Investment Review №328. Waiting for change

Corporate News In Focus of Our Analysts

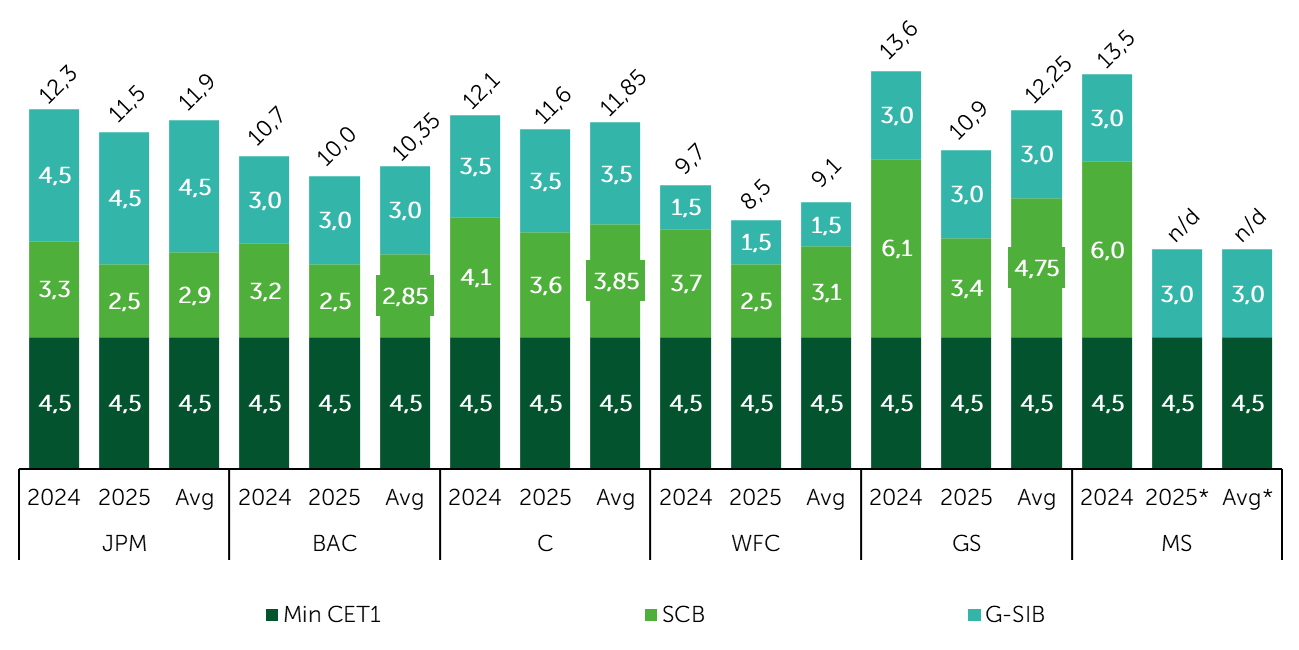

Capital Requirements for Leading U.S. Banks

On August 29, the Federal Reserve finalized individual capital requirements for the largest U.S. banks, effective October 1. The CET1 ratio remains composed of the 4.5% minimum base, the stress capital buffer (SCB) from the annual stress test, and the global systemically important bank (G-SIB) surcharge. The updated requirements reflect the 2025 stress test outcomes: major banks maintained capital cushions even under a severe recession scenario, although the SCB allocations vary significantly. Morgan Stanley (MS) is currently undergoing a buffer review, with a decision expected by the end of September.

The regulator emphasizes the transitional nature of the current requirements. In April, it proposed averaging stress test results over two years to reduce SCB volatility. However, this approach would be unfavorable for the largest U.S. banks: in every case, the averaged requirement would exceed the current 2025 thresholds, leading to an increase in the overall CET1 ratio (see Chart).

Thus, the current regulations temporarily allow for a greater easing of capital requirements, but once the averaging methodology is finalized, the sector may face an increase in capital demands (relative to the updated levels) within the coming months. For banks, this implies more restrained buyback and dividend activity, while investors face the risk of downward revisions to return on equity expectations.

