Двухнедельный обзор фондовых рынков №326. Между двух огней

Corporate News In Focus of Our Analysts

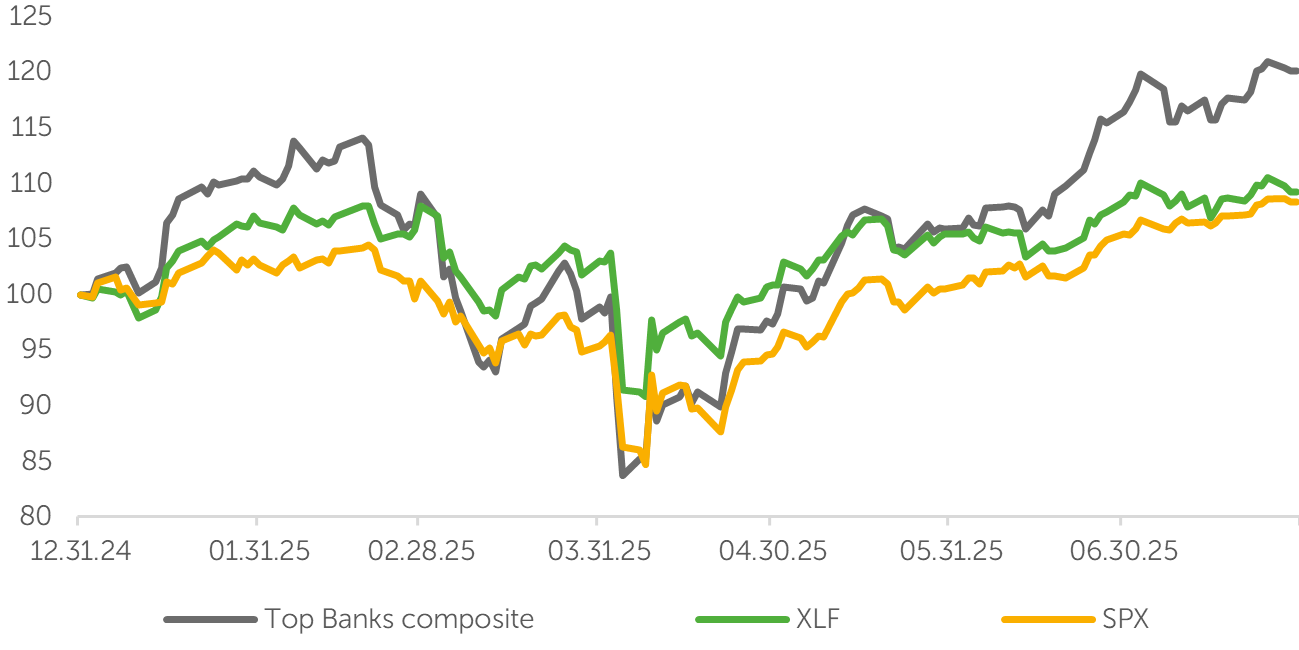

Wells Fargo, Goldman Sachs, Bank of America

In the second quarter of 2025, the largest U.S. banks surpassed expectations with their financial results, primarily driven by an upswing in lending, notably within the corporate sector. A comparable trend was observed in deposits, with interest-bearing accounts gaining prominence over their non-interest-bearing counterparts. Wells Fargo diverged from this pattern, remaining constrained by asset restrictions through June. While deposit rates decreased faster than loan rates, the net interest spread exhibited varied dynamics across different banks, contingent on fluctuations in other asset and liability rates. Notably, provisioning activity decelerated during this period.

Non-interest income witnessed an uptick, fueled by robust trading results, an increase in assets under management, and a resurgence in investment banking activities. Among the top five banks, excluding Wells Fargo, the median growth in trading and investment banking revenues stood at 13%. Goldman Sachs emerged as the leader with a 23% increase, while Bank of America trailed with a modest 4% rise.

These positive indicators have emerged despite prevailing trade tensions, macroeconomic uncertainties, and geopolitical strife over the quarter. The sector is benefitting from potential trade normalization, robust credit expansion, a favorable yield curve slope, and sustained vigor in capital markets—particularly with the prospect of interest rate reductions and easing regulatory constraints. Consequently, most bank stocks have registered significant appreciation since the start of the year, reflecting elevated valuations against historical benchmarks.

