Investment Review №328. Waiting for change

Review as of September 8

Global Perspective

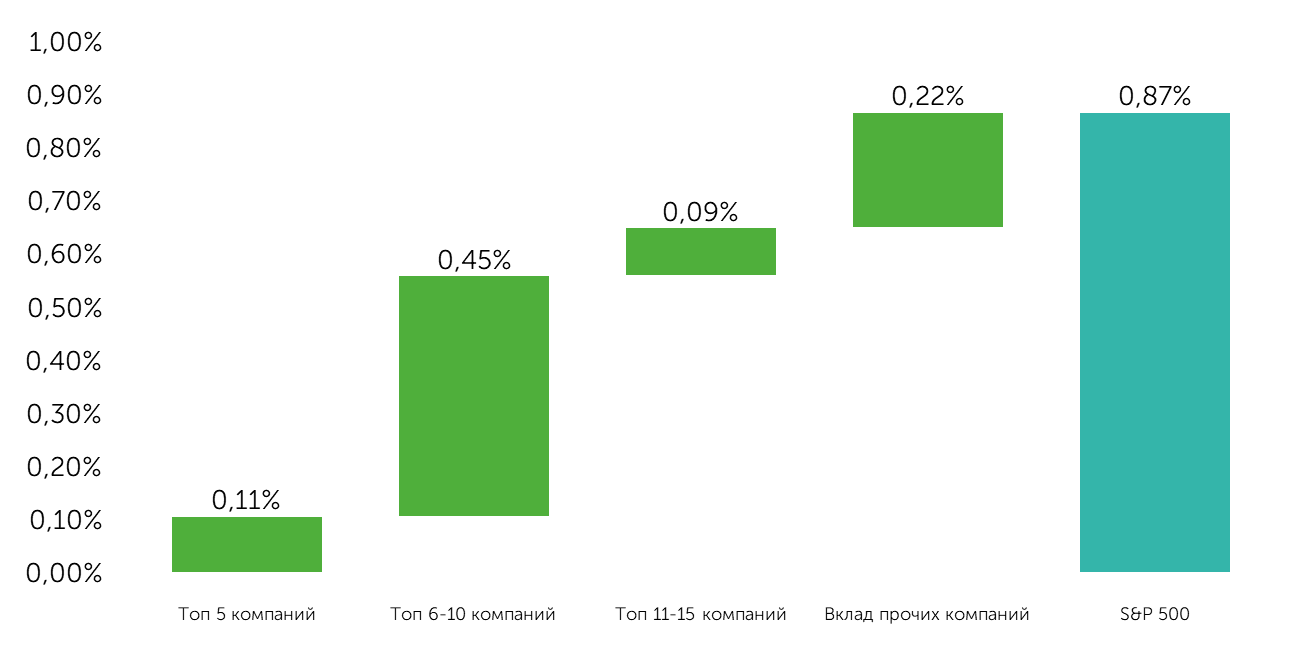

Over the recent two-week period, the S&P 500 Index experienced a 0.9% increase, the NASDAQ 100 rose by 1.4%, and the Dow Jones gained 0.5%. A noticeable rotation from large-cap stocks to small and mid-cap equities persisted, evidenced by a 1.7% excess return of the Russell 2000 Index and a 1.1% gain in the MidCap 400 Index. Notably, index growth remains highly concentrated, with the top 15 companies accounting for 75% of the total index growth during this timeframe.

Group Contributions to S&P 500 Index Dynamics

Source: FactSet, Freedom Broker

Over the past two weeks, the market has been experiencing significant turbulence as it grapples with the issue of increased government intervention in the economy. The decision by Trump's administration to acquire a 10% stake in Intel (INTC), coupled with the Pentagon's prior equity investment in REM mining company MP Materials (MP), has intensified these concerns. Additionally, speculation persists regarding the Federal Reserve's ability to maintain its independence in policy-making amid ongoing pressure from Trump, both verbal and actionable. This is underscored by the recent removal of Lisa Cook from her position, following charges related to mortgage loan fraud.

