Investment Review №337. A shift toward hedging

Against the current

Despite heightened uncertainty and rising risks, local index prices posted solid gains.

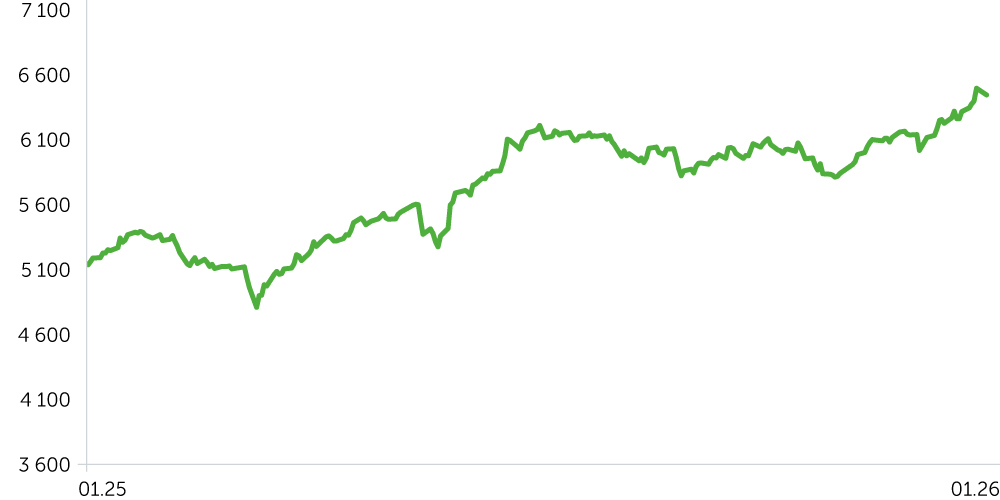

DFM General Index: 1-Year Dynamics

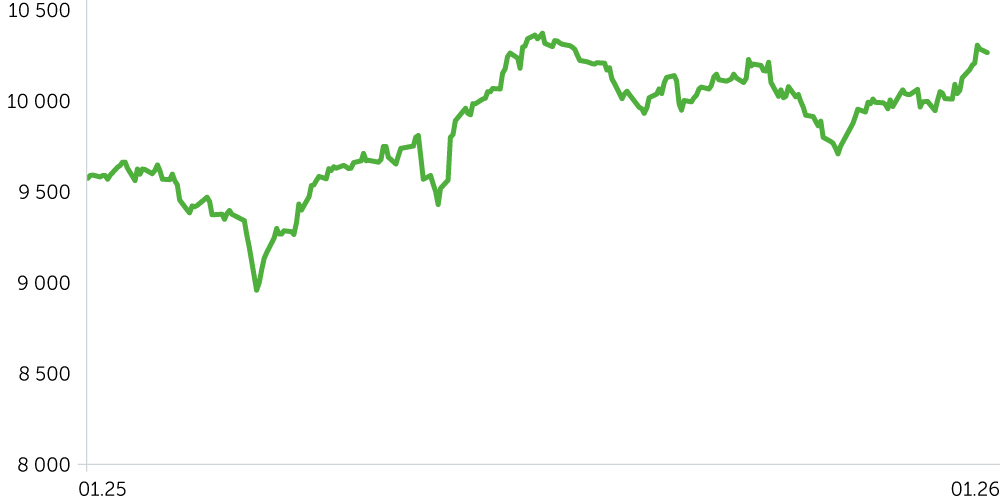

Abu Dhabi Securities Exchange Index: 1-Year Dynamics

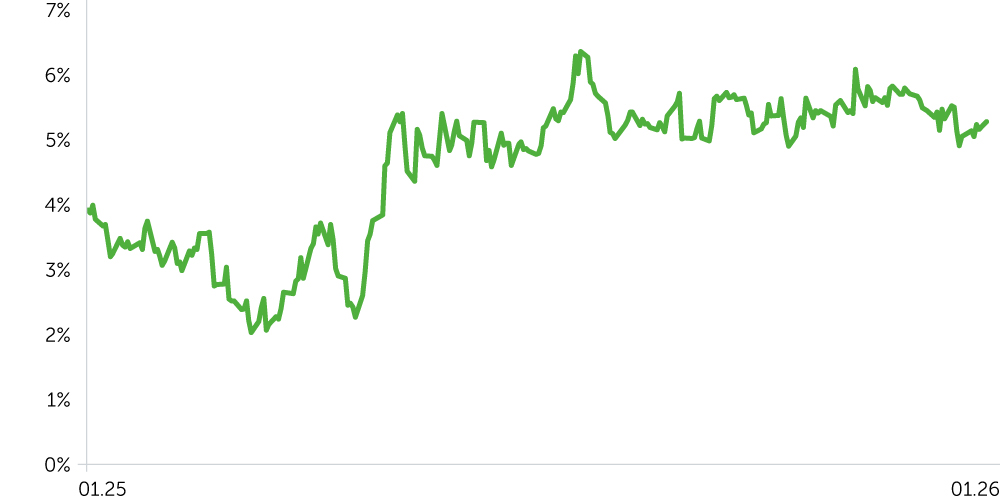

Yield, Forward Rate 1m10y, UAE, 1-Year Dynamics

Brent Oil, 1-Year Dynamics

Market Performance

- Between 12 January and 26 January 2026, UAE equity markets experienced moderate gains. Mid-January was characterized by ongoing frictions between the U.S. and Iran, while trilateral talks on Ukraine were held in Abu Dhabi. Over the period, the Dubai Financial Market (DFM) index rose 2.8% to 6,446 points, and the FTSE ADX General Index advanced 2.6% to 10,264 points. Brent crude prices were broadly flat, edging up just 0.3% from $65 to $66 per barrel. By contrast, the S&P 500 declined 0.4% over the same period, reflecting subdued sentiment in global markets.

- Communication Services led the gains, rising 4.9%, driven primarily by Emirates Telecommunications Group (e&), whose shares advanced 6.12%. The Energy sector also performed strongly, adding 4.1% over the past two weeks, with Dana Gas (+8.57%) emerging as the top performer. The company reported that it had reached a stable production level of around 70,000 barrels of oil equivalent per day—its highest figure in seven years—largely due to the early commissioning of a natural gas field expansion project in the Kurdistan Region of Iraq. The Financial sector posted solid gains as well, rising 2.55% on average, supported by Sharjah Islamic Bank (+12.30%) and Abu Dhabi Islamic Bank (+10.21%). The Real Estate sector delivered more modest growth of 1.5% on average, despite advances in Emaar Development (+3.96%) and Aldar Properties (+4.46%). Laggards over the period were Utilities (-1.3%) and Consumer Discretionary

