Investment Review №341. The Obvious and the Unbelievable

Macroeconomics in Focus

Economic data continues to drive trends in local stock markets

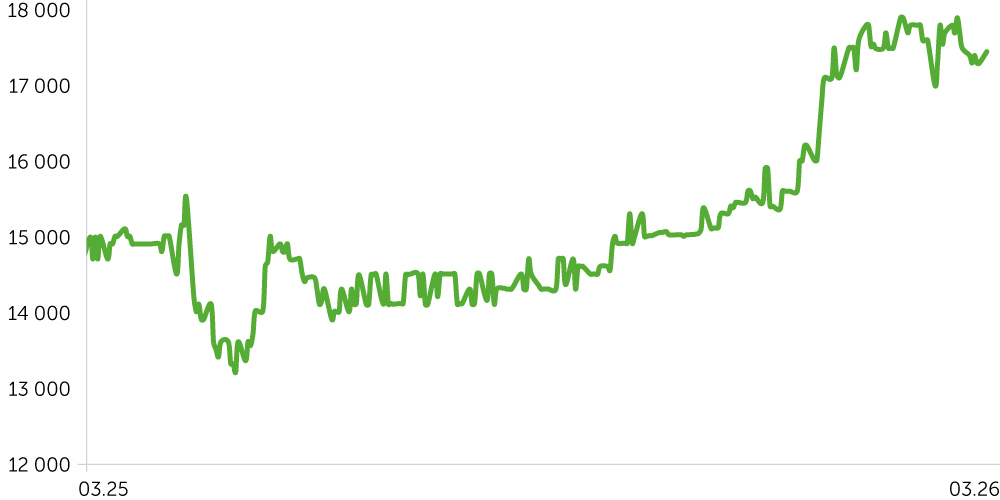

Telecom Armenia: 1-Year Stock Trends

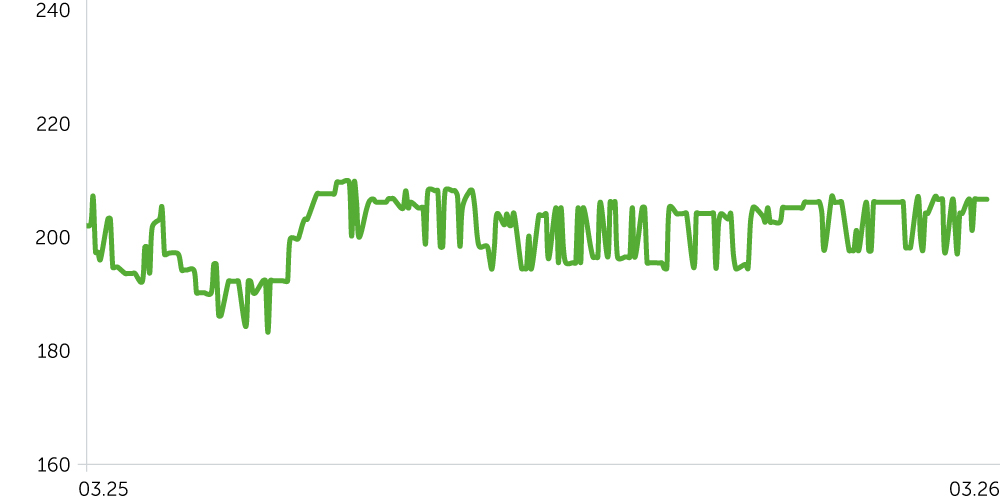

ACBA Bank: 1-Year Stock Trends

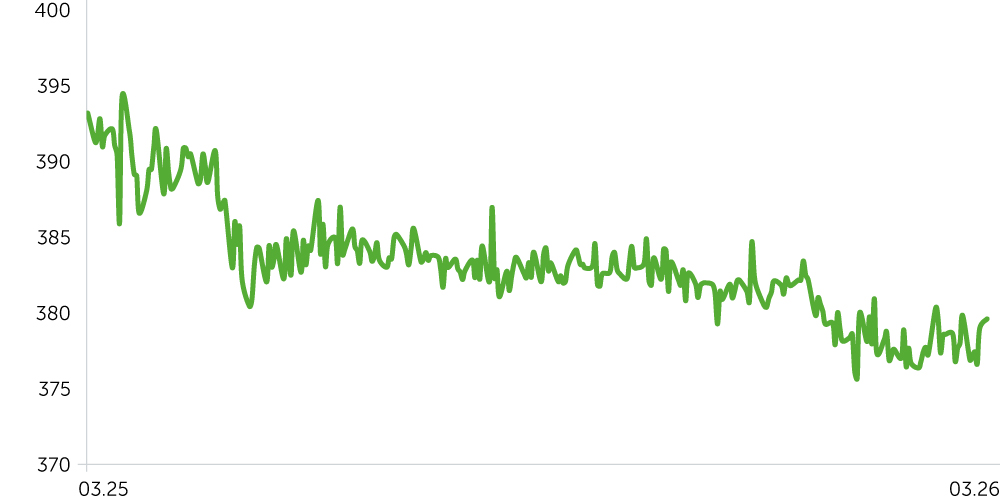

USD/AMD: 1-Year Dynamics

3-Year Corporate Bond Index (AMD) – Post-Update

Between March 9–23, 2026, Armenia’s equity market traded mixed amid a relative lull in domestic data flow. Telecom Armenia (AMTL) advanced a further 2.2% despite a lack of catalysts in sector prints. January revenue across telecoms and broadcasting rose 2.8% YoY, with the core telecom segment (~93% of sector revenue) up 3.0% YoY. By contrast, Acba Bank (ACBA) retraced 2.0%. That said, the stock remains a clear outperformer YTD (+11.9%), and the pullback reads more like profit-taking after a strong run than any deterioration in fundamentals or sector view.

The AMD-denominated 3Y corporate bond price index was broadly flat over the period, underscoring a wait-and-see stance as rate-path uncertainty stabilizes. January industrial output surprised to the upside, expanding 10.6% YoY, led by mining (+25.2%), utilities—electricity, gas & steam (+17.0%)—and accelerating momentum across chemicals, electronics and pharma. On policy, the Central Bank of Armenia held the refinancing rate at 6.5% on March 17 for a third consecutive meeting. The regulator flagged a potential additional pro-inflationary impulse of ~1.2–1.7% p.a. tied to escalation risks around Iran. Macro risks are tilting more clearly pro-inflationary amid Middle East tensions, with higher global energy prices and renewed supply-chain frictions likely to constrain scope for further easing. In a downside scenario of continued escalation, we see rising odds of a hawkish pivot and a near-term rate hike.

The dram edged down 0.3% against the dollar yet continued to trade at historically strong levels.

Economic Updates

- Armenia’s industrial output in January 2026 rose 10.6% YoY (-56.7% MoM). Manufacturing, the largest contributor at 56.5% of total, expanded 4.3% YoY, while mining (+25.2% YoY) and utilities—electricity, gas & steam (+17.0%)—posted stronger growth. Within manufacturing, performance remained uneven: major segments—food, basic metals, and tobacco—showed muted growth, whereas chemicals, electrical equipment, electronics, and pharma outpaced the broader sector, signaling gradual diversification of the industrial base.