The corporate news landscape remained robust, with notable developments across various sectors. On the positive side, companies benefiting from advancements in artificial intelligence, such as NVIDIA (NVDA), Broadcom (AVGO), and Oracle (ORCL), reported strong performance. Conversely, challenges were evident within the Consumer Discretionary sector. Tesla, for instance, faced a downturn with a reported 40% decline in new car registrations in Europe in July. Lululemon also highlighted a drop in demand, particularly in the U.S., where comparable sales fell 3% y/y. However, one of the most impactful developments in market dynamics was Alphabet's (GOOGL) significant gain—its shares rose 8% on September 3 after a favorable court ruling allowed it to retain key assets. This was despite an extended period of accusations regarding market monopolization in its key operational areas.

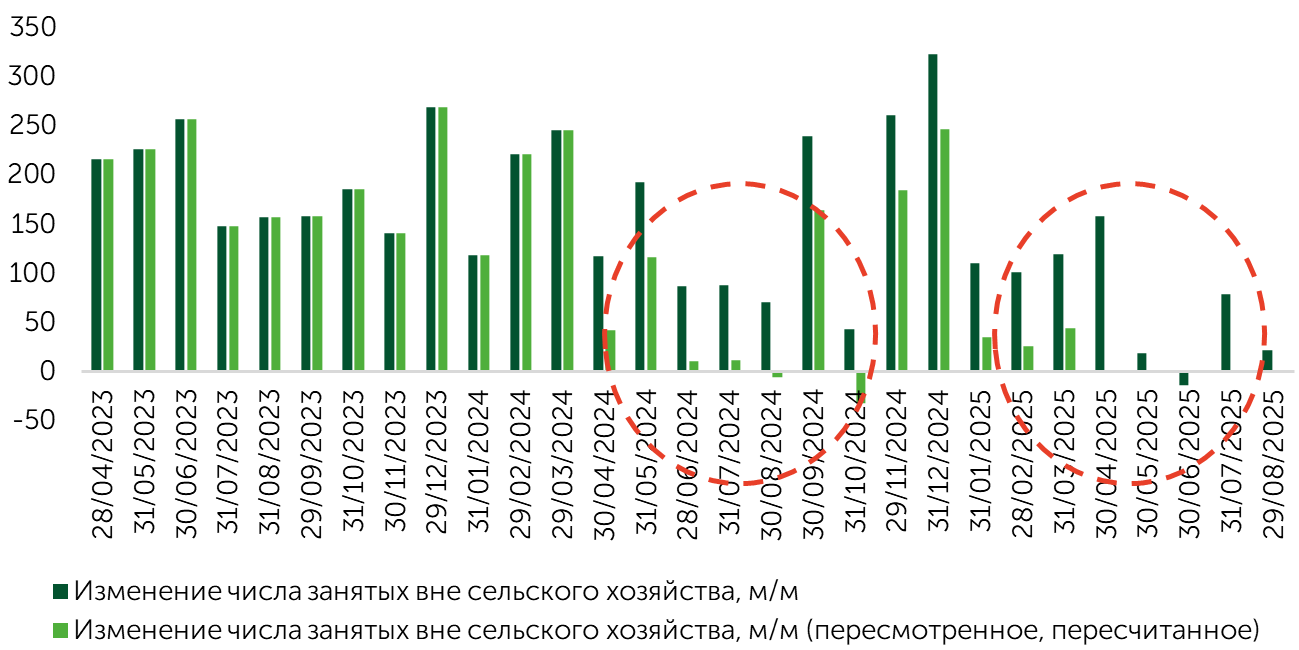

The focal point of the market was labor market data, which continued to trend towards a significant cooling, with risks escalating. Notably, in August, job openings rose by 22,000, falling short of expectations of a 75,000 increase (the previous figure was marginally revised from 73,000 to 79,000). Following a partial recovery in July after particularly weak periods in May and June, the August data once again point to a substantial deterioration in hiring dynamics. Additionally, July's open job positions were reported at 7.18 million, missing the anticipated 7.38 million and subsequently revised down from an initial reading of 7.43 million to 7.36 million. This reaffirms the ongoing trend of declining job openings, suggesting weakness on the labor demand side. It is also noteworthy that the job openings data for the April 2024-March 2025 period was revised downward by 911,000 on September 9, indicating that the labor market issues are more systemic. These challenges are not only prompted by increased uncertainty due to tariff risks but are also likely exacerbated by the U.S.'s stringent monetary policy. Meanwhile, despite slower hiring, there has been no significant reduction in staffing levels, suggesting that while overall labor market conditions have deteriorated, they are not dire.

