Investment Review №330. Profit favors the bold

Vadim Merkulov

Head of Analytics department

ConocoPhillips. An oil and gas classic

The medium-term growth potential in COP shares is around 20%.

About Company

ConocoPhillips (COP) engages in the exploration, production, transportation, and marketing of oil and natural gas, with a primary focus on its North American operations. The United States contributes approximately 80% of the company's revenue, while Canadian operations account for an additional 6%. Established in 1875, ConocoPhillips maintains its headquarters in Houston, Texas.

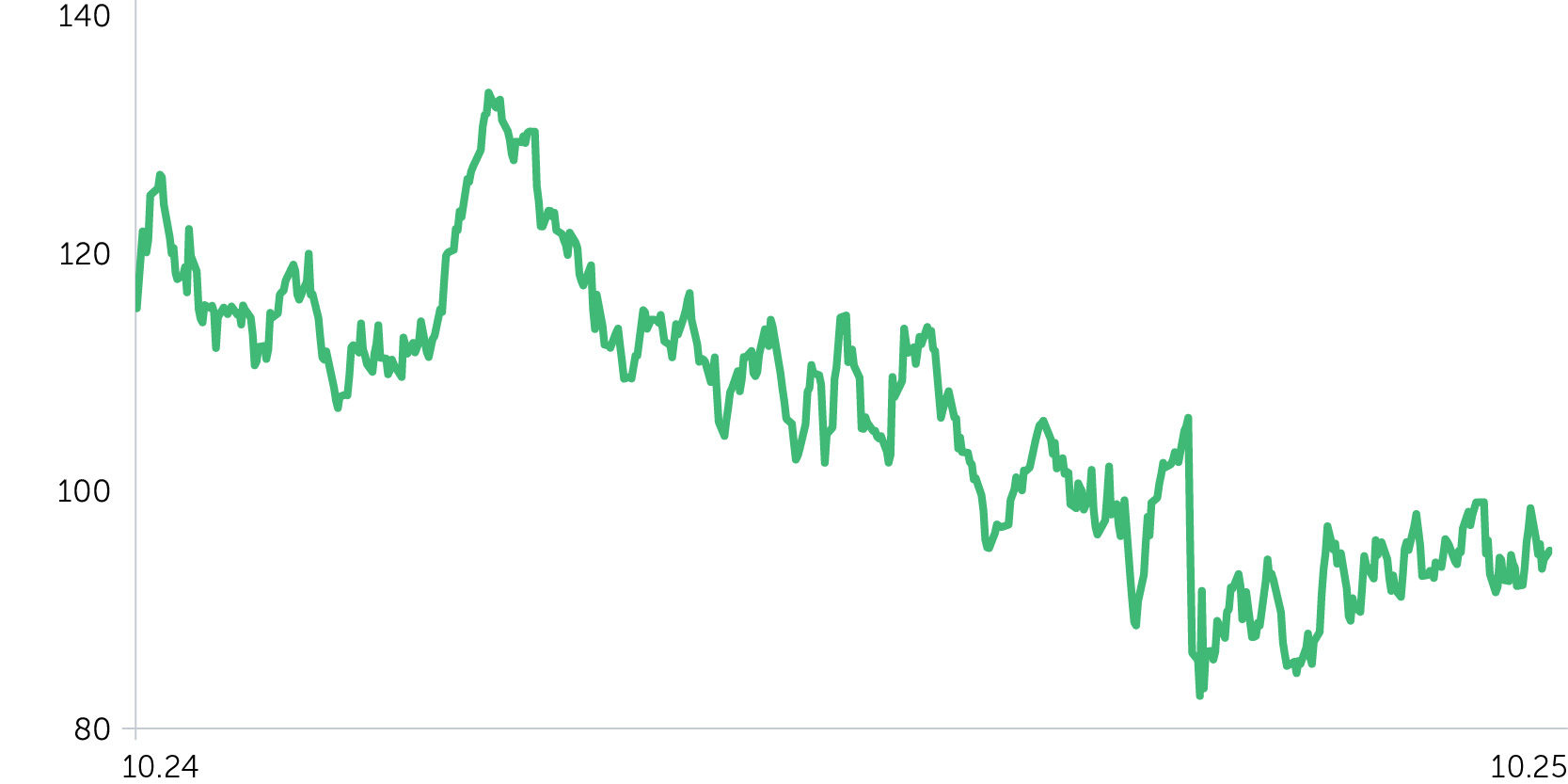

Following the announcement of import duties by the Trump administration, the resulting decline in oil and natural gas prices has weighed on the company’s shares this year. Since the start of 2025, ConocoPhillips (COP) shares have declined by 4.3% (as of the market close on October 6). However, we believe that the company securities possess significant upside potential for several reasons.

| Ticker | COP |

| Share price as of analysis | $94,91 |

| Target share price | $114 |

| Growth potential | 20,1% |

| Stock vs Indices | Day | Week | Month | Quarter | Year |

| COP | 0,8% | (1,0%) | 2,1% | 1,3% | (17,1%) |

| S&P 500 | 0,4% | 1,2% | 4,0% | 7,3% | 17,2% |

| Russell 2000 | 0,4% | 2,1% | 4,0% | 10,6% | 12,4% |

| DJ Industrial Average | (0,1%) | 0,8% | 2,9% | 4,2% | 10,3% |

| NASDAQ Composite Index | 0,7% | 1,6% | 5,7% | 11,4% | 26,5% |

Price dynamics COP, $

Investment Thesis

- Increased demand and upward pricing pressure on natural gas during the heating season. Robust growth in gas production, combined with weaker-than-expected summer demand, triggered a notable price decline, with values falling 25.2% from this year’s peak.

