both the DFM and ADX. Technically, there are signs of a trend reversal: DFM managed to break above its 50-day and 200-day moving averages, fully recouping the declines seen in January amid heightened geopolitical risk.