Investment Review №343. The return of the bulls

A Time for Optimists

Stock indices in the Emirates rose sharply on expectations that the U.S. military operation in Iran would come to an end

DFM General Index: 1-Year Dynamics

Abu Dhabi Securities Exchange Index: 1-Year Dynamics

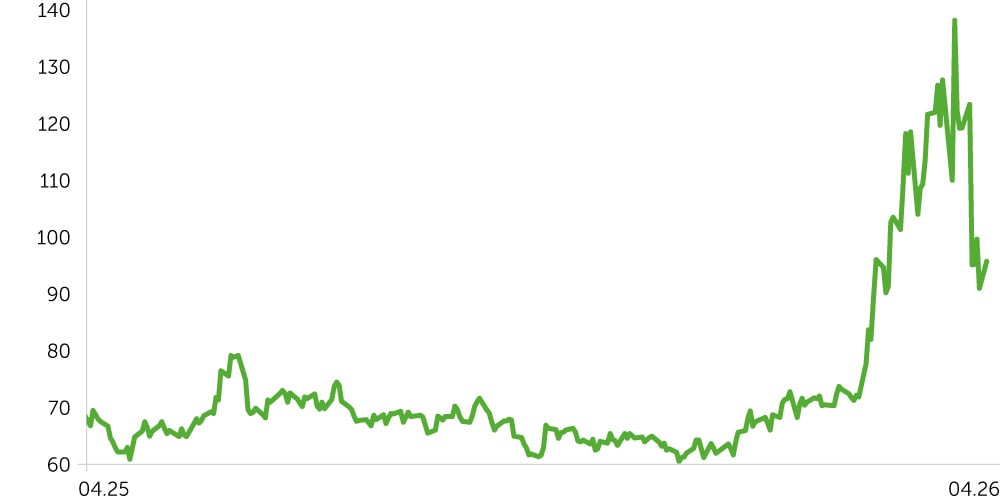

Yield, Forward Rate 1m10y, UAE, 1-Year Dynamics

Brent Oil, 1-Year Dynamics

UAE equities saw elevated volatility through April 6–20, ultimately resolving into a firm upside move across benchmarks. Price action was driven by a complex geopolitical mix, including temporary easing of tensions in the Gulf followed by renewed concerns over supply stability through the Strait of Hormuz. Against the backdrop of a global correction in energy prices and a repricing of U.S. Fed rate expectations, UAE equities outperformed many developed markets, signaling strong investor confidence in the country’s macroeconomic stability. Over the period, key UAE benchmarks delivered positive returns, rebounding from prior uncertainty. The Dubai Financial Market (DFM) advanced 7.6%, rising from 5,448 to 5,862, driven by liquidity inflows into Financials and Construction, alongside positive developments in logistics reconfiguration. The Abu Dhabi Securities Exchange (ADX) advanced 2.2%, reaching 9,842 vs 9,625 at the start of the period. DFM’s relative outperformance reflected its higher exposure to real estate and transport names, which benefited most from ongoing economic adjustment. Brent crude oil prices declined 13%, falling from $110 to $95/bbl, as markets priced in expectations of de-escalation and a reopening of the Strait of Hormuz for commercial shipping. The move resulted in a sharp compression of the geopolitical risk premium.

Over the 2-week horizon, sector dynamics were predominantly positive, with Industrials leading at an average 13.26%—driven by Gulf Navigation Holding (+44.8%), a direct beneficiary of the opening of the Strait of Hormuz to tanker traffic, and Air Arabia (+27.8%), which recovered after several weeks of route disruptions. Real Estate advanced 7.14% on average, led by RAK Properties (+15.0%), Emaar Development (+13.4%), and Emaar Properties (+10.9%), while Consumer Discretionary gained 6.88% on average, supported by Taaleem Holdings (+13.3%) and Parkin (+11.7%). At the other end, Communication Services were broadly flat at +0.33% on average, reflecting their defensive profile in a risk-on environment, while energy was likewise subdued at +0.08% on average, as the opening of the Strait of Hormuz neutralized the geopolitical risk premium in oil equities, capping upside.

UAE sovereign proxy yields declined 43bps, from 5.25% to 4.82%, reflecting compression in the regional risk premium following the ceasefire. The 10-year U.S. Treasury yield declined by 9bps over the period, from 4.42% to 4.33%. Consequently, the UAE spread over U.S. Treasuries narrowed from ~82bps to ~49bps. This compression indicates that markets are beginning to price a partial unwinding of the geopolitical risk premium embedded in UAE assets, though yields at ~4.82% remain elevated by historical norms given persistent uncertainty.

Economic Updates

- GDP proxy and business activity. The Central Bank of the UAE reaffirmed its real GDP growth forecast at 5.6% for 2026, unchanged vs 2025, with expansion driven primarily by non-oil sectors—Financial Services, Manufacturing, and Construction. Non-oil GDP is expected at 4.5–5.0%, while oil GDP should be supported by the recent increase in OPEC+ quotas. The S&P Global UAE PMI declined to 52.9 in March (vs 55.0 in February)—the lowest since July 2021, but still in expansion territory. The slowdown was driven by supply chain disruptions linked to restrictions in the Strait of Hormuz: delivery times lengthened for the first time since September 2021, input costs rose sharply, and business expectations fell to a five-year low. Nonetheless, the PMI is expected to stabilize in April as logistics normalize following the reopening of the strait.