- The Central Bank of Armenia kept the refinancing rate at 6.5% in March for a third consecutive meeting, a move largely priced in and reflecting the regulator’s conservative stance. The pause provides space to assess whether the recent inflation spike >4% is a transitory shock—driven in part by supply-side pressures—or a more persistent trend. For the local fixed-income market, the cautious monetary path supports greater predictability. That said, we see upside risk to inflation expectations if instability in the Middle East persists, which could weigh on real yields and, in turn, bond prices. The regulator estimates that escalation around Iran could add ~1.2–1.7% to annual inflation.

- Armenia’s telecoms & broadcasting sector revenue rose +2.8% YoY in January (vs +2.7% YoY in FY25) but fell -12.3% MoM. Despite the sharp MoM slowdown, YoY growth remains positive, driven by the core telecom segment (+3.0% YoY), which accounts for ~93% of sector revenue.

Corporate News

- Electric Networks of Armenia prepaid a ~$9m loan to a local bank ahead of schedule without tapping new financing. According to the interim manager, total liabilities since the start of administrative proceedings have declined ~12%, with repayments exceeding $47m funded from internal cash. The move points to reduced leverage and modest improvement in the company’s financial position.

Two-Week Outlook

- Between March 27–April 6, a meaningful macro data slate for Armenia is scheduled. February external trade releases should clarify FX flows and the net export contribution to GDP, with the forecast pointing to a modest widening of the trade deficit. February retail sales will shed light on domestic demand trends.

Market focus will center on February economic activity, with expectations for a rise from 7.6% in January to 8.3% YoY. Another key release is March CPI, where growth is forecast to ease from 4.3% in February to ~3.7% YoY. March’s geopolitical shocks are likely to have a muted effect on the monthly figures, so market reaction is expected to be minimal.