Investment Review №340. The Bombshell Effect

Corporate News In Focus of Our Analysts

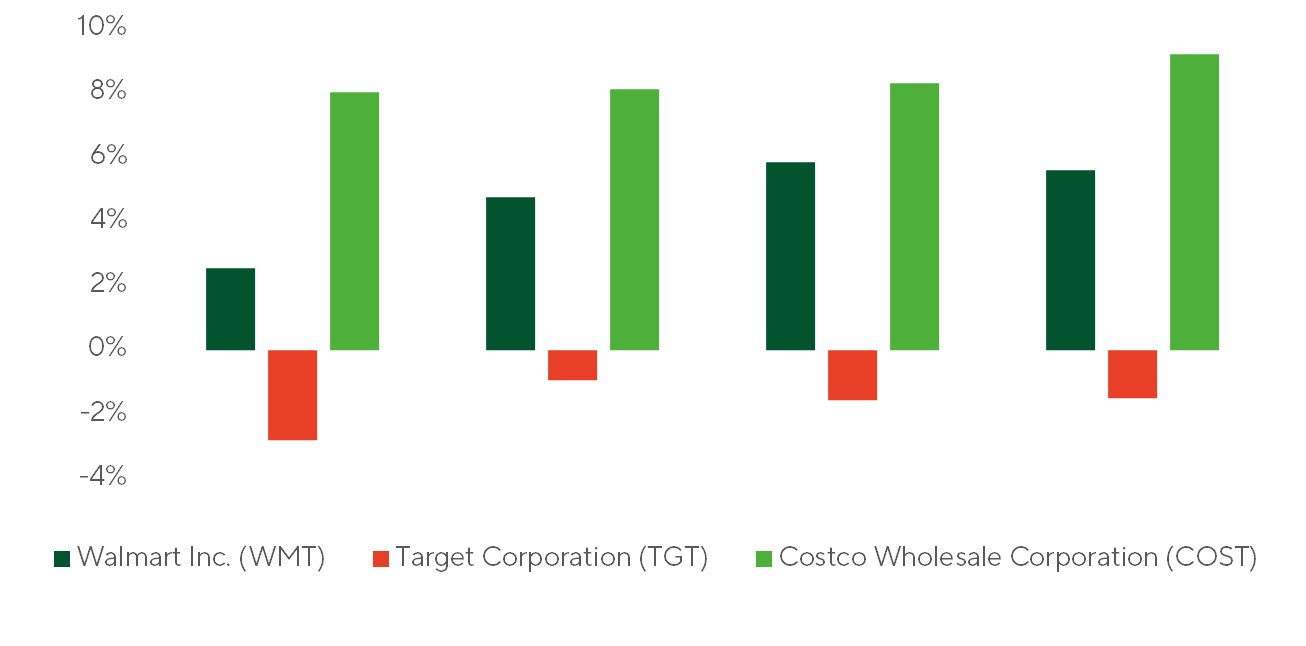

Costco

Costco (COST) remains the fastest growing among major U.S. retailers by revenue. Q2 revenue rose 9.1% YoY to $68.24bn (8.7% YoY on a comparable basis). Comparable sales increased 5.9% in the U.S., 10.1% in Canada, and 13.0% in other international markets. Operating income grew 12% YoY to $2.6bn, a margin of 3.8%. EPS of $4.58 topped consensus. Market reaction has been neutral. The shares trade at P/E above 50, materially higher than for Amazon (AMZN) and Walmart (WMT).

