Investment Review №340. The Bombshell Effect

Black Swans vs. the Bulls

The outbreak of armed conflict in the Middle East triggered a record plunge in Emirati stock prices

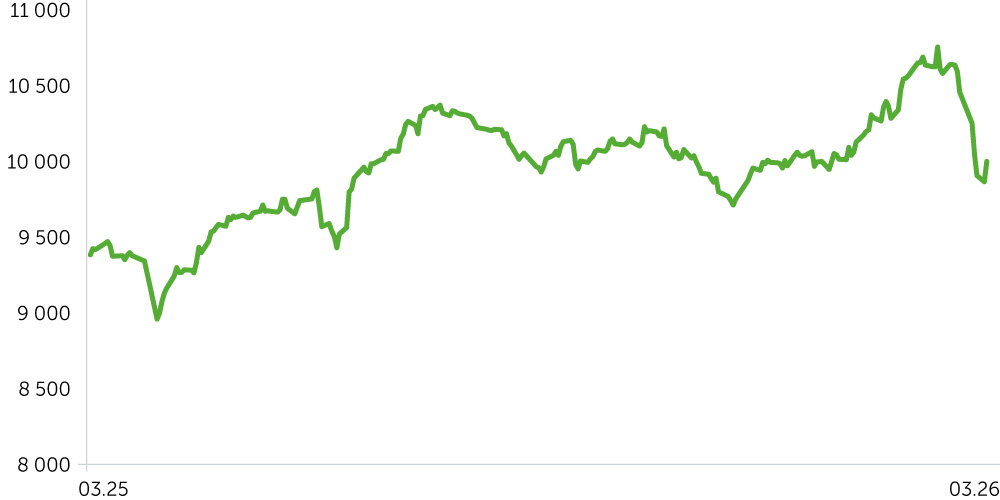

DFM General Index: 1-Year Dynamics

Abu Dhabi Securities Exchange Index: 1-Year Dynamics

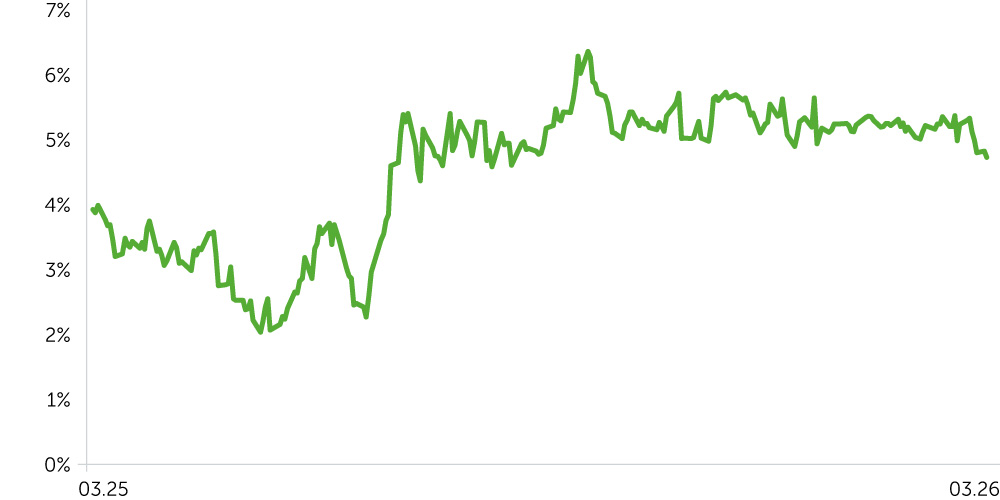

Yield, Forward Rate 1m10y, UAE, 1-Year Dynamics

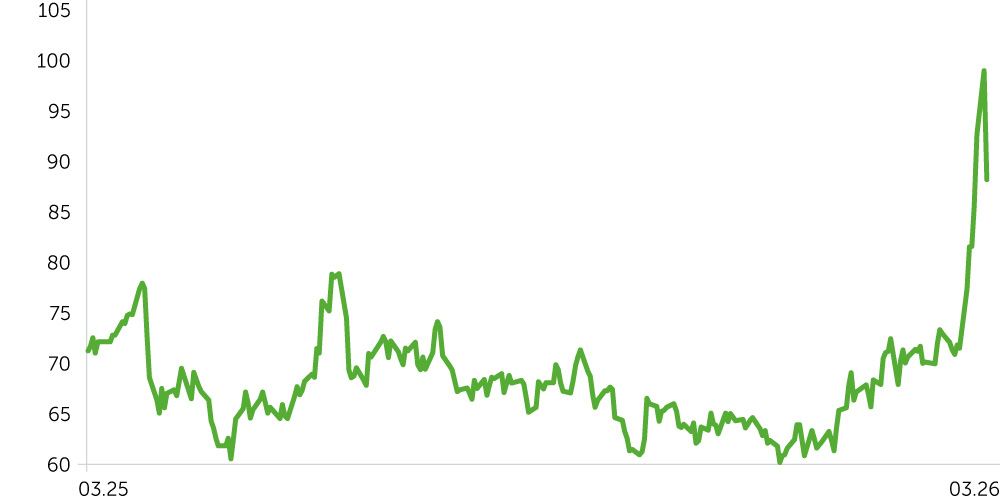

Brent Oil, 1-Year Dynamics

- Between 24 February and 10 March 2026, UAE equities experienced an unexampled selloff following the 28 February start of U.S.-Israeli military operations against Iran and subsequent Iranian missile and drone strikes targeting U.S. military facilities in the UAE. The Dubai Financial Market (DFM) Index fell 12.0% to 5,867 (from 6,669), the Abu Dhabi Securities Exchange (ADI) Index declined 6.0% to 9,997 (from 10,638). By comparison, the S&P 500 slipped 1.6% to 6,781 (from 6,890) over the same period, highlighting the disproportionate pressure on local assets. The Securities and Commodities Authority (SCA) suspended trading on DFM and ADX on 2-3 March; when markets reopened on 4 March, a temporary 5% downside limit was introduced to curb disorderly selling. Brent crude rose 23.8% to $88/bbl (from $71) amid the escalation in the Persian Gulf and heightened risk of disruption in the Strait of Hormuz.

- Sector performance was negative, with cyclical segments under the greatest pressure. Real Estate was the clear laggard: the average return was -20.57%. Emaar Properties fell 25.44%, Aldar Properties declined 24.60%, and Emaar Development lost 21.08%. Both flagship developers repeatedly closed at the -5% circuit breaker during the first sessions after trading resumed. On March 6, Aldar Properties nonetheless confirmed “full operational continuity” in the UAE, which helped reinforce confidence in the perceived resilience of the large developers’ business models. Consumer Discretionary declined 14.15% on average. The steepest