- Banking sector—assets at record highs. According to the UAE Central Bank (data published April 9), total banking system assets reached $1.49tn by end-February 2026, up 1.1% MoM. Gross loans increased to $716.1bn (+1.2% MoM), including a $5.6bn rise in domestic credit. Deposits stood at $925.8bn, with private sector deposits up 2.2% to $632.2bn. Sector capital adequacy is 17%, while the liquidity coverage ratio exceeds 146.6%.

- Dubai AED1bn (~$272m) stimulus package. Effective April 1, 2026, the AED1bn ($272m) package approved by Crown Prince Sheikh Hamdan provides targeted support over a 3–6 month horizon, including a three-month deferral of tourism and hotel fees, an extension of the customs clearance grace period from 30 to 90 days, and simplified residency procedures. The measures are primarily aimed at the tourism and hospitality sectors, which have come under pressure from reduced inflows during the conflict period.

- Dubai Real Estate—record 1Q26. According to the Dubai Land Department (DLD), total transaction value reached $68.6bn in 1Q26, up 31% YoY in value and 6% YoY in volume. Real Estate investment totaled $47.1bn (+22% YoY), with 57,744 investments and 48,448 investors, including 29,312 new investors (+14% YoY). Separate estimates indicate the luxury segment reached $23.9bn and remains the key driver of value growth, while off-plan transactions account for ~70% of total volumes.

Corporate News

- Abu Dhabi Islamic Bank (ADX: ADIB). On April 14, the bank opened a new retail branch at Dubai Hills Mall, underscoring continued geographic expansion in the retail segment. Over the 2-week period, the stock rose 10.95%.

- Emaar Properties / Emaar Development (DFM: EMAAR / EMAARDEV). Emaar Properties benefited directly from record Dubai Real Estate activity in 1Q26, with total transactions up 31% to AED252bn ($68.6bn), providing a clear tailwind to developer sales. On April 17, the market continued to show sustained demand for Emaar projects in both villa and apartment segments, notably within The Oasis development.

- Multiply Group (ADX: MULTIPLY). On April 20, 2026, the company announced a $19.7bn all-share acquisition of 2PointZero and Ghitha Holding from International Holding Company (IHC), issuing 23.36bn new shares to IHC. The deal aims to form a diversified investment holding platform with an estimated valuation of ~$32.6bn across Energy, Food, Logistics, Packaging, Mining, and Media. Over the 2-week period, the stock rose 11.52%.

- Air Arabia (DFM: AIRARABIA). The stock posted one of the strongest gains in the Industrials sector, up 27.8% over the period. The airline emerged as a direct beneficiary of the ceasefire, supported by the resumption of regional air traffic, lower jet fuel costs following the decline in Brent, and the reopening of airspace. Aviation equities globally rallied sharply on April 8, reflecting relief over the reduced risk to the Strait of Hormuz corridor.

- Gulf Navigation Holding (DFM: GULFNAV). The stock was the top performer over the period, surging 44.8%. The integrated marine transport operator for oil and chemical cargoes was a direct beneficiary of the reopening of the Strait of Hormuz, with the restoration of tanker transit through the corridor effectively normalizing operating flows after several weeks of disruption. On April 22, the company scheduled a Board meeting to review strategic matters.

- SHUAA Capital (DFM: SHUAA). Shares rose 18.54% over the period, marking the second-strongest performance in Financials. On April 14, 2026, SHUAA Capital and Gate Capital announced the launch of the first retail fuel retail platform in Saudi Arabia, a strategic step expanding the company beyond the UAE. The Annual General Meeting is scheduled for April 25, 2026, to review FY25 financial results.

Two-Week Outlook

The key inflection point over the period was the announcement of a temporary U.S.–Iran ceasefire alongside the reopening of the Strait of Hormuz. UAE markets responded with a strong rally, while oil corrected 13%, with Brent declining from $110 to $95/bbl. However, the truce remains fragile and short-lived in nature.

OPEC+ output in March collapsed by 7.7m b/d MoM amid constraints through the Strait of Hormuz, with the steepest declines in Iraq (−2.6m b/d MoM, −61.2%), Saudi Arabia (−2.3m b/d MoM, −22.9%), the UAE (−1.5m b/d MoM, −44.7%), and Kuwait (−1.4m b/d MoM, −53.0%).

In the base case, the ceasefire gradually evolves into a more durable arrangement: the Strait of Hormuz remains open, oil stabilizes below $95/bbl, and UAE risk premia in rates continue to compress. Under this scenario, the UAE Banking sector remains a key beneficiary, supported by high liquidity levels and continued loan book expansion. Real Estate retains structural support, with record 1Q26 activity in Dubai and Abu Dhabi underscoring sustained investor demand. Industrials and Marine Transport sectors emerge as direct beneficiaries of logistics normalization.

In a downside scenario, a breakdown of the ceasefire or renewed closure of the Strait of Hormuz could trigger a renewed market correction. The most exposed segments are highly leveraged Developers, Banks with concentrated real estate loan books, as well as the Aviation and Logistics sectors.

Key investor watchpoints include: (1) developments in U.S.–Iran negotiations and the operational status of the Strait of Hormuz; (2) the UAE PMI print for April (expected in early May); and (3) initial April data for Dubai and Abu Dhabi real estate markets.

The main medium-term headwind for asset prices remains supply normalization: reopening of the Strait of Hormuz would restore export volumes from Iraq, Saudi Arabia, the UAE, and Kuwait that were disrupted in March. The current reopening is still temporary in nature, while the risk of renewed escalation could still drive sharp volatility in pricing.