Revenue over the Past Four Quarters

Source: FactSet

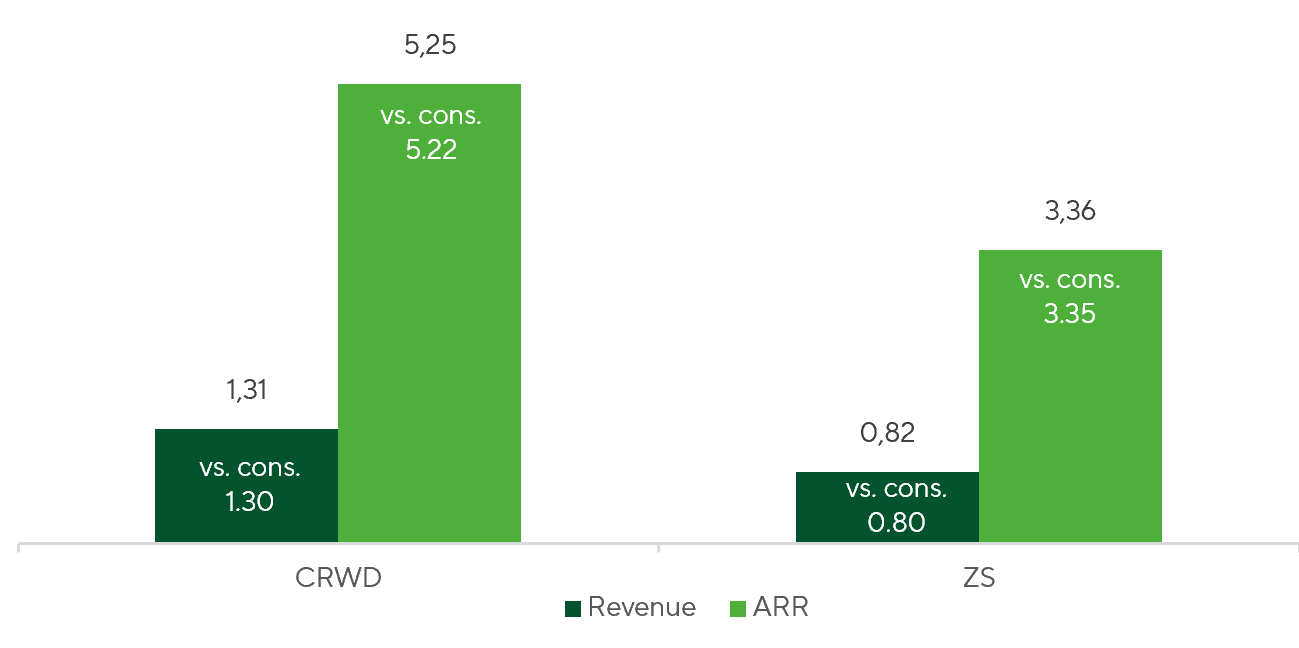

Zscaler, CrowdStrike

The cybersecurity investment thesis remains compelling following strong quarterly results from industry leaders CrowdStrike (CRWD) and Zscaler (ZS). Both companies delivered consensus beats that highlight the scalability and durability of their business models. Structural growth in the sector continues to be driven by increasingly sophisticated cyber threats and the global shift toward Zero Trust architectures.

In this environment, enterprises are rationalizing IT budgets and favoring integrated platforms over disparate solutions. While investors are concerned about potential disruption from autonomous AI agents, we view the trend as a net tailwind for CrowdStrike and Zscaler. With AI-enabled attacks becoming more frequent, customers are inclined to seek equally advanced, algorithmic defenses and accelerate adoption of their platforms. The companies’ sustained leadership in AI-centric cybersecurity underpins a long-term investment appeal of the sector.

Comparison of quarterly revenue ($bn) and annual recurring revenue (ARR) ($bn) versus market consensus

Source: FactSet

Dell Technologies

Dell Technologies (DELL) delivered a strong quarterly print on February 26, with earnings and revenue both exceeding market expectations, while the infrastructure and client segments posted faster-than-anticipated growth. Guidance for Q1 and FY 2026 was also well ahead of consensus, and management pointed to accelerating AI server revenue growth alongside margin improvement in traditional servers, data storage systems, and PCs. The market reacted sharply; shares jumped nearly 22% the following day. Despite the general optimism, the path to meaningfully higher profitability remains constrained, in part by industrywide component shortages. A week later, at a Morgan Stanley conference, the company highlighted a record $43bn backlog and said it expects its AI server business to roughly double on the back of exceptional demand.