drop came from Parkin Company (-21.44%)—Dubai’s public parking operator, whose revenue is closely tied to passenger volumes, tourism activity, and footfall at malls and airports. The closure of UAE airspace, the cancellation of more than 11,000 flights across the region, and a shift to remote work and learning sharply reduced road traffic, clouding the company’s near-term operating outlook despite strong 2025 results (revenue: +42.9% YoY; net income: +47.7% YoY). In Industrials, the average return fell 11.75%, driven primarily by Air Arabia (-22.46%), which was hit by airspace closures and flight disruptions. Energy was relatively more resilient: the average two-week return was -4.46%. Despite a sharp rise in oil prices, investors took profits in ADNOC Gas (-4.07%) and ADNOC Drilling (-3.82%).

- Since late February, the UAE Treasury-bond proxy yield fell 47 bps to 4.72% from 5.19%, reflecting flight-to-quality flows. Over the same period, U.S. Treasury yields rose 9 bps to 4.23% from 4.14%. As a result, the spread between the UAE proxy and U.S. Treasuries narrowed to 49 bps from 105 bps. This shift points to fund inflows into government securities amid broader market uncertainty.

Economic Updates

- On March 1, 2026, eight OPEC+ members, including the UAE, agreed to raise oil production, announcing a 206 kb/d increase starting in April 2026. This begins a gradual unwind of 1.65 mb/d in voluntary cuts introduced in April 2023. After pausing quota increases through the first quarter of 2026, the group is now resuming the process, citing a “sustainable global economic outlook and low oil inventories.” However, the outbreak of hostilities in Iran has materially shifted the balance of risks: tanker transits through the Strait of Hormuz have dropped to about four vessels per day, versus a typical 24. J.P. Morgan estimates that complete closure of Hormuz could remove up to 4.7 mb/d from the market. Brent briefly exceeded $100/bbl before retreating to around $88/bbl by March 10.

