Investment Review №339. Playing Defense

Armenian Market: A Bright Streak

Strong fourth-quarter macro data supported solid gains in local equities

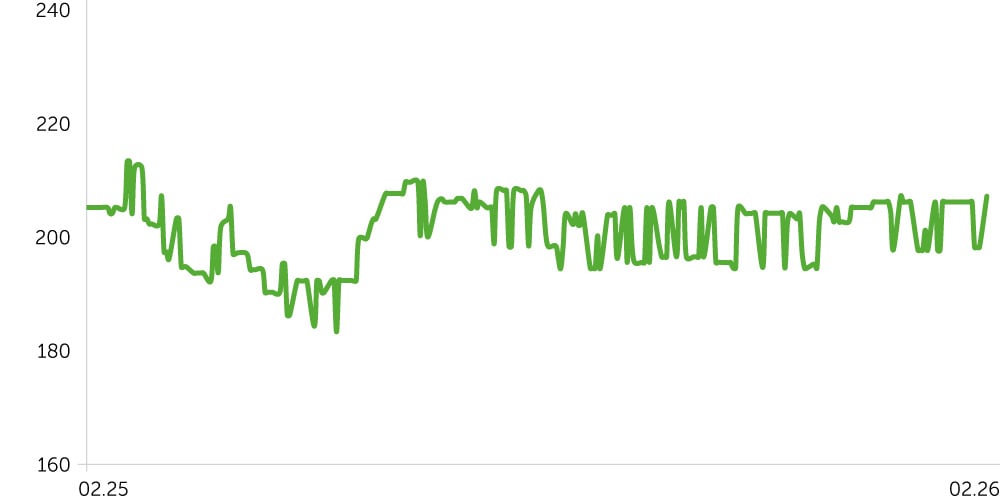

Telecom Armenia: 1-Year Stock Trends

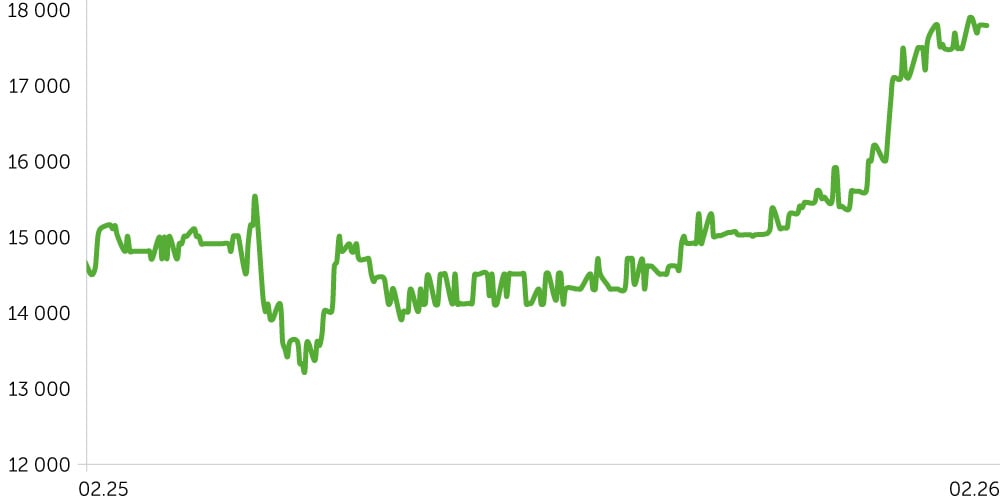

ACBA Bank: 1-Year Stock Trends

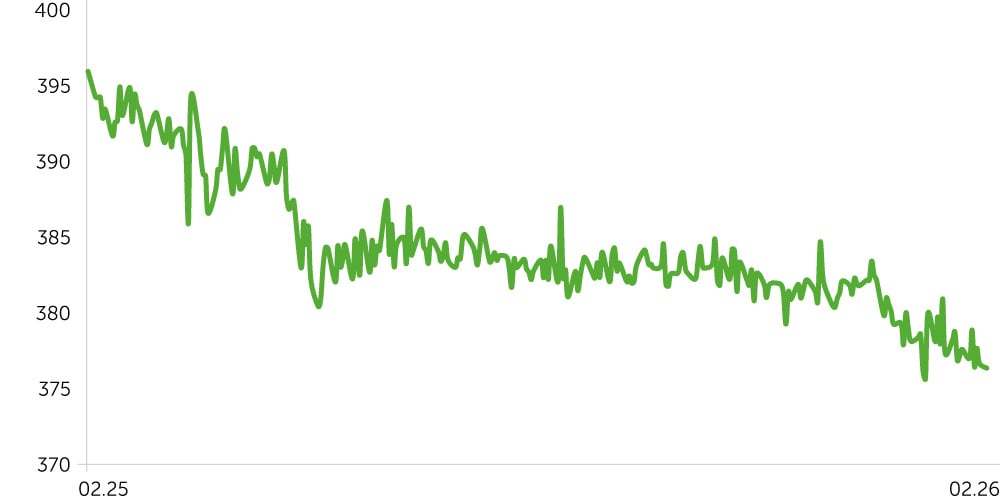

USD/AMD: 1-Year Dynamics

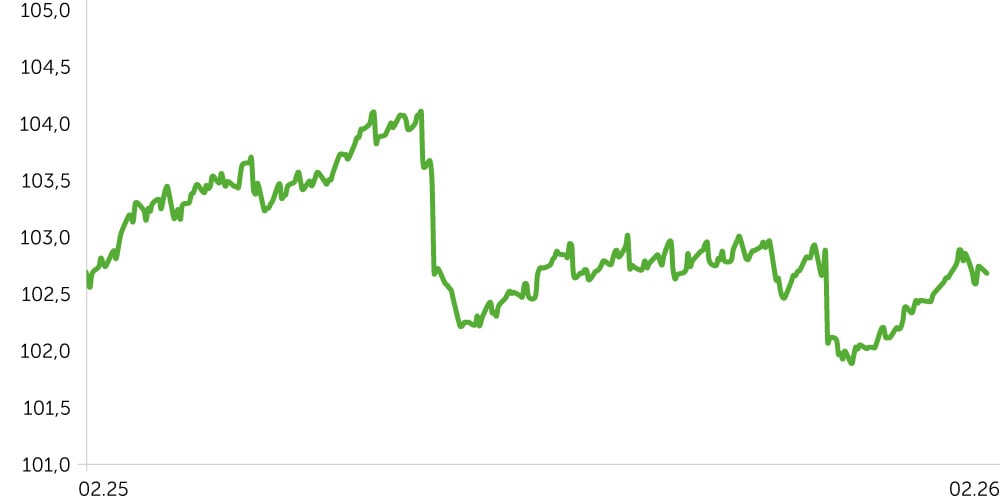

3-Year Corporate Bond Index (AMD) – Post-Update

Market Overview

Armenia’s stock market posted moderate gains over February 9-23, 2026. Acba Bank (ACBA) led the advance, rising 1.7% and lifting its YTD return to an impressive 14%. The period’s driver was likely buoyant sentiment in the financial sector, supported by the CBA governor’s comments on a reduction in the sector’s nonperforming loans (from roughly 5% to 2%) and record Q4 GDP growth of 9.8% YoY, with financial services up 14.3% for the quarter. Telecom Armenia (AMTL) delivered a more subdued +0.5%, consolidating after its prior rally, but remaining a beneficiary of sector momentum (+20% YoY in Q4).

The 3-year Corporate Bond Index was broadly unchanged, suggesting policy-rate expectations are largely priced in, consistent with the EDB’s forecast (2026 inflation at 3.3% and a 6.25-6.50% rate). Another moderately positive development for the period was S&P Global Ratings’ revision of Armenia’s credit rating outlook to Positive from Stable (BB-/B), mirroring Fitch’s recent move. The agency noted the economy’s resilience (average growth of 7.8% in 2022-2025) and progress in normalizing geopolitical relations. Together with record December tourist arrivals (+7.5% YoY), this decision supported a modest 0.5% appreciation of the dram versus the U.S. dollar. Even so, the late‑2025 GDP acceleration—driven in part by industry (mining +30.3% YoY) and construction (+18.7%)—alongside a pickup in retail credit growth warrants close monitoring by the regulator. In our view, the CBA will likely maintain a wait‑and‑see stance in the coming months, while assessing whether the acceleration is structural or cyclical and preventing potential secondary inflationary effects.

Economic Updates

Between February 9 and 23, Armenia’s macro data releases were marked by an S&P Global Ratings upgrade to the sovereign credit rating outlook and by robust Q4 GDP growth—outpacing the earlier quarters of 2025—underpinned by a strong rebound in industrial production.