Dynamics of Dell's financials

Sources: FactSet, Dell, Freedom Broker

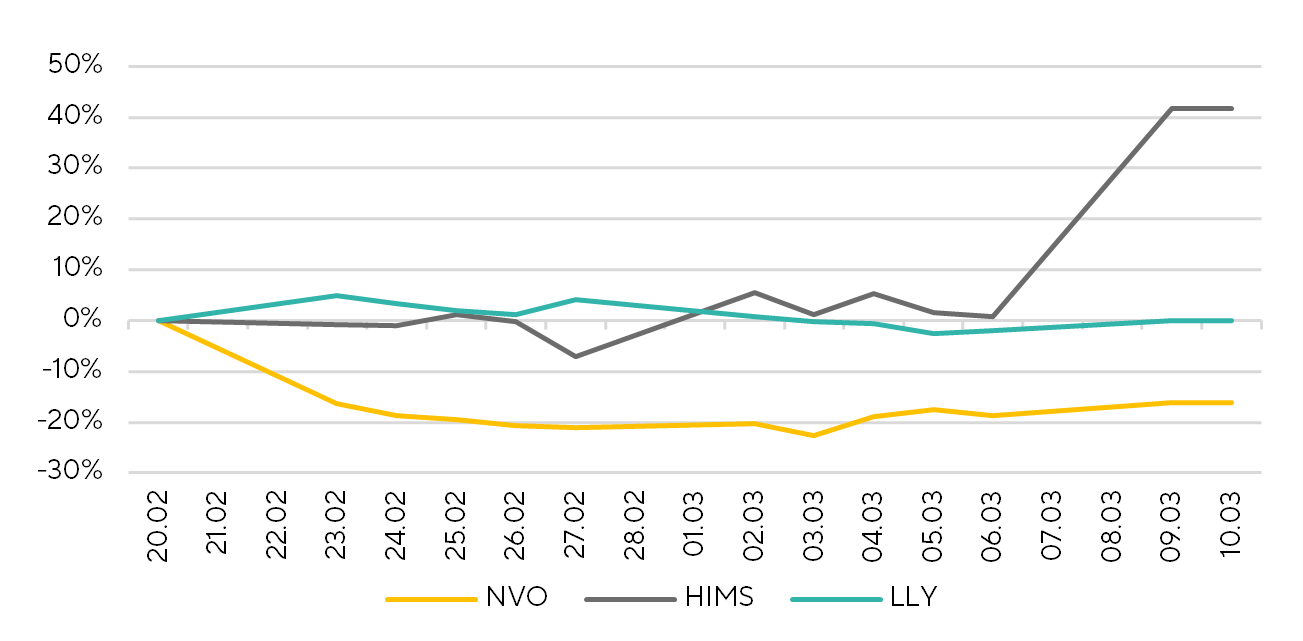

Eli Lilly, Novo Nordisk

Eli Lilly’s oral GLP-1 receptor agonist, orforglipron, delivered greater reductions in glycated haemoglobin and body weight than Novo Nordisk’s Rybelsus (oral semaglutide) in a Phase 3 study. The results reinforce Lilly’s leadership in the weight-loss market, extending it into the oral GLP-1 segment.

Meanwhile, On March 9, Hims & Hers Health announced an agreement with Novo Nordisk—a surprising turn given their prior litigation related to Hims’ plans to market an oral Wegovy copy on its platform. Under the newly reached agreement, Hims will distribute Novo Nordisk’s oral GLP-1 via its platform, whereas Novo Nordisk will dismiss its legal claims.