(-0.5%). - The UAE 10Y sovereign proxy yield declined by 24.5 basis points over the period, from 5.51% to 5.27%, whereas the yield on 10Y U.S. Treasuries edged up by 2 basis points to 4.36%. As a result, the spread between the two yields narrowed to 91 basis points. Given that the UAE effectively imports the Fed’s monetary policy, such fluctuations around the long-term average spread are to be expected. Despite heightened geopolitical tensions, investors continue to take a positive view of the region’s credit risk, pointing to an ongoing reassessment of the UAE’s economic structure.

Economic Updates

- Risks of a U.S. military invasion of Iran. Iran continues to experience political and economic instability following widespread anti-government protests. Tighter sanctions, a more confrontational regional environment and the deployment of the aircraft carrier USS Abraham Lincoln to the Persian Gulf have further heightened market concerns. The UAE has reiterated that it will not allow its airspace, territory or territorial waters to be used for any strikes against Iran, instead calling for dialogue, de‑escalation, adherence to international law, and respect for state sovereignty. Iran accounts for roughly 3% of global oil production and exports around 2 million barrels of crude per day, almost all of which is shipped to China. Besides, Iran controls the Strait of Hormuz, a chokepoint through which about 30% of seaborne global oil trade passes each day, making it a recurring focus of market attention during periods of regional tensions.