Composite Index Price Dynamics of Leading Banks Versus the Broad Market and Financial Sector Benchmarks

Source: FactSet, Freedom Broker analysis

Alphabet

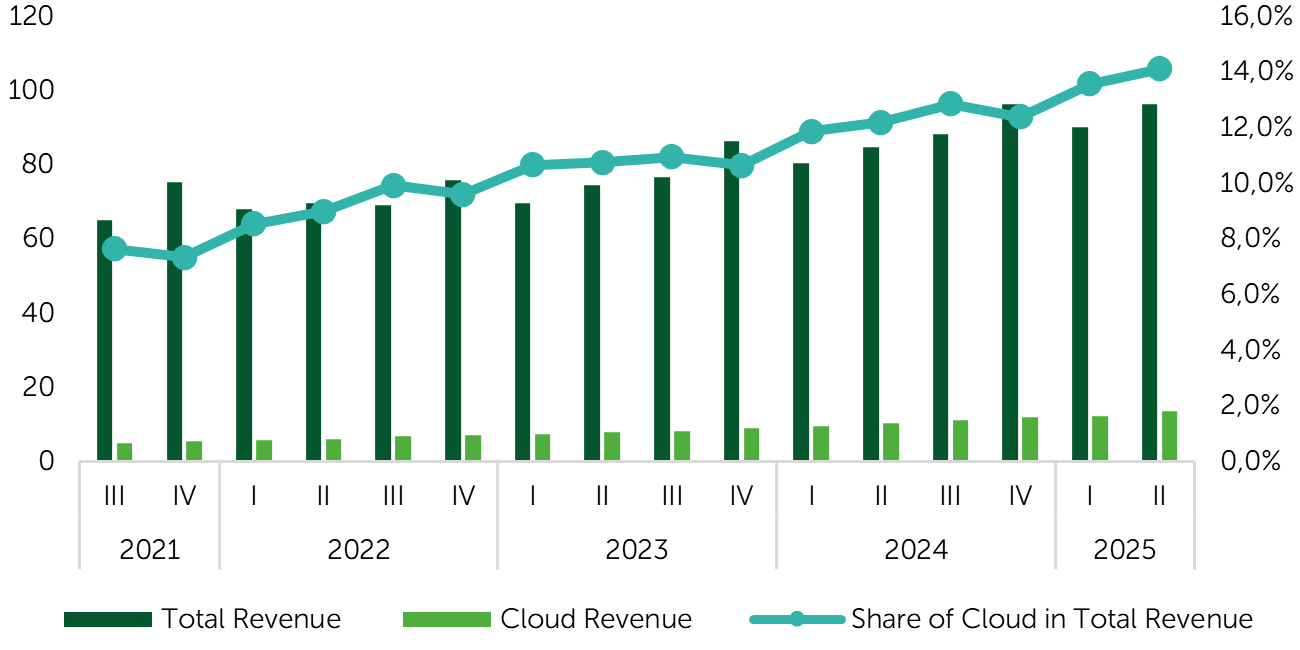

On July 23, Alphabet Inc. (GOOGL) unveiled its financial results for the second quarter of 2025, highlighting a substantial boost from its cloud segment. Alphabet's performance exceeded market expectations, fueled by robust growth across its search and YouTube platforms, as well as a marked acceleration in its cloud services. Consolidated revenue reached $96.4 billion, reflecting a 12% y/y increase. Notably, revenue from Google Cloud surged by 32% to $13.6 billion, driven by a broadening customer base in Vertex AI. Management emphasized the strategic use of proprietary TPUs, which affords a pricing advantage. Alphabet has projected sustained strong demand for AI workloads and anticipates continued expansion of its customer base within the cloud segment. In response to this growing demand, the company has revised its capital expenditure forecast for 2025, raising it from $75 billion to $85 billion. Major investments will be directed towards the acquisition of servers and the accelerated construction of data centers. Furthermore, the company is committed to aggressively expanding its AI and cloud teams, while strategically managing operating expenses.

