Investment Review №339. Playing Defense

UAE Market. The Rally Lacks Catalysts

Uncertainty in oil price trends has led to sideways trading on the UAE exchanges.

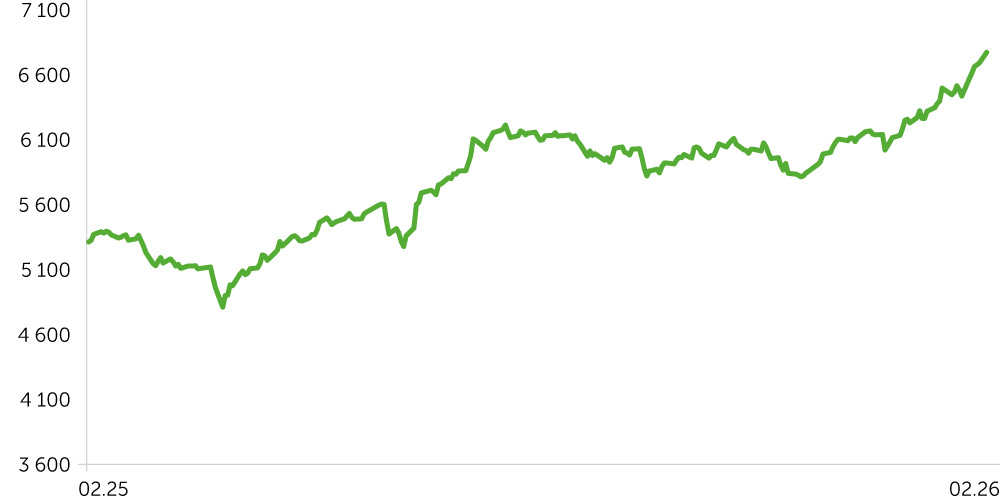

DFM General Index: 1-Year Dynamics

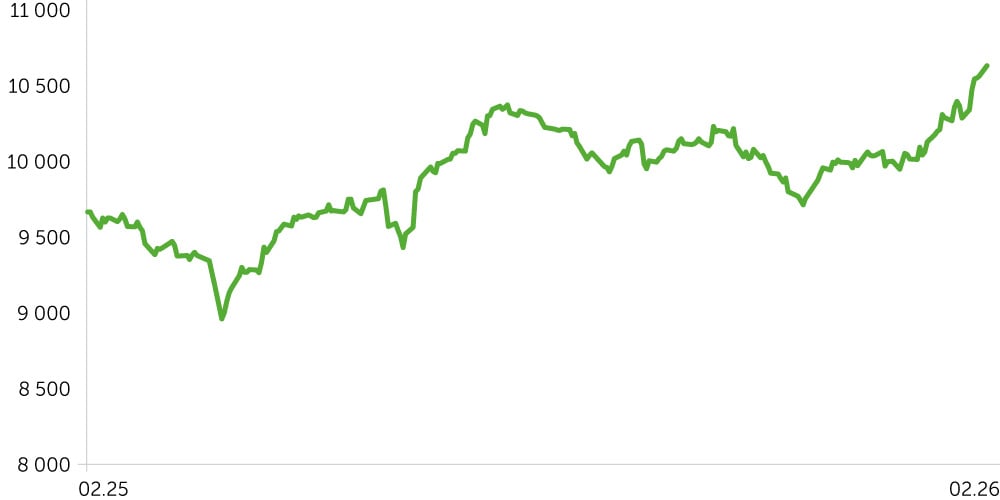

Abu Dhabi Securities Exchange Index: 1-Year Dynamics

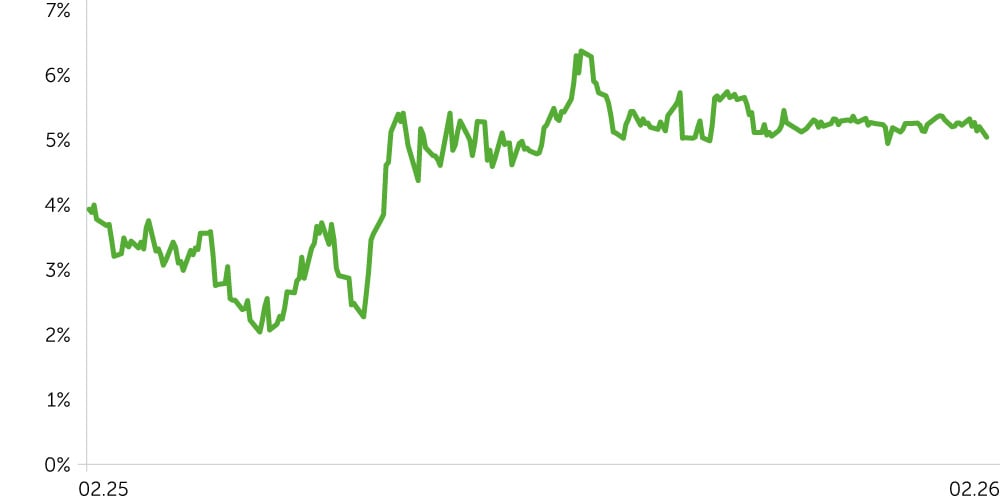

Yield, Forward Rate 1m10y, UAE, 1-Year Dynamics

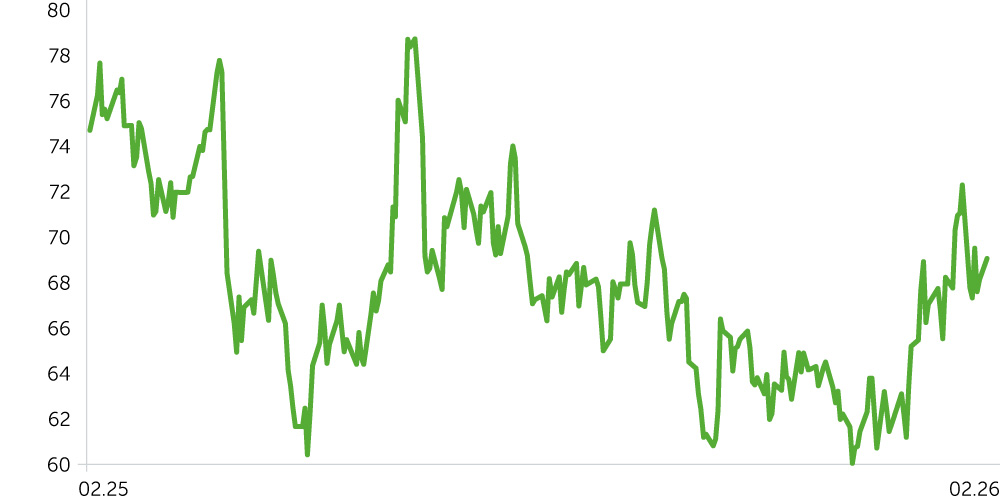

Brent Oil, 1-Year Dynamics

- Between February 9 and 23, 2026, UAE equities showed mixed signals. The Dubai Financial Market (DFM) slipped 0.9% to 6,711, while Abu Dhabi’s ADX eked out a marginal 0.1% gain to 10,639, both outperforming the U.S. S&P 500, which fell 1.8% over the same stretch (6,965 → 6,838). Geopolitical tensions around Iran continued to underpin oil prices: Brent rose 0.4% to $72/bbl, bolstered by lingering regional risks and expectations for the March OPEC+ meeting, supporting Abu Dhabi’s energy sector sentiment.

