Investment Review №338. Change in Direction

The Armenian Market: Rapid Expansion Meets Overheating Concerns

Развитие текущих макротрендов будет способствовать усилению интереса инвесторов к локальным биржевым активам

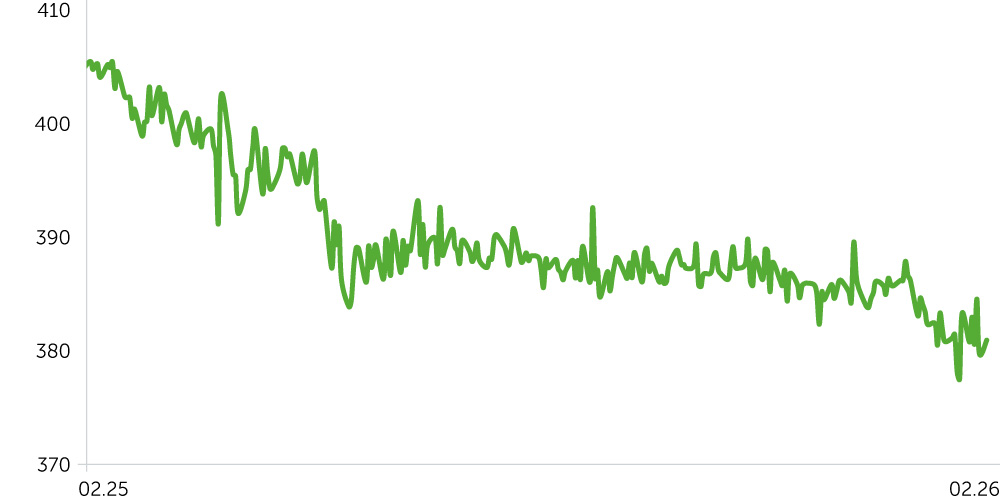

Telecom Armenia: 1-Year Stock Trends

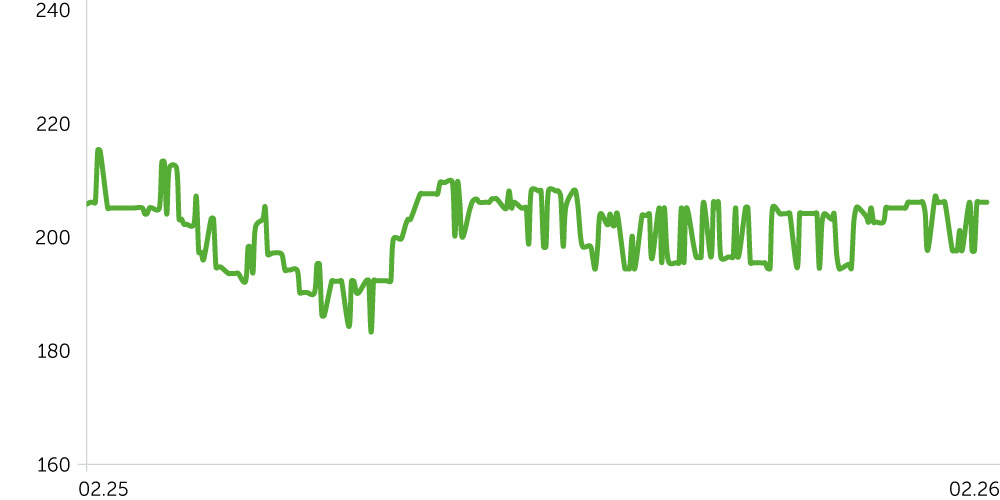

ACBA Bank: 1-Year Stock Trends

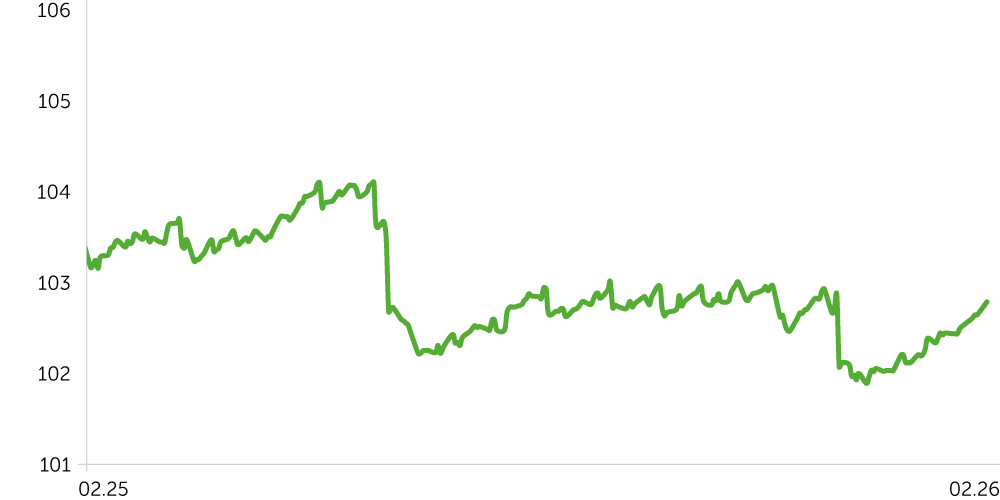

USD/AMD: 1-Year Dynamics

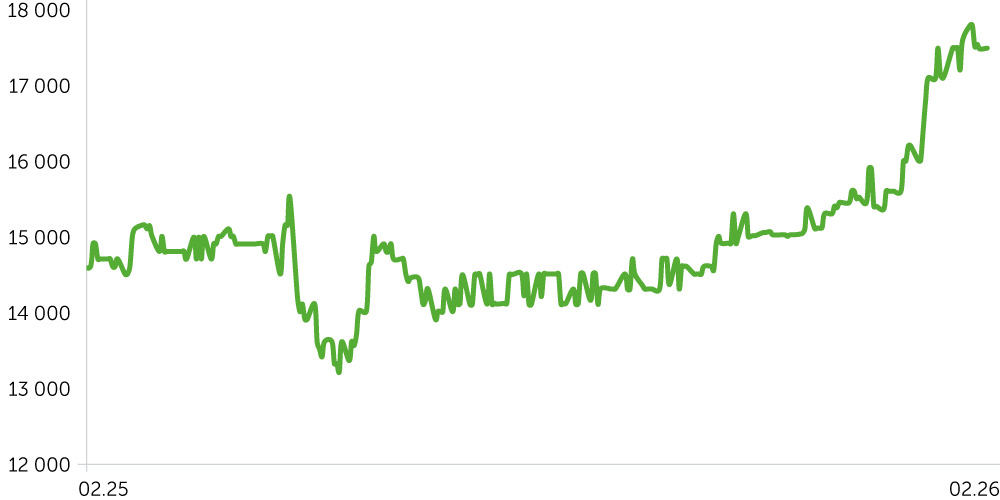

3-Year Corporate Bond Index (AMD) – Post-Update

Market Overview

From January 26 to February 9, 2026, the Armenian equity market posted modest gains. Investor sentiment was anchored by a twofold acceleration in December economic activity, which materially exceeded expectations and sets a favorable backdrop for early-2026 GDP growth. Telecom Armenia (AMTL) shares rebounded 4.3% but remained confined within the trading range established since September 2025. Acba Bank traded flat, showing no meaningful price movement.