Alphabet's Total Revenue and Cloud Revenue

Source: FactSet, Freedom Broker

Sarepta Therapeutics

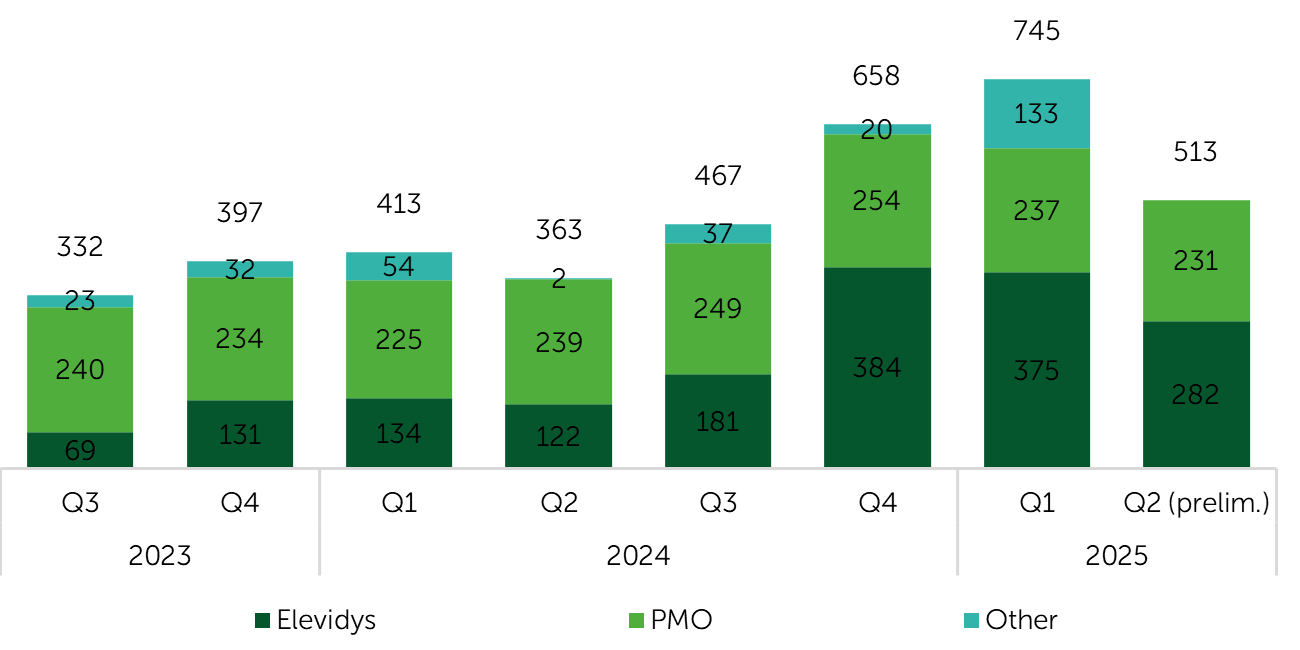

On July 22, Sarepta Therapeutics ceased all distributions of Elevidys within the United States, following the deaths of three patients who succumbed to acute liver failure. Notably, two of these individuals were adolescents diagnosed with Duchenne muscular dystrophy, having been treated with Elevidys, while the third was a 51-year-old male participant in the SRP-9004 clinical trial, targeting anti-limb-girdle muscular dystrophy. The intertwined use of a shared viral platform in both SRP-9004 and Elevidys therapies has intensified apprehensions regarding a potential systemic safety risk inherent in Sarepta's overarching gene therapy platform. Compounding these issues, the delayed disclosure concerning a patient fatality linked to the SRP-9004 trial, accompanied by incongruent statements about the halt of Elevidys sales, has severely undermined investor confidence in the strategic governance of Sarepta's executive management.

