Financier №1 (41) 2026

Vladimir Chernov

Analyst, Freedom Finance Global

Investing Beyond Myths

How to Select Exchange‑Traded Instruments Aligned with Your Goals - Break the Mold!

It is widely believed that women, when trading on the stock market, are on average more cautious than men and tend to avoid risk. This stereotype is usually presented as a neutral observation, but in practice it can influence how financial solutions are offered to women.

Caution as a Trap

In recommendations targeted at women traders, there is often a stronger emphasis on maximally conservative instruments, while discussion of alternatives or independent decision‑making takes a back seat.

By stereotypes here, it means not personal beliefs, but the persistent expectations of society as a whole: business consultants, financial media, and even one’s close social circle. These expectations create a backdrop against which investing is often framed as a complex - and therefore “not quite suitable for women” - topic. As a result, some women may experience a decline in confidence in their own abilities, even when they have both the interest and the willingness to engage with the subject.

Risk Appetite

The gap between the desire to engage in investing and actual participation in trading transactions is also supported by survey data. In developed countries, women are just as likely as men to express a desire to invest, but they more often postpone getting started due to uncertainty about their own knowledge. Meanwhile, according to recent Bloomberg data, in China, for example, women manage funds totalling nearly $1 trillion. Furthermore, 3 721 funds with female involvement in management have delivered positive returns over the past year.

Sometimes, when discussing differences in investment behaviour, biological factors are also mentioned. A number of scientific studies have shown that risk appetite is influenced by testosterone. Individuals with higher levels of this hormone tend, on average, to make risky decisions more easily, while at low levels of the hormone, gender differences in such behaviour practically disappear. However, the authors of these studies themselves emphasise that the hormonal status of a potential investor cannot be considered a determining factor. Access to information, the quality of financial advice, income levels, and career breaks have a far more significant impact on investment strategies than biological factors.

Excessive caution in this context has clear consequences over long time horizons. According to data from the analytics firm Morningstar, in the US market from 2013 to 2023, model long‑term portfolios with a large equity allocation on average delivered higher returns than strategies focused primarily on bonds and cash instruments.

These differences do not depend on the investor’s gender. They merely reflect a general principle: avoiding risk reduces portfolio volatility but simultaneously limits its growth potential.

A Portfolio for the Conservative Investor

If we assume that predictability and psychological comfort are a priority for the investor, it is logical to start with a simple portfolio structure. This strategy is especially suitable for those who are just beginning to invest and are not yet ready for sharp fluctuations in asset values. The foundation of such an investment portfolio usually consists of bonds - debt securities that, in essence, represent a loan provided by the investor to the government or a company for a predetermined period at a fixed interest rate, generating guaranteed income. These securities can account for 50 % to 80 % of the total portfolio. Bonds are well‑suited for goals with a set timeframe - for example, saving for education or a major purchase in several years.

However, risks still exist here. The issuer may face financial difficulties and delay coupon payments or principal repayment. Additionally, if the issuer’s credit quality deteriorates, the market price of the bond may decline. Furthermore, when market interest rates rise, the value of previously issued bonds typically falls. Therefore, over the short term, the key criteria become not maximum returns, but the borrower’s reliability and the time to maturity.

The second element of such a portfolio typically includes shares of large, stable companies - the so‑called “blue‑chip” stocks. These are businesses with a long track record, stable earnings, and a clear business model. A classic example is Alphabet (GOOGL) shares, which have appreciated 8.5‑fold (+747 %) over the past 10 years, driven by steady growth in the advertising and cloud computing businesses. Another example is NVIDIA (NVDA) securities, which have risen 14‑fold (+1308 %) over the past five years, amid the boom in artificial intelligence and high‑performance chips. The share of such stocks in the portfolio may be relatively small, but they provide the chance to grow capital above inflation and support long‑term returns.

This group also includes “dividend aristocrats” - issuers that have consistently distributed profits to their shareholders for many years and regularly increased the size of these payments. Classic examples in international markets are Coca‑Cola (KO) and Johnson & Johnson (JNJ), which continue to pay dividends even during economic downturns. Such securities provide portfolio protection in case of a decline in the value of other securities, as they continue to generate passive income in the form of dividends, regardless of market trends. They can account for 20–30 % of a conservative portfolio.

In 2025, the price of an ounce of gold increased by $1,694.45, which is more than 64%. Over the year, the metal reached historical highs more than fifty times.

As a complement to this set of assets, gold or exchange‑traded funds (ETFs) tracking this metal are often included. This instrument does not generate regular income, but it reduces the overall portfolio risk during periods of high geopolitical or economic uncertainty and serves as a hedge against market stress. Cautious investors typically allocate an average of 10–30 % of the portfolio to hedging assets - instruments that protect against risks.

For those who do not wish to select individual securities manually, exchange‑traded funds (ETFs) are available. The easiest way to think of them is as a ready‑made basket of assets assembled according to specific rules. In practice, an ETF mirrors the performance of a chosen asset or index. For example, a gold or silver ETF tracks the prices of the respective metal, while a fund tracking the S&P 500 or NASDAQ index reflects the performance of the largest US companies. There are also funds focused on the global equity market, specific regions such as Europe or emerging markets, as well as those based on bonds or mixed assets. By purchasing a single instrument, an investor gains access to a diversified portfolio and is relieved of the need to monitor constantly the balance. Such funds are especially convenient for long‑term goals - temporary dips in quotes should not become a reason to make emotional decisions.

Choosing the Time Horizon

The investment horizon plays a key role in portfolio construction. If your goal is to earn on investments within one to two years, it is better to opt for the most stable instruments and not chase high returns - that is, allocate the majority of the portfolio to bonds. For a timeframe of three to five years, you can combine bonds and defensive assets with a small share of equities, including growth stocks. For even longer‑term goals, it is reasonable to build the foundation on equity funds, supplementing them with a defensive component to weather market fluctuations without stress (for more details on the composition of a long‑term portfolio, see pp. 36–37).

There is another important criterion that is discussed less frequently. An investment strategy must be psychologically feasible. If the portfolio you have built causes you to constantly check quotes and worry about every market movement, the risk of mistakes increases. In this sense, simplicity and clear logic often prove to be no less important than returns as such.

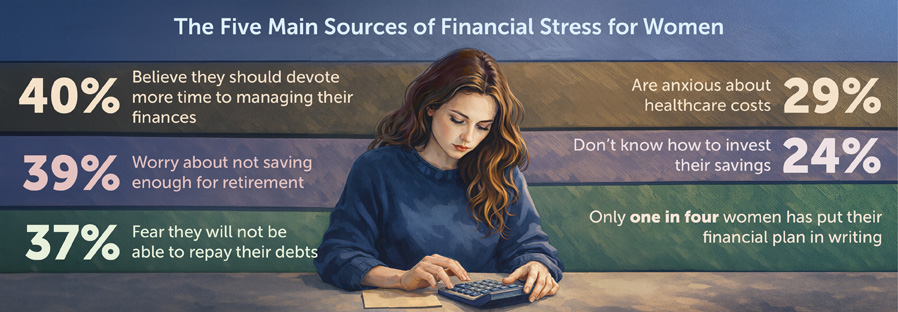

Source: Fidelity Investments, Women’s Study (October 2023)