The three-year dram-denominated corporate bond price index rose a further 0.3%, with yields compressing, which we interpret as evidence of renewed capital inflows amid a resilient macro backdrop, an improved sovereign rating profile, and the Central Bank’s refinancing rate held steady at 6.5%. Inflation edged up to 3.9% YoY, above forecasts, yet investors appear unfazed, likely because price dynamics remain within the regulator’s target range. Over the medium term, sentiment could come under pressure if incoming data continue to reinforce the overheating narrative. The Central Bank Governor flagged double-digit retail lending growth materially outpacing wage dynamics as a key signal, raising the risk of tighter funding conditions and, by extension, a moderation in economic growth. Meanwhile, the AMD/USD remained stable near multi-year lows, supported by accelerating export growth—both YoY and relative to imports—which contributed to a modest narrowing of the trade deficit in December.

Economic Updates

From January 26 to February 9, 2026, Armenia’s macro data surprised to the upside. External trade figures pointed to an acceleration in both export and import growth YoY versus the prior month, resulting in a narrowing of the trade deficit from –$485m to –$451m. The Central Bank left the refinancing rate unchanged at 6.50%, although the Governor flagged emerging signs of economic overheating. This makes the inflation uptick largely tax-driven rather than demand-led, supporting a measured, data-dependent stance by the regulator on future rate decisions.

- Armenia’s inflation in January 2026 came in at 3.8% YoY, slightly above the 3.1% forecast and at the top of the Central Bank’s 3% ±1pp target range, but still within bounds. The key driver was food and beverages (+5.9% YoY), with a notable contribution from alcohol and tobacco (+~9% YoY) on higher EAEU-mandated excise taxes. This makes the inflation uptick largely tax-driven rather than demand-led, supporting a measured, data-dependent stance by the regulator on future rate decisions.

- December external trade data were encouraging, signaling a recovery: total turnover rose 32% YoY and 9.4% MoM. Exports outpaced imports, climbing 34.3% YoY and 13.9% MoM versus 30.4% YoY and 6.5% MoM, suggesting stronger external demand and likely more structural gains in select export niches. We view this as evidence that the external trade cycle may have bottomed, and if the trend persists through 2026, it could mitigate net export headwinds on GDP. That said, the sustainability of the recovery will hinge on global price dynamics, further easing of geopolitical logistics constraints, and other key factors.

- Economic activity surged 14% YoY in December, well above the 11.5% consensus, and accelerated to 23.4% MoM. Industrial output drove the rebound, rising 38.6% YoY and 25% MoM versus a 4.7% average for 2025. Construction also made a strong contribution, up 20.5% YoY and a remarkable 77.9% MoM, while domestic trade and services expanded more modestly at 3.2% and 6.9% YoY, respectively.

- On February 3, the Central Bank of Armenia held the refinancing rate at 6.50%, but its tone turned more cautious. Governor Martin Galstyan highlighted signs of economic overheating, noting that consumer lending is growing ~20% YoY while wages rose only ~6% (November data). The regulator is closely monitoring the economy and stands ready to deploy macroprudential tools—such as buffers—to selectively cool riskier credit segments. Should double-digit retail lending persist, a tightening of policy rhetoric and funding conditions could weigh on domestic demand and economic growth.

Corporate News

- Team Holding is issuing a second tranche of USD-denominated bonds with an 8.75% annual coupon. Each bond carries a $100 face value and a 4-year tenor (48 months). The offering runs through April 12, 2026, with Freedom Holding Armenia acting as the underwriter. Team Holding is a diversified conglomerate with operations spanning renewable energy, logistics, real estate, IT, fintech, hospitality, e-commerce, FMCG, and winemaking.

Two-Week Outlook

Between February 13 and 23, only a limited amount of material macroeconomic data is expected for Armenia. However, revised releases of previously published statistics may be published during this period.

The key upcoming event is the release of Armenia’s 4Q25 GDP data, which will clarify last year’s final trends, while sector-level detail will allow a sharper read on economic strengths and weaknesses. Sustained moderately positive macro conditions, coupled with progress in the Armenia–Azerbaijan peace process—including the PM’s recent removal of transit restrictions on Armenian exports through Azerbaijan—could provide an additional catalyst for foreign investor interest in the medium to long term.