Investment Review №344. A Commitment to Techno-Optimism

Inflation Remains Sticky Despite Cooling Activity

Macroeconomic Data Led to a Neutral-to-Negative Trend in Local Markets

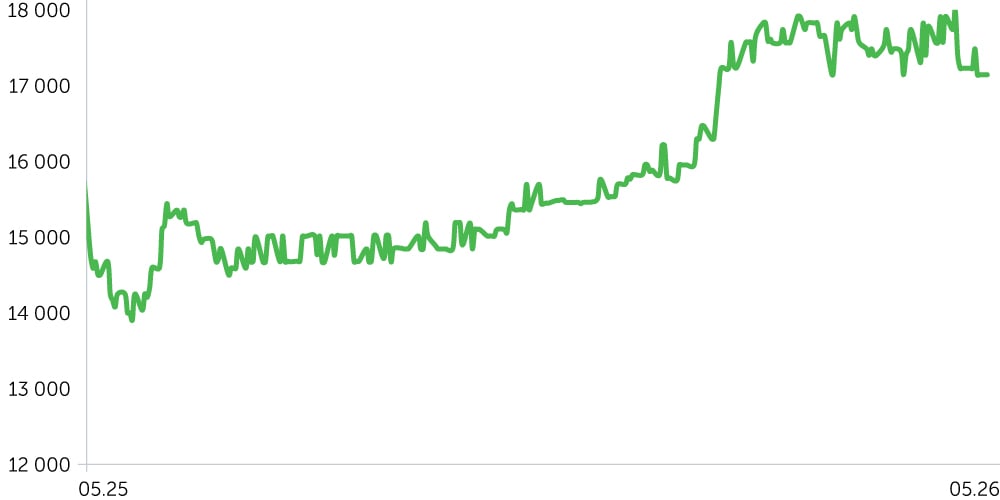

Telecom Armenia Stock Performance (Post-IPO)

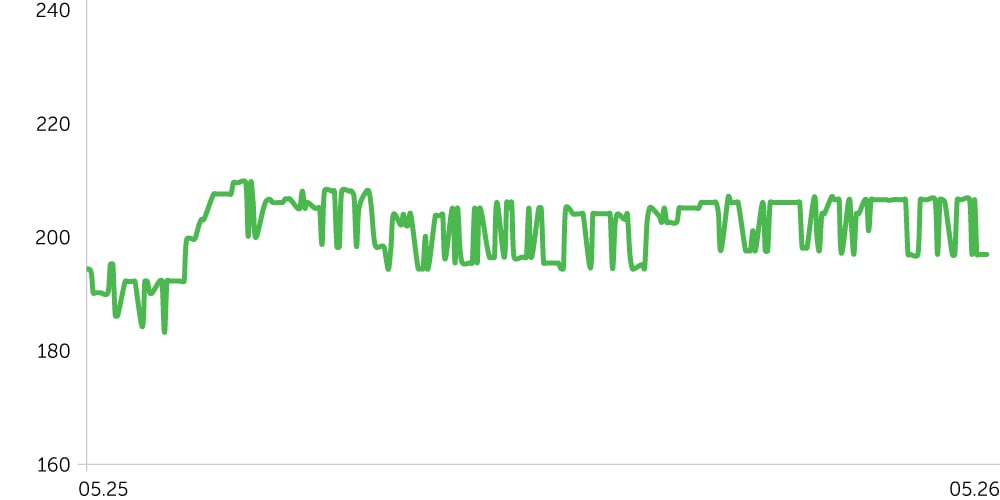

ACBA Bank: 1-Year Stock Trends

USD/AMD: 1-Year Dynamics

3-Year Corporate Bond Index (AMD) – Post-Update

From April 20 to May 4, 2026, the Armenian equity market saw a partial pullback amid signs of cooling economic activity. ACBA Bank declined 4.0%, trimming its YTD gain to 9.7%, while Telecom Armenia (AMTL) was unchanged. Pressure on financials likely reflects a slowdown in March GDP growth to 6.6% YoY (vs. 7.2% YoY in February), the weakest pace since April 2025. The main drag was a sharp moderation in industrial growth to 7.0% YoY from 23.8% YoY a month earlier, alongside stagnant domestic trade (+0.2% YoY). By contrast, construction retained robust momentum (+24.0% YoY), pointing to still-elevated real estate investment demand that, in our view, continues to divert capital from the country’s financial markets.