Monthly Variation in Non-Agricultural Employment Numbers

BLS, FactSet, Freedom Broker

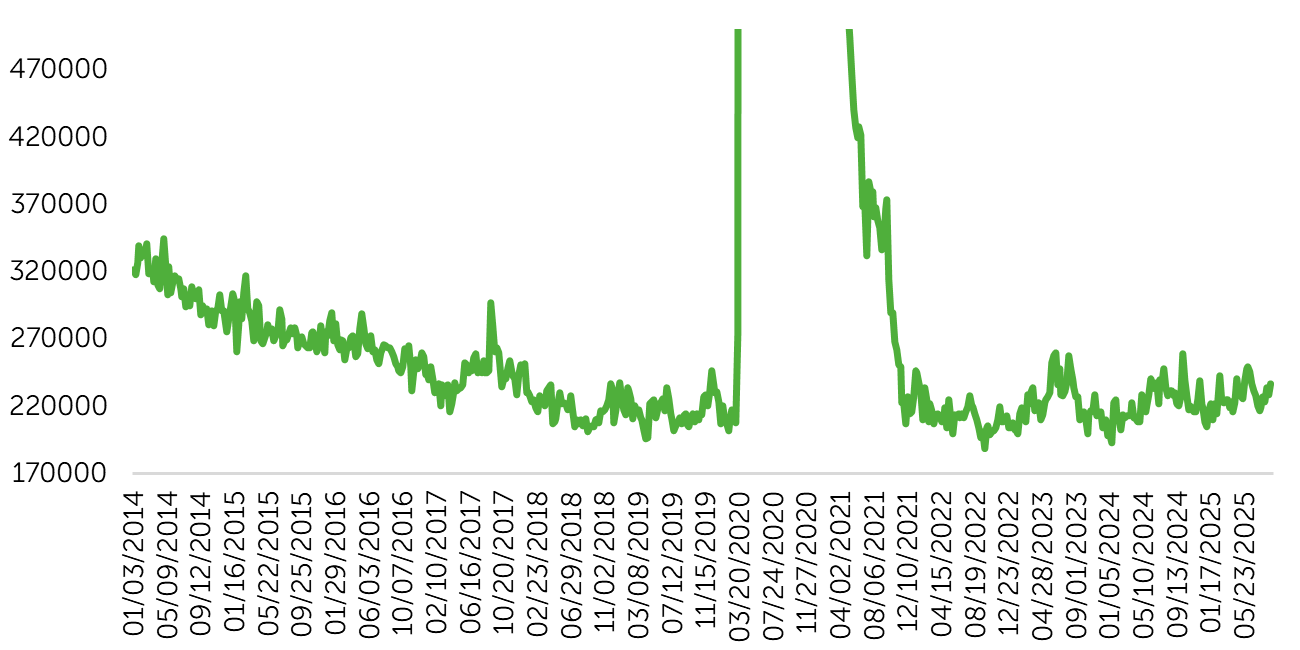

U.S. Weekly Initial Jobless Claims Report

U.S. Department of Labor, FactSet

The release of notably weak employment data in the U.S. for August led to only a minor correction in the market but significantly increased the likelihood of a rate cut at the Federal Reserve's next meeting. Furthermore, it elevated the chances of a more substantial rate reduction of 50 basis points. Currently, the market perceives the situation as: economic activity has decelerated, and while the labor market has softened, it has not reached a crisis point. Consequently, the market is pricing in a potential improvement in macroeconomic conditions, driven by anticipated rate cuts from the Federal Reserve, which remains the central focus of market participants.

Market Focus

The Federal Reserve meeting in the coming two weeks stands as the central event, with the market currently anticipating a 25-basis-point rate cut. We are similarly inclined to believe that the Fed will refrain from opting for a 50-basis-point cut. Such restraint is primarily to avoid alarming market participants, as a deeper cut could be perceived as an acknowledgment of substantial issues within the labor market and potential economic fragility. Nonetheless, we cannot completely discount the possibility of this action, given the Fed's precedent of more rapid policy easing a year prior. This meeting holds significant weight also because the Fed will release updated economic, inflation, and interest rate forecasts. These updates could considerably influence key market narratives. Ideally, investors would favor the maintenance of current forecasts for economic activity, allowing for only a slight deterioration in labor market assessments and showing some improvement in inflation projections, which would ideally not indicate the significant acceleration that was previously feared due to the rate effect.