CET1 Capital Requirements: Actual Levels for 2024–2025 and Hypothetical Scenario Based on SCB Averaging

Source: federalreserve.gov, analysis by Freedom Broker

Note: "Avg" represents the hypothetical CET1 level assuming the Fed’s proposal to average the stress capital buffer (SCB) over two years is approved.

* For Morgan Stanley, the 2025 SCB is currently under review and will be announced by the end of September 2025.

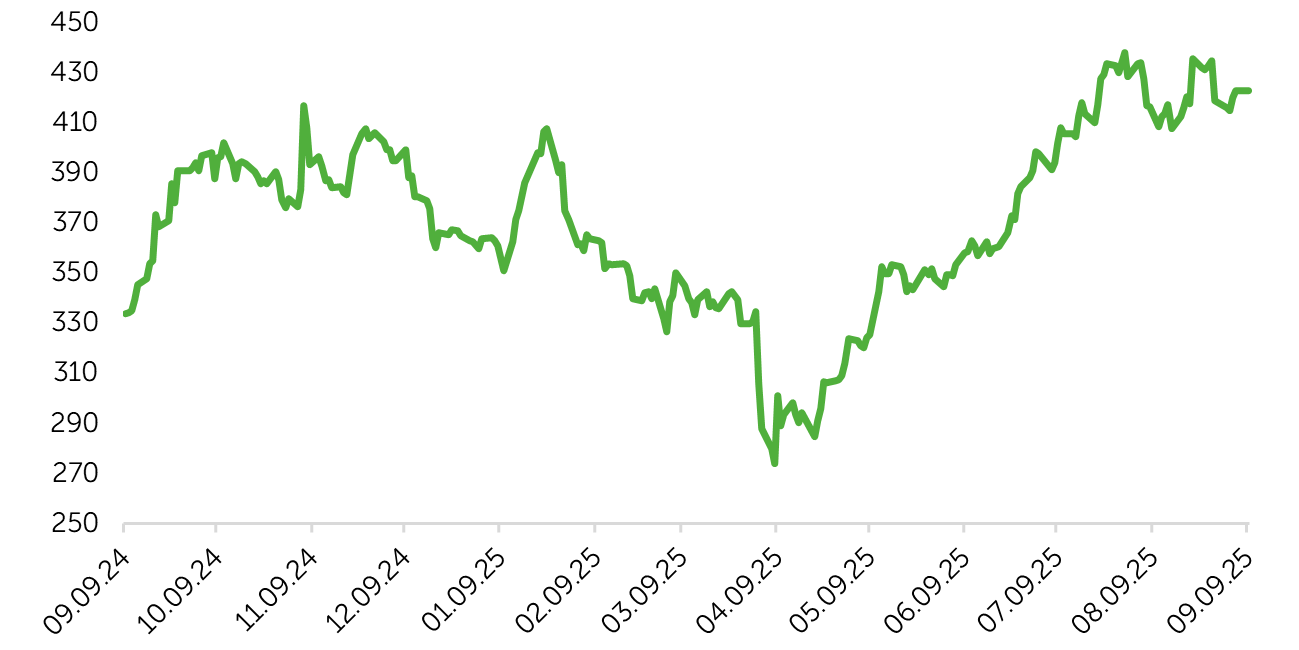

Caterpillar

On August 28, Caterpillar Inc. (CAT) provided an updated outlook on the anticipated impact of tariffs on its financial results. Based on revisions and clarifications announced after August 5, 2025, and expected to take effect from August 31, 2025, the company now estimates the net impact of additional tariffs imposed in 2025 to be approximately $500 million to $600 million for Q3 and roughly $1.5 billion to $1.8 billion for the full year 2025.

Taking into account the net impact of additional tariffs, the company now expects its adjusted operating margin for the full year to be closer to the lower end of the target range. The revised tariff impact estimates are not expected to affect the previously issued sales and revenue guidance.