- U.S. tariffs on countries trading with Iran. U.S. President Donald Trump has imposed a 25% tariff on any country doing business with the Islamic Republic of Iran, without specifying a detailed list of targeted states. Iran’s largest trading partner remains China, followed by Iraq, the UAE, Turkey, and India. This makes China and the UAE particularly exposed and places them among the countries likely to be hit hardest by the new tariffs.

- Trilateral talks on Ukraine in Abu Dhabi. On January 23-24, delegations from Russia, Ukraine and the United States held two days of talks in Abu Dhabi, marking the first negotiations in this trilateral format. The meetings were conducted behind closed doors. A new round of talks could take place as early as February 1, according to reports.

- Saudi Arabia’s NEOM project is under review. Saudi Crown Prince Mohammed bin Salman’s flagship project is set to be significantly scaled back and revised after years of delays and cost overruns. The government is reassessing the project’s budget amid substantial spending commitments related to hosting the World Expo in 2030 and the FIFA World Cup in 2034. Since NEOM’s launch in 2017, several megaprojects have been announced, including The Line, the Trojena mountain resort (originally slated to host the 2029 Asian Winter Games) and the Oxagon coastal logistics and industrial zone. Riyadh has also indicated that Trojena will be downsized and will no longer host the Winter Games as previously planned.

- Launch of advanced reasoning AI system in the UAE. The leading Abu Dhabi technology university has launched K2 Think, an AI system with advanced reasoning capabilities that researchers say is on par with the best open-source models from the U.S. and China, accelerating the UAE’s push toward “sovereign” AI. With Western developers yet to provide a clear response to the latest generation of Chinese open-source models, the project aims to begin closing that gap. The announcement comes amid recent research indicating that Chinese firms such as DeepSeek and Alibaba, for the first time last year, surpassed their U.S. competitors in the global market for open AI models.

Corporate News

- Sharjah Islamic Bank (+12.3%): the share price rose after the release of strong 2025 results. The bank reported a 26% YoY increase in net earnings, and the Board of Directors proposed that the shareholder meeting approve an increase in the cash dividend to 20% of capital (from 15% a year ago). Management also approved a plan to raise the bank’s capital, subject to regulatory and shareholder consent.

- Tecom Group (TECOM: +4.9%): acquired an educational campus in Dubai International Academic City for AED 125 million (around USD 34 million), as part of efforts to develop the UAE’s higher education sector. The transaction supports Dubai’s and the UAE’s position as a global hub for education and talent development, in line with the national higher education strategy until 2030.

Two-Week Outlook

The global energy market remains volatile due to the escalation of tensions in Iran. The Iran factor adds significant uncertainty to the outlook for oil prices. The start of a military operation may trigger a short-term spike in prices.

Over the next two weeks, the geopolitical backdrop and news flow may drive global risk sentiment, which will in turn influence UAE markets. Next week, the U.S. is also supposed to announce its first interest rate decision in 2026. Given the AED’s peg to the USD, the UAE Central Bank is expected to follow the Fed’s move, which could introduce volatility into equities in interest rate-sensitive sectors of the UAE economy.

At the same time, the UAE’s largest companies are set to report their Q4 2025 results in late January. Given the strength of the economy, we expect broadly solid corporate earnings, which could act as a positive fundamental catalyst for the market.

From a technical perspective, signals point to a trend reversal. The DFM has broken above both its 50‑day and 200‑day moving averages, and the January decline amid geopolitical developments has been fully retraced.

Shifts in the oil market and global risk appetite may affect the ADX via the energy sector and the DFM through capital inflows and outflows in higher-beta financial and real estate names.