- Central bank and financial stability. On March 5, the Governor of the UAE Central Bank stated that the country’s banking and financial system remains highly resilient and stable. The capital adequacy ratio is 17%, the liquidity coverage ratio exceeds 146.6%, and total banking assets now surpass AED 5.42tn ($1.48tn). Banks, finance companies, and insurers continue to operate normally, with digital platforms and payment infrastructure functioning without interruption. Fitch affirmed that GCC banking systems are “well buffered” against conflict-related credit risks under its baseline assumption of a conflict lasting less than one month. However, the agency cautioned that prolonged damage to energy infrastructure or extended hostilities could pressure sovereign ratings and, by extension, bank ratings. S&P Global Ratings lowered the real GDP growth forecast for 2026-2027 to 2.5% from 4.2%, citing the potential impact of the conflict on tourism and investment flows.

- UAE macro data. The UAE non-oil sector PMI rose to 55.0 in February 2026 from 54.9 in January—a 12-month high—signaling broad expansion. Growth in new orders accelerated, supported by stronger demand in tourism, e-commerce, and AI. The labor market strengthened, with employment growth at its fastest pace since November 2025. Input cost inflation eased to its lowest since October 2025, helped by lower fuel prices. Dubai’s PMI eased to 54.6 from 55.9 in January but continued to signal strong growth. The data were released on March 4 and reflect conditions prior to the recent escalation in hostilities; any impact from the conflict is likely to appear in the March-April readings.

Corporate News

- Emaar Properties (DFM: EMAAR). On March 5, the company issued an operational update on UAE real estate sales of $4.68bn for January-February 2026, up 118% YoY. The update builds on record 2025 results released in mid-February. The shares were among the period’s notable laggards, falling 25.4% over two weeks and repeatedly hitting the -5% limit. This appears to reflect a repricing of geopolitical risk rather than any deterioration in fundamentals.

- IHC/Judan Financial (ADX: IHC). International Holding Company (IHC) established Judan Financial, an AI-driven financial services holding company that will manage over $237bn in assets, including Chimera Investment, Lunate Capital, International Securities, and other units. On March 9, Judan announced its first strategic transaction: the acquisition of 50.1% of Alpha Wave Global, a U.S. investment manager with $29bn in AUM and investments in SpaceX (largest position), Anthropic, OpenAI, Cerebras, and others. The initiative aims to build an AI-native U.S. life insurance platform and expand IHC’s global financial services footprint. IHC shares were broadly resilient over the period (-0.40%), consistent with the conglomerate’s defensive profile and positive sentiment around its expansion strategy.

Two-Week Outlook

The key driver over the coming weeks remains the trajectory of the regional military conflict. Trump’s March 10 assertions about a possible imminent end to hostilities sparked a partial rebound in stocks (DFM +2.0%; ADX +1.4%), but ongoing attacks are capping the recovery. Air transportation remains constrained, with most major airlines extending suspensions of flights to and from the UAE into mid-March. A full restoration of air services would be a key signal of regional stabilization.

The next OPEC+ meeting is scheduled for April 5, when production policy will be reassessed in light of market conditions. Fundamentally, risks to oil prices are skewed to the downside over the longer term. OPEC+’s planned output increases add pressure, while the recent hostilities produced only a short-lived bounce. Taken together, these factors are exerting downward pressure on prices and heightening the risk of a longer-term decline. In addition, OECD countries and China jointly hold an estimated ~3.6 bn barrels of strategic crude and product inventories and could draw as much as ~15 mb/d, allowing them to substitute for lost Gulf volumes for an extended period.

With uncertainty persisting, UAE equities are likely to remain volatile.

Defensive sectors (telecoms, utilities, consumer staples) should show relative resilience, while real estate developers and airlines will remain most sensitive to headlines. The banking sector’s strong capital buffers and the recent affirmation of S&P and Fitch ratings provide a foundation for sustained financial stability even under a protracted scenario.