Looking ahead, we anticipate a rebound in natural gas prices in the latter half of the fall, driven by the onset of the heating season. According to the U.S. Department of Energy (DOE), November's U.S. gas consumption is projected to rise by 16% m/m, with a further increase of 16.6% m/m in December. This translates to an estimated consumption of 92.6 billion cubic feet per day (Bcf/d) in November, escalating to 108 Bcf/d in December.

Additionally, domestic natural gas prices are poised to experience further support from expanding liquefied natural gas (LNG) production and export capabilities. The DOE forecasts LNG exports will increase by 23.6% year-over-year in 2025 and by 10.2% in 2026, reaching 14.7 Bcf/d and 16.3 Bcf/d, respectively. - High dividend yield and large-scale share repurchases. On November 22, 2024, ConocoPhillips finalized the acquisition of Marathon Oil (MRO), a major U.S. oil and gas producer, in a transaction characterized by its non-monetary nature, as payment was executed in COP shares. The acquisition was valued at approximately $16 billion, excluding assumed debt. To mitigate the dilution effect from issuing additional shares, ConocoPhillips plans to undertake a significant share buyback program amounting to $20 billion within three years post-closing. In 2025, COP has earmarked a $10 billion capital return to shareholders, designating $6 billion specifically for share buybacks, a notable increase from $5.4 billion in 2024. As a result, COP shares outstanding saw a reduction of 1.25% in Q2 2025.

For Q2 2025, management has maintained the quarterly dividend at $0.78 per share, resulting in an annualized dividend yield of 3.3%.

We project a 20% upside potential for COP shares over the medium term. Our 12-month price target is set at $114, with a "Buy" recommendation. It is advisable to establish a stop-loss at $83.40.

| Marginality % | 2022A | 2023A | 2024A | 2025E | 2026E | 2027E | 2028E | 2029E |

| Gross margin | 45% | 45% | 45% | 44% | 45% | 45% | 45% | 45% |

| EBITDA Non-GAAP (non-adj) margin | 43% | 43% | 43% | 41% | 43% | 42% | 42% | 42% |

| Net Income margin | 21% | 18% | 16% | 14% | 16% | 16% | 16% | 17% |

| Ratio Analysis | 2022A | 2023A | 2024A | 2025E | 2026E | 2027E | 2028E | 2029E |

| ROE | 36% | 22% | 14% | 13% | 14% | 14% | 13% | 13% |

| ROA | 18% | 11% | 8% | 7% | 8% | 8% | 8% | 8% |

| ROCE | 35% | 20% | 13% | 11% | 12% | 12% | 12% | 12% |

| Sales/Assets | 0,9x | 0,6x | 0,5x | 0,5x | 0,5x | 0,5x | 0,5x | 0,5x |

| Interest Coverage | 35x | 22x | 19x | 15x | 17x | 19x | 20x | 23x |

| Financial performance, $ mn | 2022A | 2023A | 2024A | 2025E | 2026E | 2027E | 2028E | 2029E |

| Revenue | 82 156 | 58 574 | 56 953 | 61 401 | 62 697 | 65 593 | 66 905 | 68 243 |

| COGS | 44 905 | 32 140 | 31 205 | 34 691 | 34 352 | 35 939 | 36 569 | 37 300 |

| Gross Income (adj.) | 37 251 | 26 434 | 25 748 | 26 710 | 28 345 | 29 654 | 30 336 | 30 943 |

| SG&A | 623 | 705 | 1 158 | 776 | 786 | 801 | 818 | 834 |

| Operating income (adj.) | 35 698 | 25 407 | 24 408 | 25 011 | 26 665 | 27 444 | 28 060 | 28 689 |

| A&D | 7 504 | 8 270 | 9 599 | 11 822 | 11 881 | 11 948 | 12 021 | 12 142 |

| Interest expense (income) | 805 | 780 | 783 | 884 | 864 | 818 | 783 | 726 |

| Pretax Income (adj.) | 27 389 | 16 357 | 14 026 | 12 305 | 13 919 | 14 678 | 15 256 | 15 822 |

| Income Taxes | 9 548 | 5 331 | 4 427 | 3 445 | 3 897 | 4 110 | 4 272 | 4 430 |

| Net Income (adj.) | 17 340 | 10 615 | 9 224 | 8 859 | 10 022 | 10 568 | 10 984 | 11 392 |

| Dilluted EPS | $13,52 | $8,77 | $7,79 | $6,91 | $8,13 | $8,92 | $9,55 | $10,20 |

| DPS | $4,99 | $3,91 | $3,12 | $3,12 | $3,16 | $3,24 | $3,30 | $3,40 |