Caterpillar (CAT) stock performance for 2024–2025

Source: FactSet

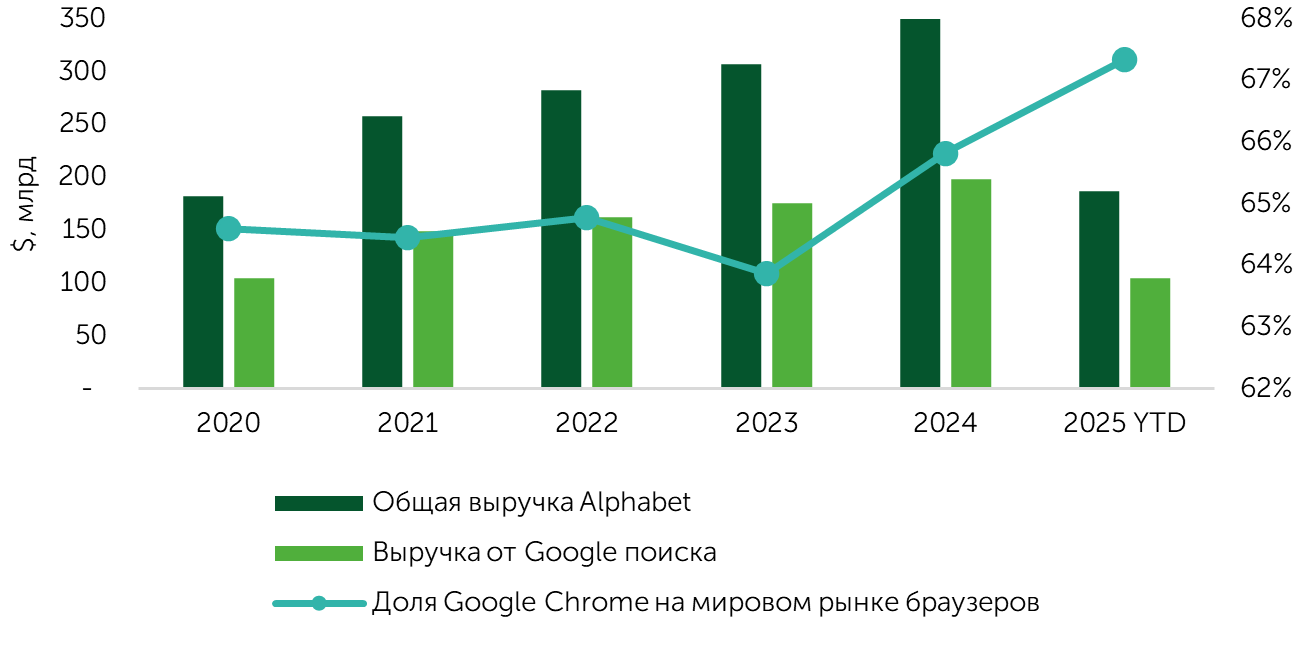

Alphabet

On September 2, a U.S. federal court delivered its verdict in a lawsuit against Alphabet (GOOGL). Judge Amit Mehta ruled that the company is not required to divest Chrome and Android, as initially demanded by the U.S. Department of Justice (DOJ). Additionally, the court did not prohibit Alphabet from making payments to partners, such as Apple, for positioning Google as the default search engine. However, these partnership agreements need to be renegotiated on an annual basis. The court has also prohibited exclusive distribution agreements for Search, Chrome, Google Assistant, and Gemini. Furthermore, Alphabet is required to provide limited access to search queries and user data to “qualified competitors,” including AI firms, to promote competition. These measures aim to prevent Google’s dominance in search from transitioning automatedly into the AI domain. The court’s ruling, without dividing Google’s business, aligns with the expectations of most market participants, and the behavioral covenants imposed were even less stringent than anticipated.

Revenue from Google Search and Google Chrome's share of the global browser market

Sources: Alphabet Inc., statcounter.com

Lululemon Athletica

LULU (LULU) stock has lost more than 60% of its value since the beginning of 2024. Once valued with price targets exceeding $800, the stock now struggles below $300. LULU’s aggressive expansion strategy, encapsulated in the Power of Three ×2 program, aimed to double revenue by 2026. Initially impressive, the sales growth rates were between 25% and 30% y/y. This year, the growth rate has dipped below double digits, and the company is finding it increasingly difficult to maintain its growth momentum. Despite this, capital expenditure has increased by ~20%. Currently, robust sales are only being seen in China, while the domestic market has deteriorated significantly, posting negative comparable sales for the first time.