- In Q4 2025, Armenia’s GDP growth accelerated sharply to 9.8% YoY, outpacing dynamics in the earlier quarters (5.2% in Q1, 6.4% in Q2, and 6.2% in Q3). The late-year macro data surge was driven by a robust rebound in industry: mining rose 30.3% YoY and manufacturing increased 18.5% YoY. For full 2025, construction (+21% YoY), information and telecom (+18.6% YoY), and financial services (+14.7% YoY) remained the structural growth leaders. This strong year-end performance underscores the economy’s high adaptability. That said, persistently rapid growth in construction and services, alongside accelerating credit activity—particularly in retail lending—warrants close monitoring.

- The Eurasian Development Bank (EDB) forecasts Armenia’s inflation at 3.3% in 2026—near the upper end of the CB’s target range (3% ±1 percentage points), if the refinancing rate remains within the 6.25-6.50% corridor.

- On February 20, S&P Global Ratings, following Fitch, revised Armenia’s credit rating outlook up to Positive from Stable and affirmed the long- and short-term ratings at BB-/B. The revision reflects a reassessment of the geopolitical backdrop, particularly expectations of further progress toward normalizing relations with Azerbaijan. In our view, the outlook upgrade across agencies is a key moderately positive signal for the local debt and Eurobond markets, raising the likelihood of a full souvereign rating upgrade in the medium term, contingent on the conclusion of peace agreements.

Corporate News

- Startup Firebird has confirmed plans to begin building AI infrastructure in Armenia after closing a land acquisition and entering the permitting phase. According to Armenia’s Minister of High-Tech Industry, Mkhitar Hayrapetyan, the first shipments of servers and graphics processing units (GPUs) are expected within two months, with services slated to launch in H2 2026.

Two-Week Outlook

Several key statistical releases are scheduled for February 27-March 9. The market’s primary focus will be the February CPI report, which should help gauge the persistence of price/inflation pressures. With January price growth already running near the upper end of the CB’s target range, any upside surprise could prompt a hawkish repricing of the interest rate path and weigh on risk appetite.

Also in focus is the January economic activity index, which is expected to moderate to 9% YoY after last month’s surge. Besides, data on construction (forecast +20.5% YoY vs. +16.0% in December) and industrial production (forecast +28.0% YoY vs. +38.6% in December) should provide additional insight into trends across key sectors.

Finally, trade-balance figures will speak to the durability of the recovery in import and export flows on a year-over-year basis. We expect the data to reaffirm the ongoing normalization in trade and, in all likelihood, to deliver few macro surprises, implying a neutral impact on market sentiment.