Investment Review №332. The Bulls switched to big tech

Not everything is so clear-cut

By early November, local companies' stock prices had moved in opposite directions

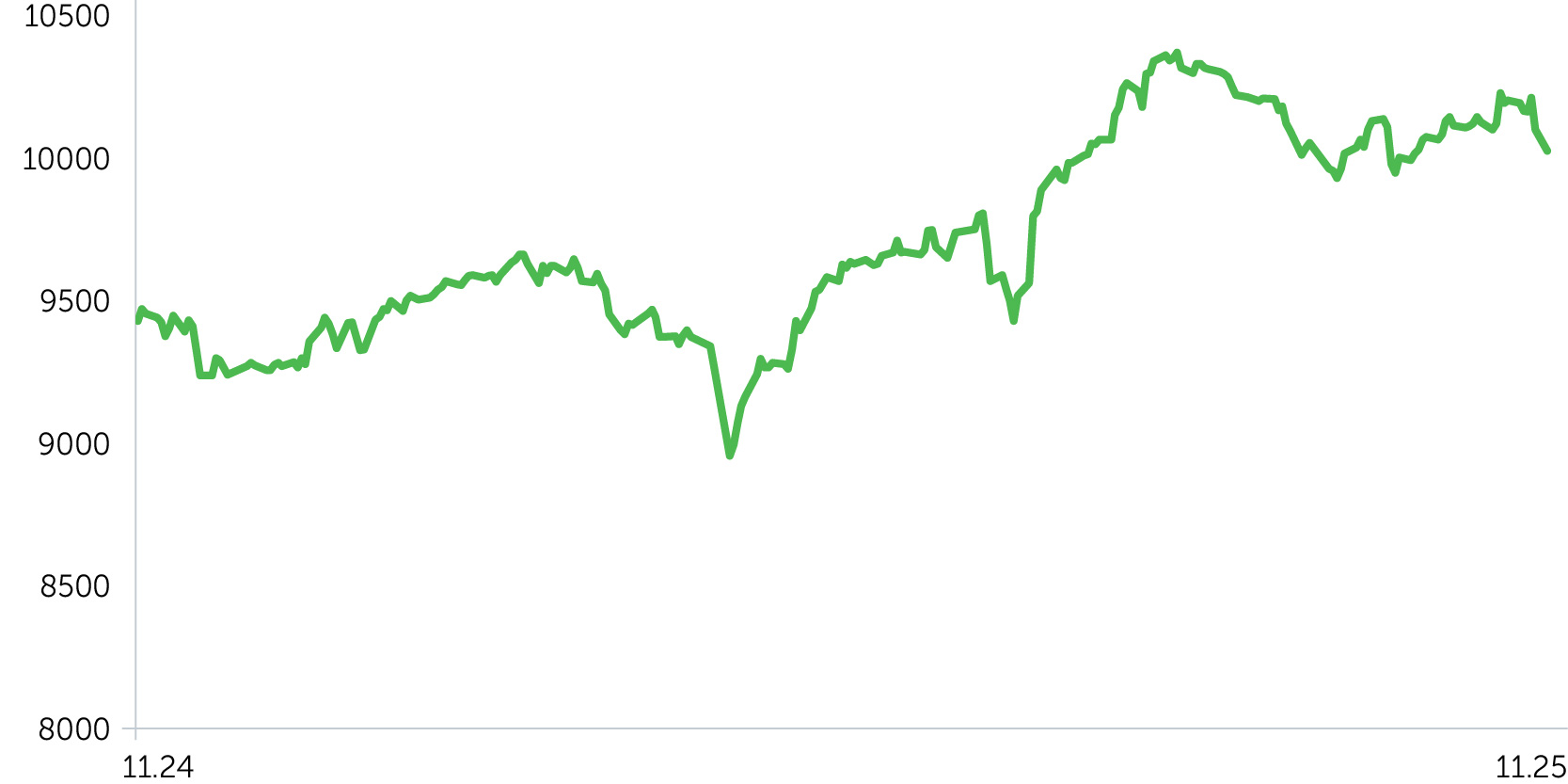

DFM General Index: 1-Year Dynamics

Abu Dhabi Securities Exchange Index: 1-Year Dynamics

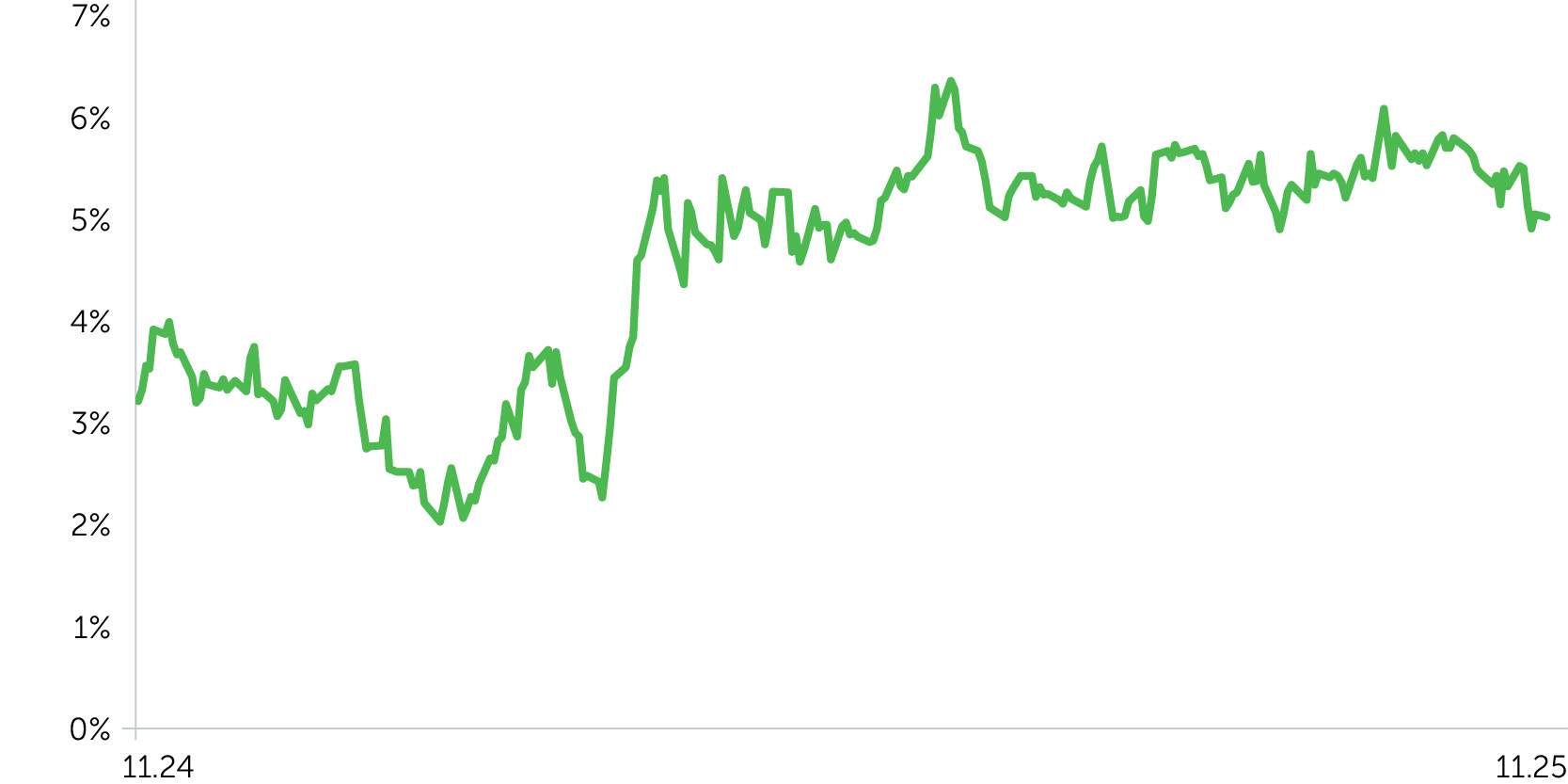

Yield, Forward Rate 1m10y, UAE, 1-Year Dynamics

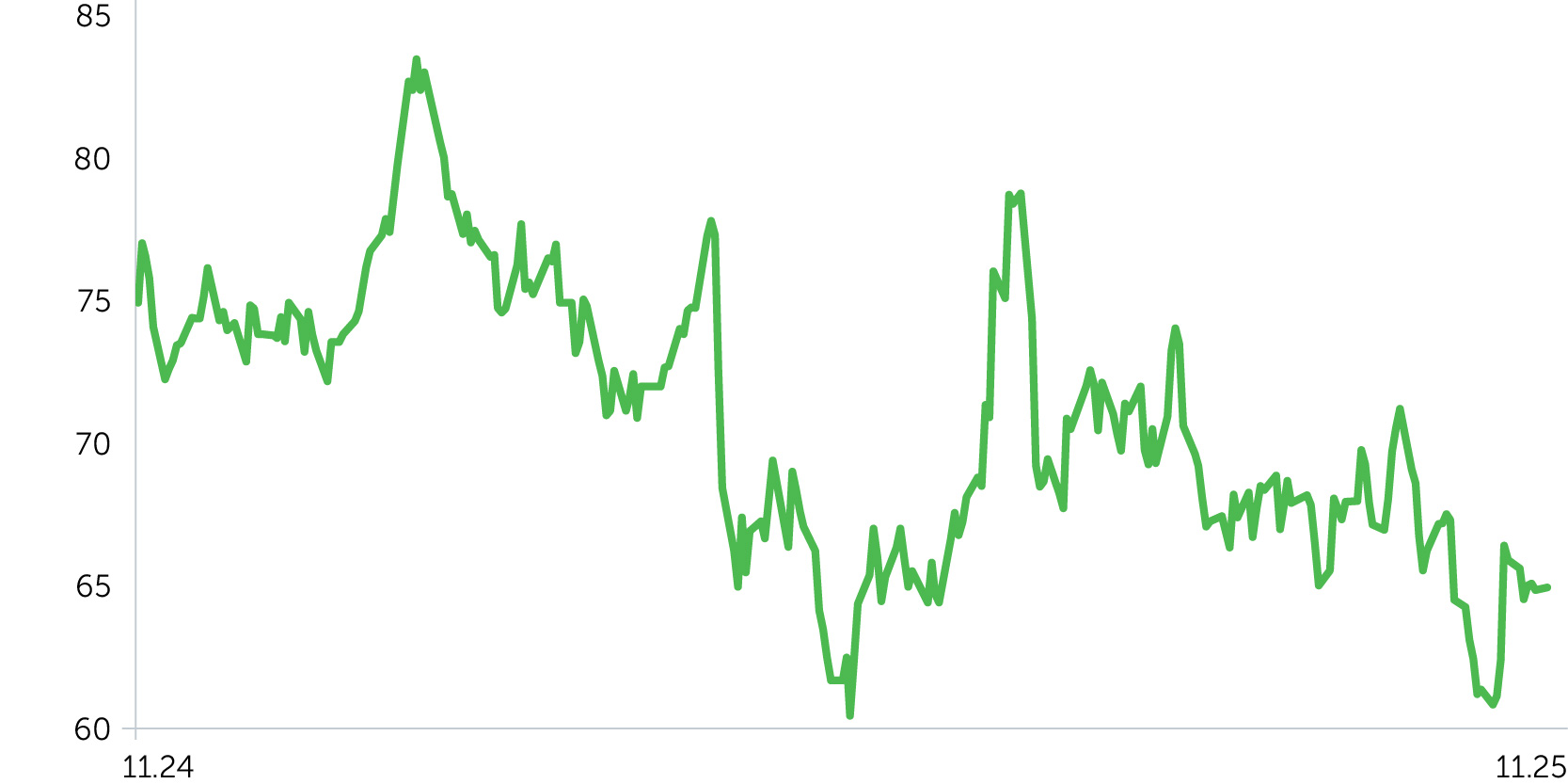

Brent Oil, 1-Year Dynamics

Between October 21 and November 3, 2025, UAE equity markets showed mixed performance. The Dubai Financial Market (DFM) Index rose by 1.1%, while the Abu Dhabi Securities Exchange (ADX) declined by 0.7%. Brent crude prices climbed 6.8% during the period, driven by attacks on Russian refineries and escalating tensions between the United States and Venezuela. The sharp rise in oil prices provided some support, but it was not enough to lift the ADI, which remained under pressure due to weakness in key constituents such as TAQA, ADNOCGAS, and EAND. By comparison, the S&P 500 trended higher over the same period, gaining 1.7%.