On July 28, FDA granted approval for the company to recommence distribution of Elevidys, albeit exclusively for outpatient use. Despite this development, the drug's market demand may face downward pressure due to growing concerns over the credibility and robustness of its safety data. Furthermore, the company's previously announced cost-reduction strategy, projecting annual savings of $400 million, might fall short of the requirements needed to comply with the covenants on its $600 million credit facility and to address over $1 billion in debt maturing in 2027. The extent of the liquidity risk is contingent upon the speed at which Elevidys sales can be restored and the steadfastness of the patient community. Although the reinstatement of Elevidys distribution marks a positive step, an urgent imperative remains for the company to fortify its long-term product pipeline.

Revenue Analysis by Product Type: Elevidys, PMO Portfolio, and Other Sources

Source: Sarepta’s SEC Filings and corporate materials

Tesla

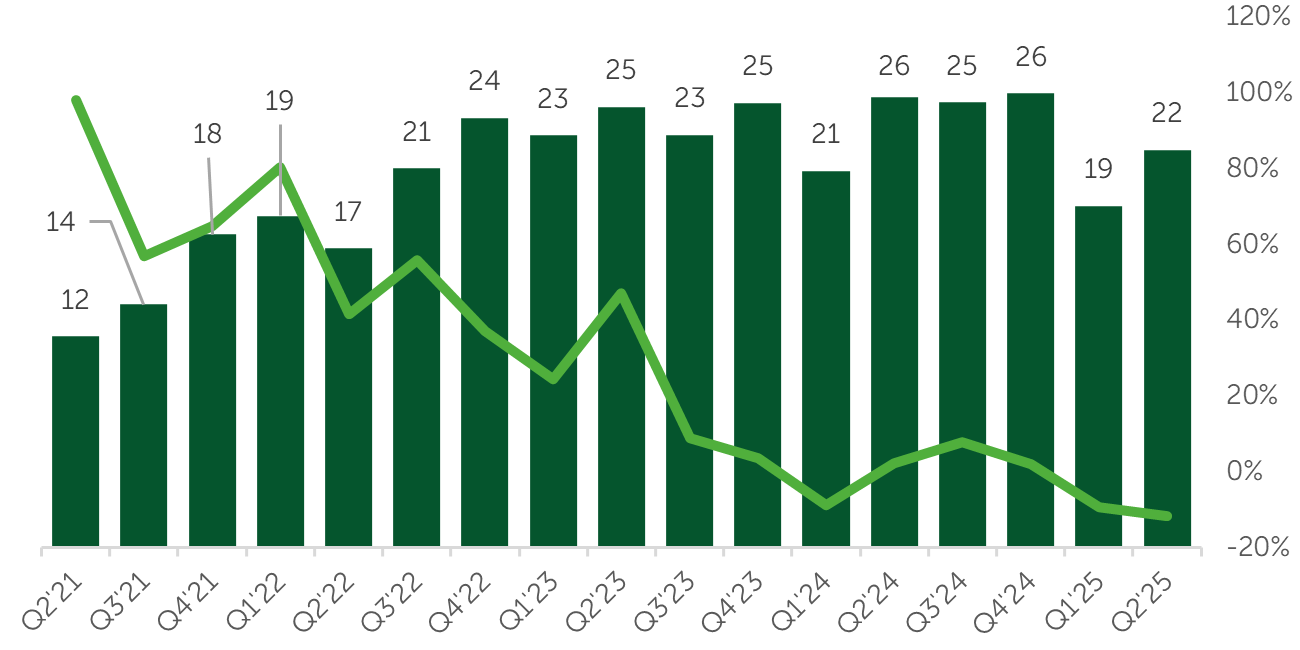

Despite the successful launch of the unmanned cab service, Robotaxi, in the United States, Tesla, Inc. (TSLA) faced financial headwinds as reflected in its Q2 2025 earnings report, disclosed on July 23. The company recorded revenue of $22.49 billion for the second quarter, representing an 11.8% decline from the corresponding period in the previous year —marking the sharpest year-over-year revenue drop in a decade. This downturn was driven by diminished sales of electric vehicles and reduced revenue from regulatory credits. However, the company's net income per share was reported at $0.40, slightly surpassing analysts' projections of $0.38.