We view the deal as mutually beneficial. For HIMS, it mitigates a key regulatory risk. For Novo Nordisk (NVO), it adds a new distribution channel amid intensifying competition from Eli Lilly (LLY).

Stock price chart for HIMS, NVO, and LLY from Feb. 20 to Mar. 10

Source: FactSet

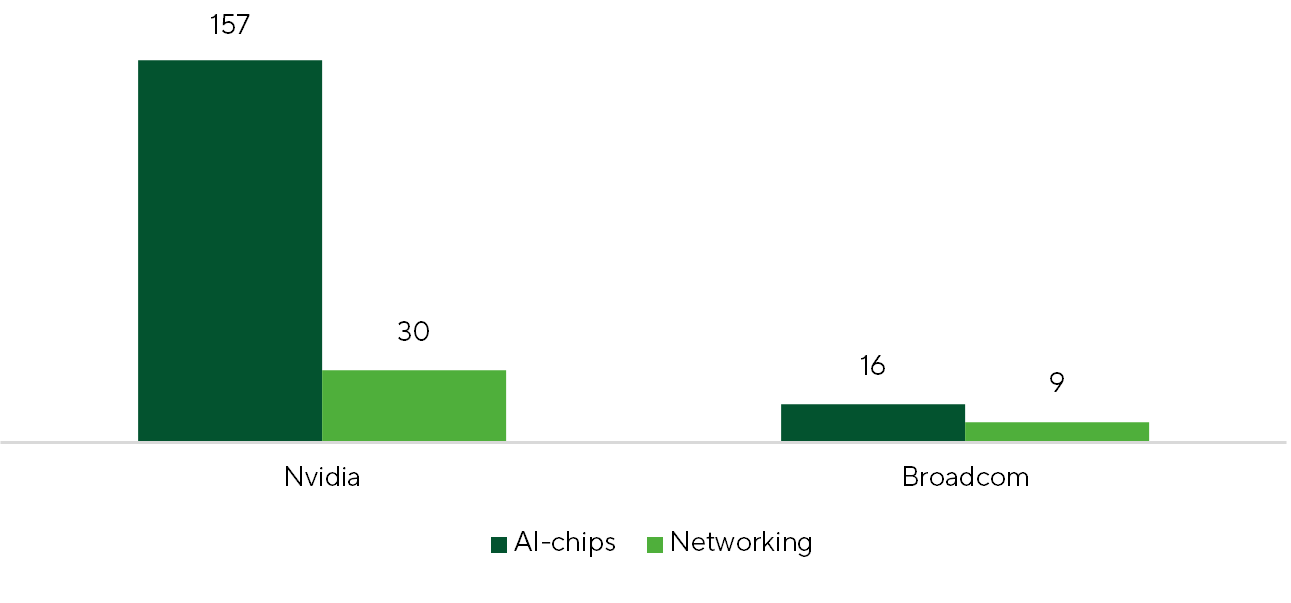

NVIDIA, Broadcom

In recent weeks, NVIDIA (NVDA) and Broadcom (AVGO) — two key suppliers of semiconductors and networking equipment for AI data centers—reported quarterly results. Both delivered strong prints alongside upbeat outlooks. Investors had braced for gross-margin pressure at both companies, but management comments largely allayed those concerns. At NVIDIA, the balance sheet signals readiness for the next leg of growth despite tightening supply of memory and other components. Inventory and supply commitments now approach $120bn, supporting the company’s ability to sustain elevated gross margins.

While the companies compete across AI data center silicon and networking, the simultaneous share-price strength and constructive sentiment for both underscore the scale of today’s infrastructure build-out. Technically, Broadcom remains the leader in networking hardware, but NVIDIA is already well ahead in terms of business scale. Attention now turns to NVIDIA’s GTC 2026 conference, which begins on March 16 and could serve as an additional catalyst for NVDA shares.

Data Center Revenue for CY2025, $ bn

Sources: Nvidia, Broadcom, FactSet, Freedom Broker