- Sector performance was mixed, with consumer names leading the charge as the standout outperformer. The consumer sector averaged +3.98%, driven by Americana Restaurants International, which surged 11.76% on expectations of sustained out-of-home dining demand and strong margins following a stellar 2025. Real estate held firm, averaging +3.03%, fueled by Emaar Properties (+3.96%), Aldar Properties (+3.31%), and Emaar Development (+3.19%), reflecting a $1bn Aldar-Apollo deal, record Abu Dhabi transaction volumes, and robust primary housing demand in Dubai and the capital region. Lagging sectors included energy, utilities, and industrials. Energy slumped 6.11% on profit-taking after a strong 2025 rally (Adnoc Gas −7.26%, ADNOC Drilling −5.62%). Rising chatter around potential OPEC+ quota hikes starting in April weighed on energy stocks, capping near-term upside in oil prices. Utilities declined 6.02% (TAQA −7.9%), as investors rotated from defensive, dividend-heavy names toward more cyclical plays, amid rising local yields. The industrial sector was uneven, averaging −5.48%, though select names outperformed sharply. Abu Dhabi Aviation jumped 10.53% and Air Arabia added 4.12%, benefiting from continued passenger recovery and record Dubai tourism in 2025. By contrast, Multiply Group (−12.34%) and Gulf Navigation (−6.8%) dragged the sector lower amid heightened volatility and targeted profit-taking in higher-risk names.

- UAE proxy Treasury yields rose 17bps to 5.20% from 5.02% in early February. U.S. Treasuries climbed 14bps over the same period, from 4.14% to 4.27%. The UAE–U.S. yield spread widened to 106bps from 75bps, reflecting local risk premiums and UST flight-to-quality tendencies amid a reassessment of the Fed’s rate-cut trajectory.

Economic Updates

- OPEC+ Meeting: Market focus remains on the March 1 OPEC+ meeting, where decisions on April production quotas will be made. Since September 2025, OPEC+ output has fallen 649k b/d, following quota increases of 137k b/d per month in October–December 2025, while growth in the first three months of 2026 was paused. Against this backdrop, the current negative production trend raises the likelihood of renewed quota hikes from April, which could modestly cap further oil price upside amid sustained demand.

- UAE Economy Shows Resilient Growth: According to the Ministry of Economy, UAE GDP rose 5.1% YoY in the first nine months of 2025 to AED 1.4tn, with non-oil sectors up 6.1%, surpassing AED 1tn and driving overall expansion. Officials linked results to the We the UAE 2031 strategy: accelerated non-oil growth and an improved business environment are supporting the long-term goal of doubling GDP to AED 3tn, with current figures serving as an interim validation of diversification efforts.

- Leading Indicators Confirm Momentum: The non-oil private sector PMI climbed to 54.9 in January 2026 from 54.2 in December, reflecting faster order and output growth. Companies reported the fastest increase in new orders in nearly two years, alongside improved expectations for future activity.

Corporate News

- e& (Emirates Telecommunications Group): The company delivered record 2025 results, emerging as a standout among ADI blue chips. Consolidated revenue rose 23% YoY to ~$72.9bn, driven by international asset consolidation and growth in digital verticals, while net profit jumped 34% YoY to $3.9bn. The board proposed 20% higher dividends for 2025 (AED 0.96/share vs 0.80), signaling strong cash flow confidence. Emirates Integrated Telecommunications (du) shares also gained 1.4%, reflecting expectations that the competitor will benefit from resilient demand in mobile and fixed-line services, alongside ongoing 5G and digital investments.

- Aldar Properties (ADX): On February 19, 2026, Aldar secured $1bn in subordinated capital from Apollo-managed funds, strengthening its balance sheet and enhancing long-term project financing capacity. A key fundamental remains its robust development backlog, representing pre-sold projects yet to be recognized as revenue—a multi-year earnings pipeline. Following the Apollo deal, Aldar shares rose 3.31% over two weeks, outpacing the real estate sector average (3.03%). Supporting the story, Abu Dhabi property market data showed record 2025 transaction volumes of $38.67bn, highlighting sustained domestic and foreign demand and creating a favorable backdrop for tier-one developers.

Two-Week Outlook

Iran-related developments and the March 1 OPEC+ meeting remain the primary near-term drivers for oil prices and, by extension, UAE equity sentiment. The onset of a military action or hawkish rhetoric could lift crude prices and support the energy sector, but a potential OPEC+ decision to resume quota hikes from April may quickly offset some of these gains, raising volatility risks in Q2.

Technically, both the DFM and ADX are in an active uptrend, trading above their 50- and 200-day moving averages. However, RSI readings above 75 signal overbought conditions, increasing the likelihood of a near-term pullback.