Sector performance was mixed. The Financials sector rose by an average of 1.1%, while Utilities declined by approximately 1.11%. Among large-cap names, Emirates NBD Bank (ENBD) advanced 8.6% following strong financial results. At the same time, Aldar Properties (ALDAR) shares lost 8.3% amid concerns over a potential exit of Alpha Dhabi Holding from the company’s shareholder base.

UAE Treasury yields declined by 33 basis points, while U.S. Treasury yields rose by 13 basis points. The current spread versus a comparable U.S. Treasury issue stands at 73 basis points, notably above the five-year median of 48 basis points. Improved economic forecasts for the UAE and expectations of softer monetary policy are bolstering the reassessment of credit risks in the region toward a narrowing of the spread to historical levels (over the past two weeks, the differential stood at 78 basis points).

Economic Updates

- Dubai’s real estate market remained resilient in October, with residential and commercial transactions totaling AED 46.26 billion. Off-plan sales accounted for 71.4% of overall activity, reflecting strong buyer confidence. Cumulative sales value for the first ten months of 2025 reached AED 559 billion, surpassing the full-year record set in 2024.

- Dubai approved a series of strategic initiatives aimed at enhancing quality of life and reinforcing its position as a global hub. Key measures include a Sports Sector Development Plan through 2033, a policy to expand the network of affordable schools, and the establishment of a specialized court for financial restructuring and bankruptcy cases to boost investment appeal.

Corporate News

- PureHealth Holding (PUREHEALTH: −0.72%), the region’s largest healthcare group, reported strong results for the first nine months of 2025 on November 3. Revenue rose 6% year-over-year to AED 20.1 billion, while net profit increased 8% to AED 1.55 billion. Growth was driven by a higher number of patients and expanded clinical capacity in both the UAE and the United Kingdom.

- On October 31, Dubai Holding and U.S. technology firm Palantir Technologies (PLTR) announced the launch of a joint venture, Aither, aimed at deploying AI solutions across Dubai’s public and private sectors. This marks Palantir’s first such initiative in the UAE and is expected to support the objectives of Dubai’s D33 Economic Agenda.

Two-Week Outlook

The OPEC+ decision to suspend further increases in oil production quotas in the first quarter of 2026 is expected to support oil prices, which in turn could have a positive impact on energy sector equities. Weekly U.S. data showing a 6.9 million-barrel decline in commercial crude inventories and a drop in drilling activity suggest a potential tightening of supply in the market, which could stimulate an increase in WTI prices. Lingering risks of a global economic slowdown continue to act as a headwind for the market. However, solid earnings in the financial sector and robust real estate activity are supporting interest in local assets. The market remains relatively illiquid compared to developed exchanges, but in the absence of escalating geopolitical tensions, foreign capital inflows could continue to drive its outperformance relative to the S&P 500.

From a technical standpoint, the outlook remains rather negative: prices have fallen well below the 50-day moving average and have not yet reached the support zone around 9,957 points. Meanwhile, the RSI remains in neutral territory, which together suggests a continued downside risk.