Investment Review №327. The soft power of the Federal Reserve

Review as of Augutst 25

Global Perspective

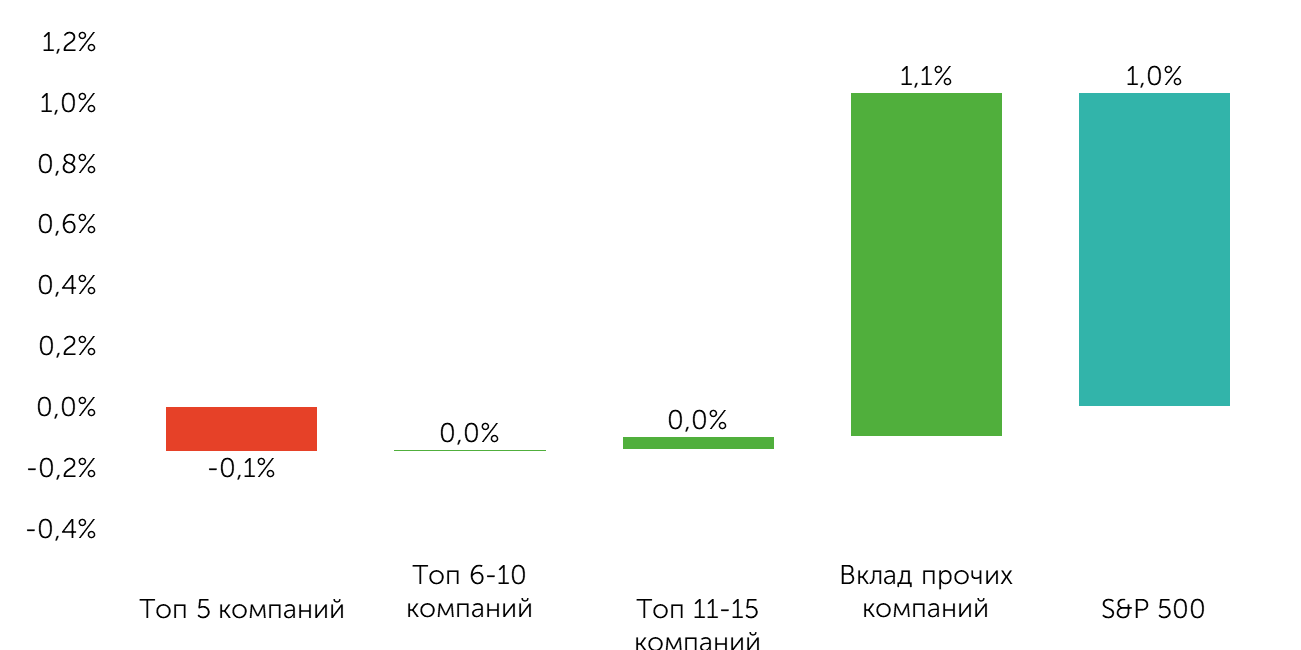

Over the past two weeks, the broad market index increased by 1%, the Dow Jones gained 3%, and the Nasdaq 100 dropped by 0.4%. The market is making another attempt to expand its rally. The Russell 2000 small cap index and the S&P 400 mid cap index achieved excess returns of 4.5% and 2.8%, respectively. Interestingly, the rotation is broad-based, with assets not only moving from larger companies to small and mid-cap firms but also shifting between sectors and factors. For instance, for the first time in a long while, the value factor is outperforming the growth factor, and a similar trend is observed in the quality and high dividend factors. From a sector perspective, there is notable profit-taking in the IT sector, and capital flows to other sectors.

