Investment Review №337. A shift toward hedging

LONG CALL ON VISA

Idea summary

Visa is the world’s крупнейшая global payment network, generating revenue from transaction processing and services for banks and merchants. The idea is a tactical bet on Visa shares rising over a ~8-week horizon via buying a Call option: downside risk is limited to the premium paid, while upside grows as the underlying accelerates higher. Support for the scenario comes from steady demand for cashless payments and Visa’s “quality” profile (strong cash flows and high margins).

Key arguments

- Visa monetizes the growth in cashless transactions without being tied to the success of any single retailer or bank.

- Cross-border payments improve the revenue mix and support profitability.

- Growth in service revenues (fraud prevention, analytics, risk solutions) increases business resilience.

- In the near term, sentiment around “quality” names and expectations for financial results may act as a catalyst.

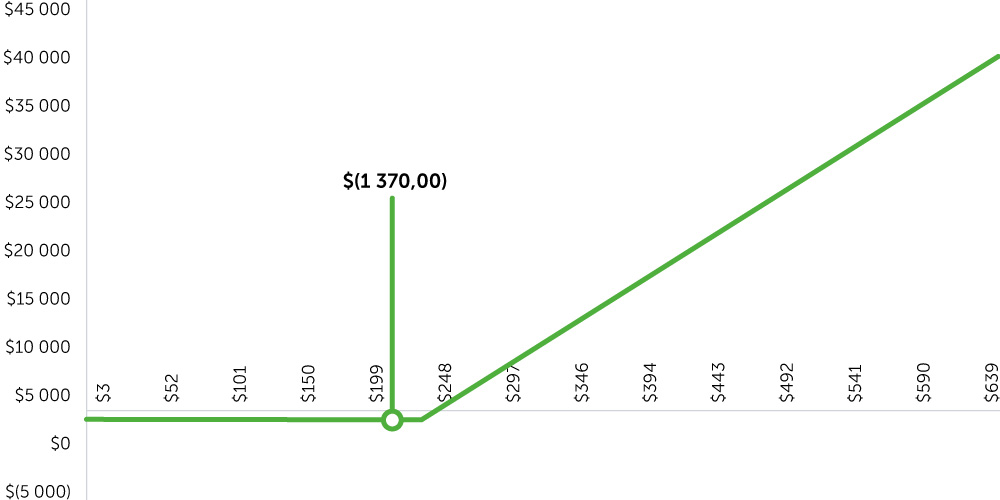

Risk management

If on the expiration date (20.03.26) the underlying price is above $235 but below $248.70, the investor will incur a loss that will vary depending on the settlement price. If the underlying price is below $235, the investor will realize the maximum loss of $1,370. If the underlying price is above the breakeven level ($248.70), the potential profit is unlimited; however, we recommend closing the position once the call option premium reaches $2,050.

Trade parameters

| Buy | Long Call on V |

| Strike | Long CALL 235 |

| Option | +V*G3K235 |

| Expiration date | March 20, 2026 |

| Margin requirement | $1,370 |

| Exit price (premium target) | $2,050 |

| Maximum profit | ∞ |

| Maximum loss | ($1,370.0) |

| Expected return | 50% |

| Breakeven | $248.70 |

P/L of the option strategy