As we approach the end of the month, the retail sales data for August will play a crucial role in evaluating the current state of consumer activity. A deceleration in consumer spending may indicate heightened risks to the economy, particularly in light of a cooling labor market. During this period, investors will also closely monitor the dynamics of industrial production, orders for durable goods, and PMI data. The primary focus will likely be on employment trends and inflation estimates.

As previously noted, potential easing of monetary policy could positively impact rate-sensitive sectors and niches, such as durable goods, industrials, commodities, financials, household goods, automotive, and homebuilders. However, considering the ongoing deterioration in the labor market and recent reports from major IT companies indicating continued strong momentum in the AI niche, expectations of double-digit EPS growth over the next two years remain supported. This suggests that any sector rotation might be sluggish and could result in only localized lags for technology versus rate-sensitive niches. The technology sector benefits from robust internal drivers unrelated to the general economic climate. Therefore, we advise a cautious and gradual increase in exposure to rate-sensitive market segments.

Despite indications of systemic strain in the labor market, we do not perceive the situation as a full-blown crisis. Layoff dynamics remain robust, and recent trends can largely be attributed to recent tariff policies. The prevailing economic patterns suggest a deceleration yet persistently strong demand, anticipated to be bolstered by OBBBA. We project that this could potentially contribute an additional 0.2-0.3% to GDP growth in the coming year.

Small-Cap Stocks

Over the past two weeks, the small-cap segment has consistently outperformed the broader stock market. The Russell 2000 Index (ETF: IWM) advanced 5.4%, the S&P Small Cap 600 Index (ETF: IJR) climbed 4.2%, and the Russell Microcap Index, which tracks micro-capitalized companies (ETF: IWC), recorded a 4.9% gain. This robust performance from the small-cap equity sector significantly exceeded the S&P 500's return by more than 3 percentage points. The data suggests a broadening of the market rally, moving beyond the dominance of "mega-cap leadership."

The primary catalyst for the market movement was Jerome Powell's speech at the Jackson Hole symposium. The Federal Reserve Chairman indicated that the central bank is contemplating a potential rate cut as early as September, bolstering segments most sensitive to interest rate fluctuations. In response, the Russell 2000 surged 3.85% on the day of the speech. Further supporting the case for policy easing in September was a batch of new labor market data: unemployment rose to 4.32% in August, while hiring trends remained weak. Nonetheless, market participants interpreted these signals as indicative of a soft landing rather than an impending recession, continuing to actively purchase dips in riskier assets.

Robust fundamental conditions are emerging to support a continuation of the rally. These are anchored not only by the heightened anticipation of 2-3 interest rate cuts by the end of 2025 but also by a shift in profit recovery forecasts within the small-cap equity sector. Following a vigorous 19% y/y increase in EPS at the close of Q2, the market is projecting a growth acceleration: 30.1% y/y growth through 2025, with an anticipated further increase to 40.2% y/y in 2026.

The spotlight now turns to the upcoming Federal Reserve meeting scheduled for the next two weeks. Rate futures have fully priced in a rate cut, with the likelihood pegged at 100%. The main point of uncertainty lies in the magnitude of the cut. Following the labor market data release, the probability of a standard 25 basis point (bp) cut declined to 88.2%, while the likelihood of a more substantial 50 bp cut — the so-called "jumbo cut" scenario — has gained traction, increasing to 11.8%.

Technical Analysis of the Broad Market

The technical outlook for the broad market index remains favorable overall, with no significant reversal patterns or overbought conditions apparent. From a market breadth perspective, there is a continued upward momentum, as evidenced by the proportion of companies with an RSI above 70, along with those trading above their 50-day moving average, suggesting no signs of market overheating. Nevertheless, it is worth noting that the prices are currently moving within a narrow ascending channel and are approaching its upper boundary. Consequently, a potential minor pullback to the 6,460-6,475 point range may be anticipated.

Expected Trading Range

We expect the S&P 500 Index to move in the range between 6,400-6,600 points.