While Tesla's quarterly earnings surpassed consensus estimates, the company faces potentially challenging quarters ahead. Starting in the fourth quarter, the U.S. will withdraw incentives for purchasing new electric vehicles, which currently provide up to $7,500 per vehicle. This policy change is likely to negatively impact demand for Tesla's electric cars.

Quarterly Tesla Revenue ($ Billion) and Year-on-Year Growth (%) Trends

Source: company data

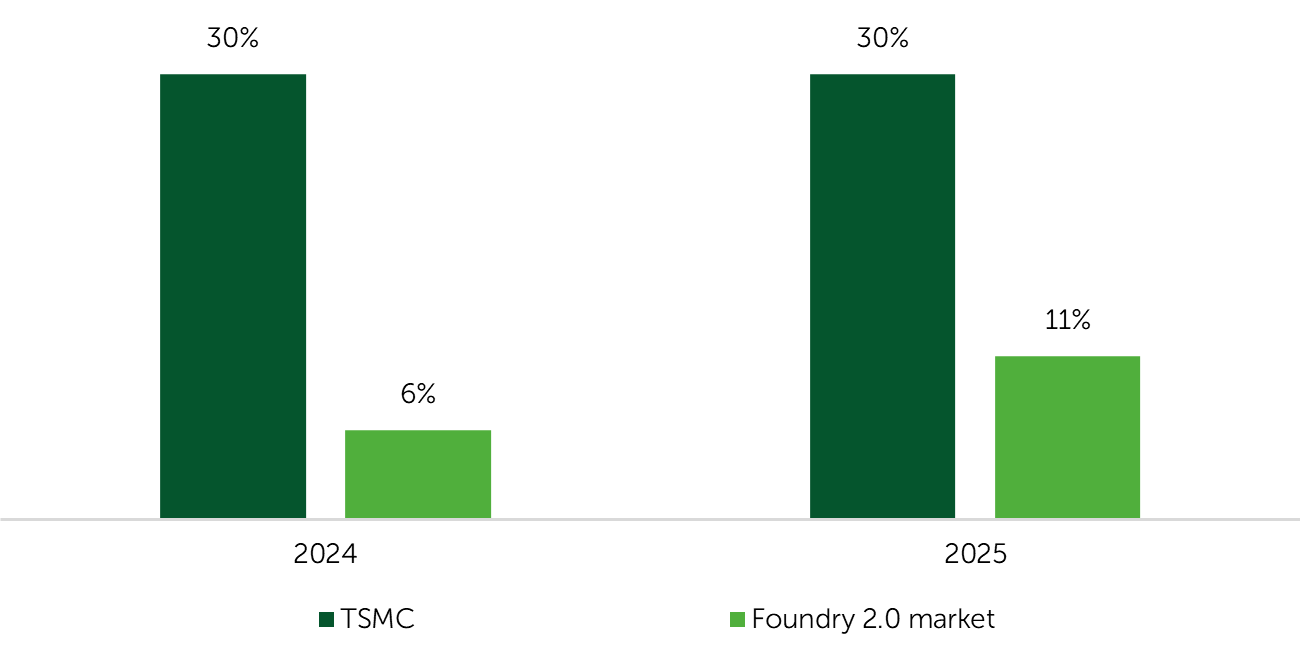

Taiwan Semiconductor Manufacturing Company

On July 17, Taiwan Semiconductor Manufacturing Company (TSM-US) announced robust Q2 FY 2025 results, surpassing its forecasts and market expectations. Driven by strong AI segment momentum and a moderate recovery in other semiconductor areas, management revised its FY 2025 revenue growth forecast from 24-26% to 30%. Despite conservative projections accounting for macroeconomic and geopolitical uncertainties, the forecast does not include the potential resumption of Nvidia and AMD chip shipments to China. Although margin pressure due to the appreciation of the New Taiwan Dollar and overseas production expansion was a bit more intense than anticipated, the long-term margin targets remain steady. Management foresees the semiconductor market and foundry business exceeding initial growth estimates through 2025, setting a positive precedent for upcoming semiconductor industry reports.

Revenue growth of TSMC vs. Foundry 2.0 market

Source: TSMC, IDC, Freedom Broker