Contribution of different groups of companies to the growth of the S&P 500

Source: FactSet, Freedom

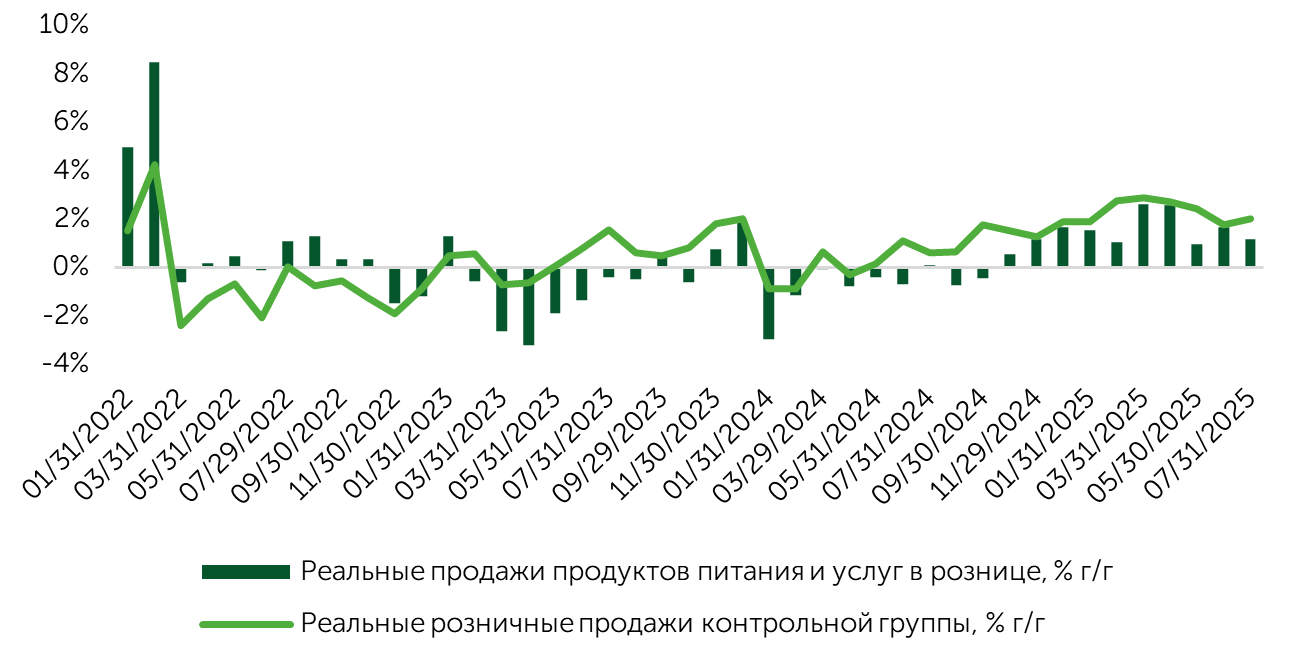

Real Retail Sales (y/y)

Source: FactSet, Freedom

Over the past two weeks, key market triggers included macroeconomic data, expectations, and the Jackson Hole summit. One major trigger was the Core CPI data, which increased by 3.1% y/y, with expectations of 3%. The markets responded very positively, as the July data did not indicate a sharp acceleration in the prices of the commodity group, excluding food and energy. This led to a reassessment of general expectations for the impact of tariffs on inflation and inflation dynamics. As depicted in the chart below, inflation expectations for the second half of 2025 have been under pressure since May-June, as concerns over a rapid price increase have gradually diminished.

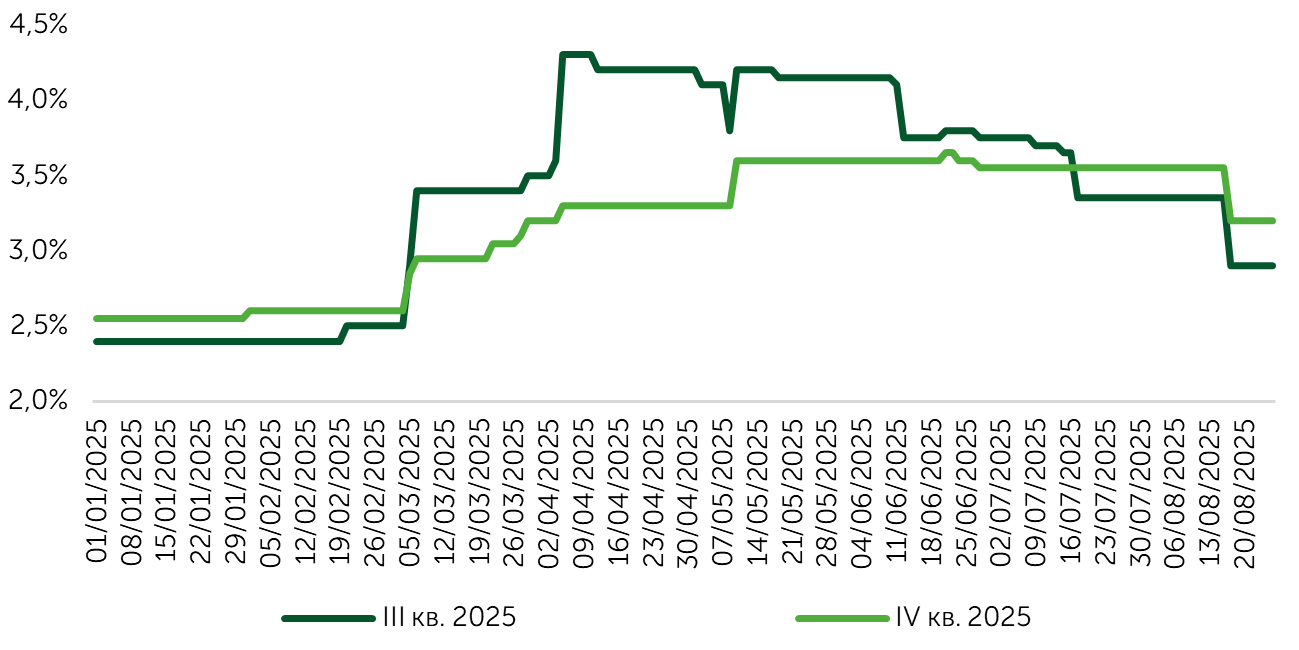

Revised Outlook for Core CPI (FactSet consensus)