The AMD 3-year Corporate Bond Index did not change, consistent with a steady Central Bank of Armenia (CBA) policy rate and a balance between real-economy slowing and persistent inflation pressures. Producer price growth maintained at 9.5% YoY, the highest rate since May 2022; coupled with ongoing external geopolitical risks, this increases the likelihood of further cost pass-through to consumers. In this context, the risk of additional monetary tightening by the CBA remains elevated. The dram strengthened a further 0.5% against the U.S. dollar over the period. Overall, the latest macro data suggests the economy is shifting to a more moderate growth path while inflation risks persist—an environment that could foster bouts of volatility, including in the FX market, if sustained.

Economic Updates

Only a handful of macro releases came out between April 20 and May 4, 2026: the Central Bank’s decision to keep policy on hold and data pointing to a cooling in economic activity amid slowing industrial output.

- Armenia’s economic activity grew 6.6% YoY in March 2026, decelerating broadly in line with expectations from 7.2% in February and marking the slowest pace since April 2025. The cooling was driven mainly by a sharp slowdown in industry (7.0% YoY vs. 23.8% YoY in February), despite an acceleration to 11.6% MoM versus 4.6% MoM in February, and by near-stagnant trade turnover (0.2% YoY vs. 5.6% YoY in February). By contrast, construction maintained strong momentum, accelerating to 24.0% YoY, while services expanded 7.8% YoY. The marked slowdown in industry and trade may reflect one-off factors; however, if persists, it could weigh on market sentiment and on economic growth expectations.

- Producer prices rose 9.5% YoY in March 2026, maintaining the fastest pace since May 2022 and underscoring persistent industrial cost pressures. On a monthly basis, PPI growth slowed to 0.1% from 1.4% in February. In our view, the elevated PPI points to an emerging additional driver that could sustain upward pressure on CPI domestically, raising the likelihood of a more hawkish turn by the regulator, which for now remains in wait-and-see stance. That said, CPI dynamics are heavily influenced by imports, given the economy’s high import dependence.

- At its May meeting, the Central Bank of Armenia kept the refinancing rate at 6.5% and left the interest rate corridor unchanged at 5.0%–8.0% (Lombard repo facility at 8.0%; the rate of borrowing funds from banks at 5.0%). The decision reflects a wait-and-see stance following an easing cycle that lowered the policy rate from 10.75% in June 2023 to 6.5% in December 2025. In our view, the current rate is close to neutral. Elevated prices increase the risk of a shift in the CBA’s rhetoric, but future moves will depend on the inflation trajectory.

Corporate News

Unibank has announced the placement of a new USD bond tranche totaling $5m, with a 5.6% annual coupon, payable quarterly. Each bond has a par value of $100, with a minimum investment of 10 bonds ($1,000). The issue will mature in 36 months.

Two-Week Outlook

Between May 8 and 18, a raft of key macro releases is due that could shape market sentiment. The marquee release is Q1 2026 GDP, with consensus looking for 4.1% YoY—consistent with a moderate cooling expected after a volatile start to the year. In parallel, we will closely watch April CPI. The forecast points to an acceleration in price growth to 4.7% YoY. If delivered—and set against elevated producer price inflation in recent years—this would underscore still‑sticky inflation and could weigh on market sentiment.

In our view, the juxtaposition of a sharp slowdown in industrial activity (+7.0% YoY) with a persistently overheated construction sector (+24.0% YoY) creates a mixed backdrop for the monetary regulator. Price pressure remains the primary risk: any sign of reacceleration in the upcoming data on inflation could prompt markets to reprice expectations toward a more hawkish policy path. Conversely, if inflation proves stable, the Central Bank is likely to maintain a wait‑and‑see stance.