Investment Review №328. Waiting for change

LONG PUT ON RBLX

Investment Rationale

Roblox Corporation (RBLX) is a platform of user-generated content and social interaction with a large audience (DAU, engagement hours). While the company shows significant growth in both engagement and bookings, it is still vulnerable to regulatory and litigation risks concerning child safety, as well as to the risk of ineffective engagement translation into sustainable monetization.

Investment Idea

Purchasing a put option with a strike of $130 represents a speculative bearish position, anticipating a significant worsening in sentiment about RBLX (potential legal issues, unsuccessful ad monetization / ARPU or disappointing quarterly results). Such developments will lead to a drop in the stock price and/or an increase in implied volatility. The expiration date of November 21, 2025, allows time for these negative triggers to potentially materialize.

Key Arguments

- Regulatory and Legal Vulnerabilities. Ongoing child safety issues and active lawsuits create a real probability of incurring fines, regulatory restrictions, or reputational damage—all of which can swiftly affect monetization efforts and increase IV.

- Risk of Monetization Failure. Despite growth in DAU and hours, the primary challenge lies in scaling ARPU and ad monetization. Shortfalls in these key metrics often act as a significant catalyst for downward valuation adjustments.

- High Valuation and Expectations Sensitivity. The stock is trading at a premium due to expected growth. Without validation of these expectations or in the event of a negative surprise, the market can rapidly reduce the multiple, exacerbating the decline in stock price.

- Volatile Stock Profile. Historically, RBLX has exhibited sharp price movements in response to news. Price declines combined with IV growth can swiftly increase the put option’s value more substantially than the net decline of the underlying value reflects.

| Strategy | Long Call |

| Ticker of the Underlying | RBLX |

| Recommendation | BUY |

| Strike and Option Type | PUT $130 |

| Expiration Date | 21.11.2025 |

| Current Price (Mid) | 14,525 |

| Strategy Cost | $1 452,50 |

| Greek Parameters | Delta – -0,454 Gamma – 0,011 Vega — 0,228 Theta – -0,090 |

| Implied Volatility | 61,61% |

| Realized | 1М – 45,24% 3М – 50,41% 6М – 49,65% 12М – 48,94% |

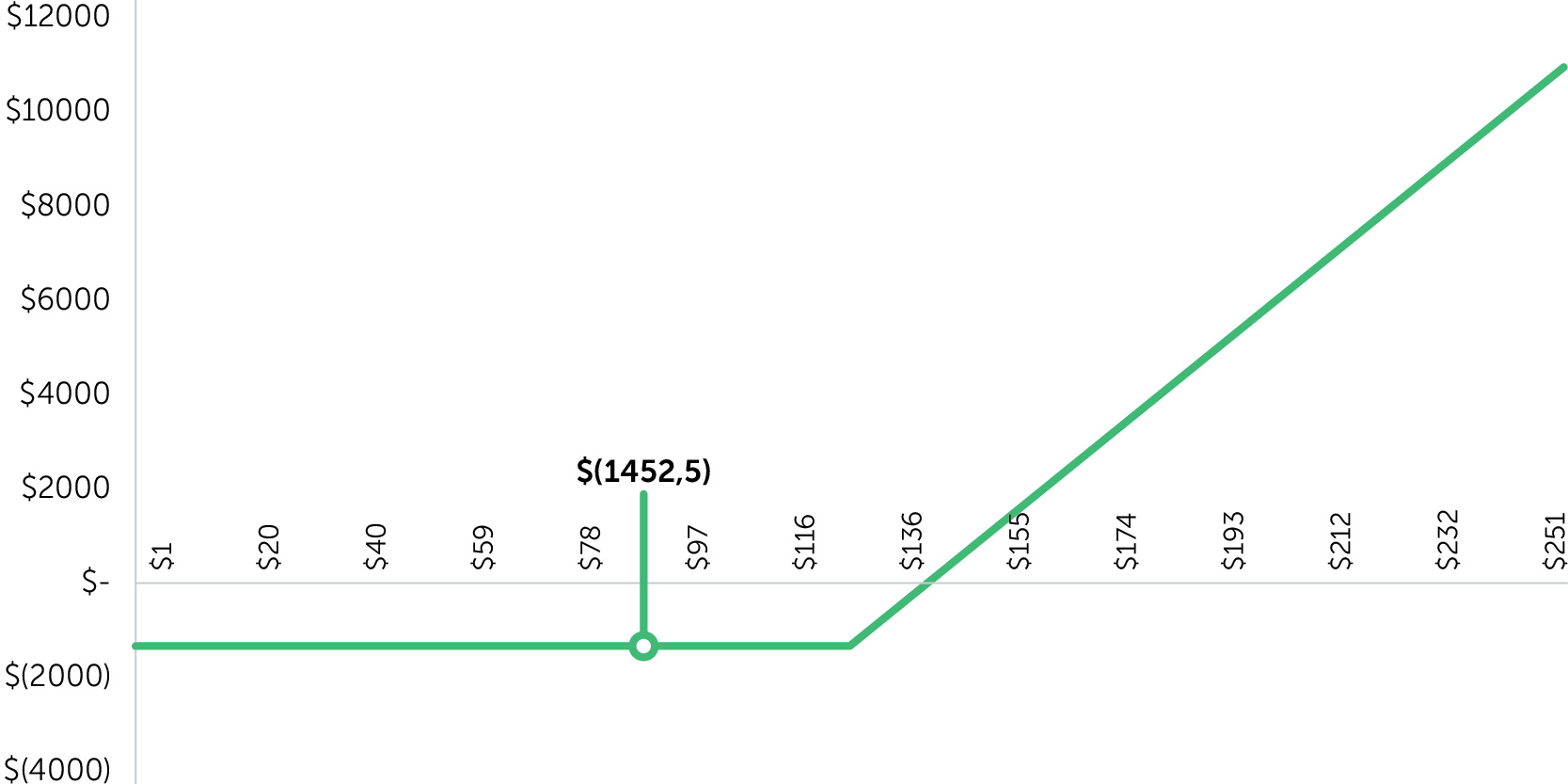

P/L of the option strategy

Trade Parameters

| Strategy | Long Call on RBLX |

| Strike | Long PUT 130 |

| Buying | +RBLX*FBL130 |

| Exp Date | 21.11.2025 |

| Margin Requirement | $1453 |

| Entry Price | $2150 |

| Max Prifit | $Inf |

| Max Loss | $(1453) |

| Expected return | 48% |

| Breakeven Point | $115,48 |

Position Management

On the expiration date of 21.11.25, if the underlying asset’s price is below $130 but above $115.48, the investor will incur a variable loss. Conversely, if the asset’s price surpasses $130, the investor will experience a maximum loss of $1,453. Should the underlying asset’s price exceed the breakeven point of $115.48, the potential profit is unlimited. However, we advise closing the position when the call option’s value reaches $2,150.