Source: FactSet

In general, there has been a notable shift in inflation expectations for this year. According to FactSet’s consensus forecast, the expected peak levels for Core CPI in 2025 were initially set at 3.3% y/y versus 3.1% y/y currently. The anticipated growth for the next year is 2.9%. We believe that, as a base case scenario, Core CPI growth is likely to be around 3.1% y/y in 2025. However, we cannot entirely dismiss a scenario where price growth may accelerate in the coming months and remain elevated until year-end, potentially driving Core CPI inflation to 3.4% in 2026.

The market interpreted the Core CPI data release as a strong indication of a potential rate cut in September, with the probability currently standing at ~90%, according to CME Group. We believe that unless there is a marked acceleration in prices in August, the Fed is likely to proceed with a rate cut this year. If current trends persist, we anticipate the first rate reduction in September, followed by another one in December 2025. The shift in expectations and the increased clarity regarding the timing of rate cuts have prompted the market to rotate to assets outside the IT sector.

Despite the increased market anxiety ahead of the Fed Chair’s speech at the Jackson Hole summit, the market’s worst fears did not materialize. The regulator’s leader adopted a moderate tone, reinforcing the market’s belief in an impending rate cut. Powell also restated the thesis that both the economy and the labor market remain sustainable.

Retail sales data for July were strong, with the overall figure rising by 0.5% m/m and the previous reading being revised from 0.5% to 0.9%. Sales in the control group accelerated growth to 0.5% m/m, exceeding the expected 0.4%. Consequently, real sales in the control group grew by 2% y/y. Recent reports from major U.S. retailers were generally positive: Home Depot (HD) and Target (TGT) maintained their forecasts for the current year, while TJX Companies Inc (TJX) and Walmart (WMT) improved their revenue and earnings projections, indicating that consumer condition is not deteriorating.

Real Retail Sales (y/y)

Source: FactSet

Market Focus

Over the next fortnight, markets will be closely monitoring key macroeconomic data that could either reaffirm current expectations for a rate cut in September or prompt the regulator to another delay in monetary policy easing. Labor market data, including the unemployment rate, hiring trends, and wage statistics, are set to be released on September 5. In light of Powell’s recent remarks, the primary focus will be on the dynamics of new job openings. Currently, FactSet’s consensus forecast predicts an increase in Non-Farm Payrolls of 110k—a figure that some market analysts deem necessary to maintain the unemployment rate at its current level. Should the Non-Farm Payrolls data be weaker, falling within the 0-50k range, coupled with negative revisions of previous figures, this could significantly heighten market concerns about the economic condition, potentially prompting the Fed to implement more aggressive rate cuts in September, such as a 50 basis point reduction.

All else being equal, August’s inflation data could pose a significant obstacle to further monetary easing. Should there be a notable acceleration in commodity inflation relative to July’s data, market expectations for inflation in the coming months may alter considerably, thereby shifting the anticipated timing of rate cuts this year. Considering the current trends in Core CPI and the fact that the surge in the PPI did not affect the commodity category, and in the lack of a marked acceleration in import prices, we do not anticipate a significant uptick in inflation for August. We continue to expect two rate cuts this year, which is in line with a cooling labor market and a reduced risk of significant inflation acceleration. The materialization of a favorable scenario, with no marked acceleration in inflation and a relatively stable labor market, may encourage the market to continue rotating away from the technology sector and large-cap companies towards other market segments, including rate-sensitive niches like automakers, cyclical goods and services, real estate developers, and REITs. Additionally, there is potential for improvement in the outlook and sentiment within the small-cap segment, a trend that is already evident.

Other market catalysts may include the reports of several major technology companies, including Salesforce (CRM), Hewlett Packard (HP), Broadcom (AVGO), Adobe (ADBE), and Oracle (ORCL), that could bolster positive sentiment surrounding AI and offer further insights into the state of demand for technology products.

Technical Analysis of the Broad Market

The technical outlook for the broad market index is positive: the RSI oscillator remains out of the overbought zone, and there are no reversal patterns or notable declines in volume. The proportion of companies that have an RSI above 70 (4%) is not close to critical levels, and 65% of companies are trading above their 50-day moving average, suggesting the potential for the rally to expand further. Investor sentiment is mixed: retail investors are maintaining a net bearish exposure, whereas professional managers exhibit a bullish sentiment, suggesting a potential increase in positioning in U.S. equities.

Expected Trading Range

We anticipate the S&P 500 index to move within a range of 6,400-6,550 points.