Investor confidence in Lululemon’s growth prospects is waning, as evidenced by a rise in short interest to 6-7%, which is twice as high as Nike’s. Tariffs add to the uncertainty, though the company has yet to detail the expected impact on its business, merely acknowledging the possible increase in retail prices.

So far, profitability remains relatively high, with a net margin exceeding 10%, which is twice that of Nike. However, should this advantage diminish, the correction in the stock price is likely to continue.

Revenue dynamics, y/y

Source: FactSet

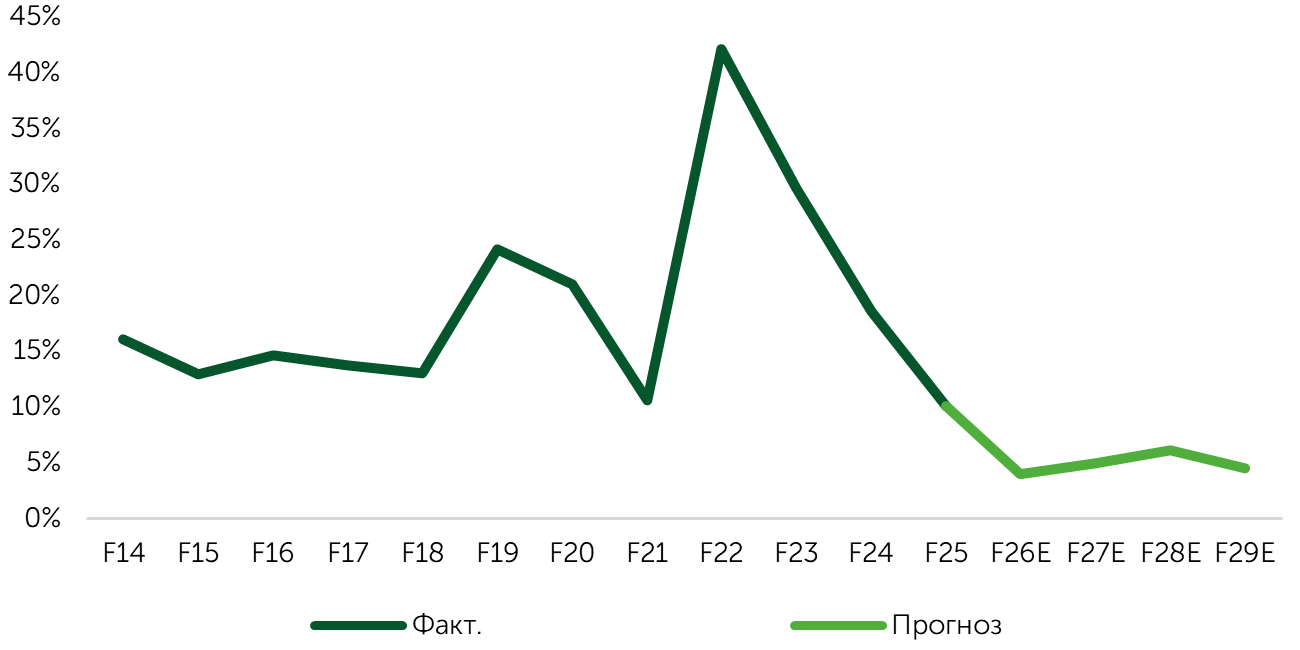

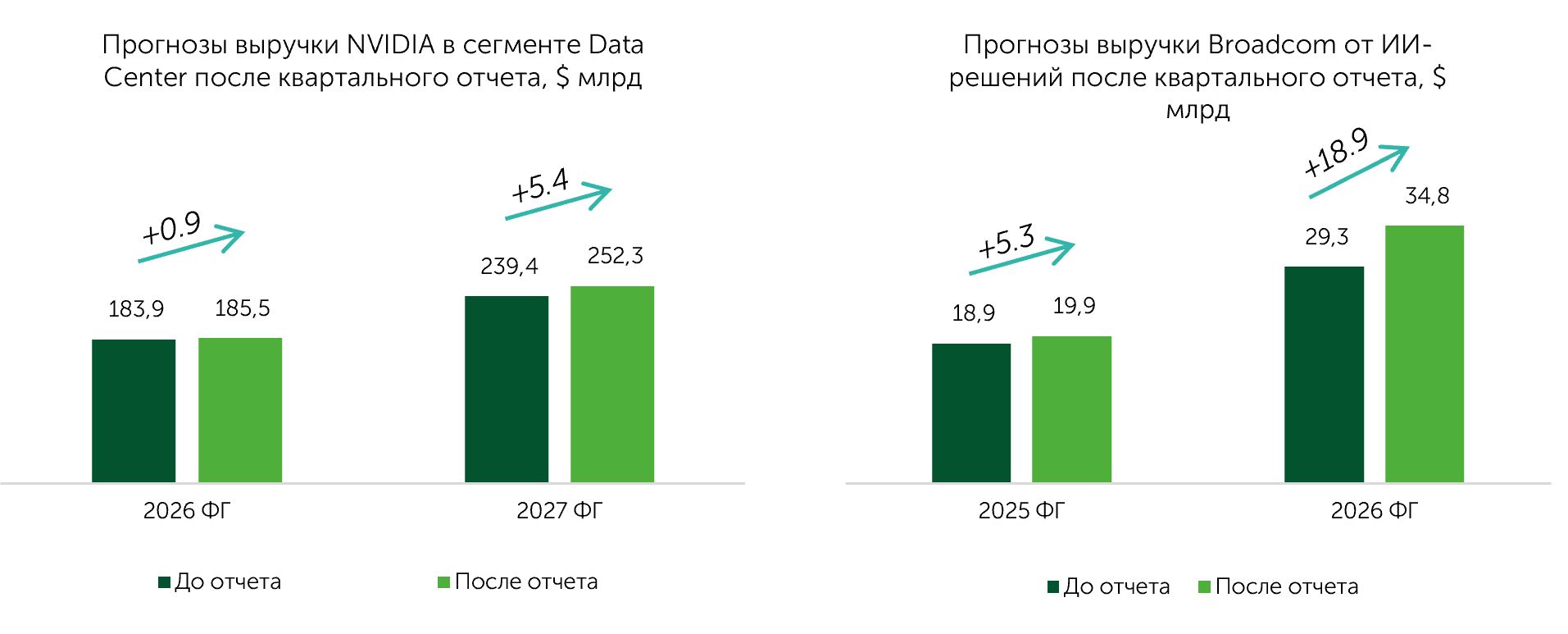

NVIDIA, Broadcom

In recent weeks, Nvidia Corp. (NVDA) and Broadcom Inc. (AVGO), the two largest suppliers of AI infrastructure components, released their quarterly reports. Despite both companies posting positive surprises, investor reactions were starkly different. Nvidia surpassed expectations across all metrics, yet its stock entered a correction phase because its data center segment’s results did not exceed investor projections for the second consecutive quarter. This underperformance was attributed to the restrictions on AI chip shipments to China. Although the U.S. provided authorization last quarter, shipments to customers have not yet occurred. Management’s guidance for this quarter did not include the anticipated $2.0-5.0 billion in revenue from shipments to China but still surpassed investor consensus estimates. Aside from this situation with China, the company confirmed robust momentum in its AI segment. CEO Jensen Huang has already increased his guidance for global AI infrastructure investment to $3.0-4.0 trillion by 2030, up from a previous estimate of just $1.0 trillion by 2028. Broadcom’s report also delighted investors with strong financial results and positive guidance for the quarter. However, the surge in AVGO’s stock price was driven by the announcement of a $10 billion contract to develop custom AI chips for a new client, OpenAI. As a result, Broadcom adjusted its FY 2026 forecasts. While management had previously expected a growth rate of 50-60% y/y in AI revenue, comparable with FY 2025, they now foresee faster growth.

Broadcom's AI solutions revenue forecasts following quarterly report, $ billion

Sources: earnings releases, FactSet, Freedom Broker