Investment Review №340. The Bombshell Effect

Cooling Economic Activity with Elevated Inflation Risks

Strong fourth-quarter macro data supported solid gains in local equities

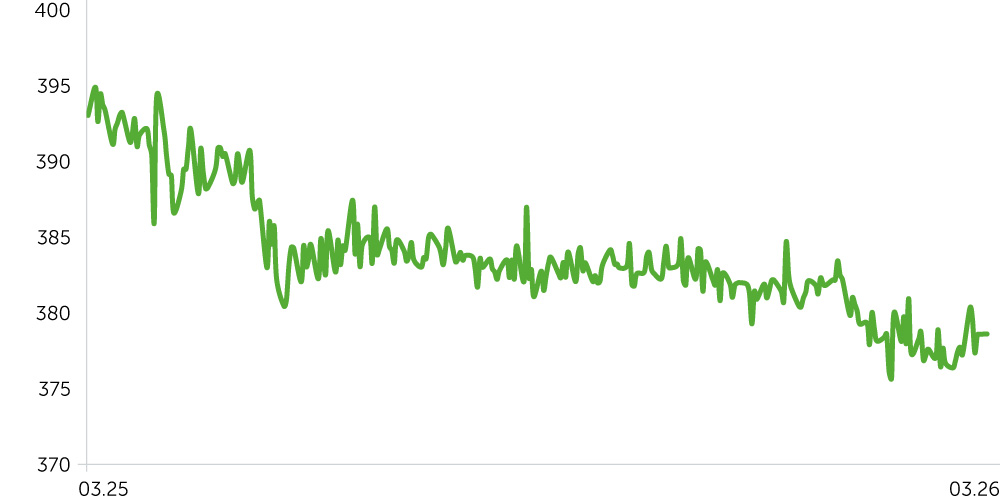

Telecom Armenia: 1-Year Stock Trends

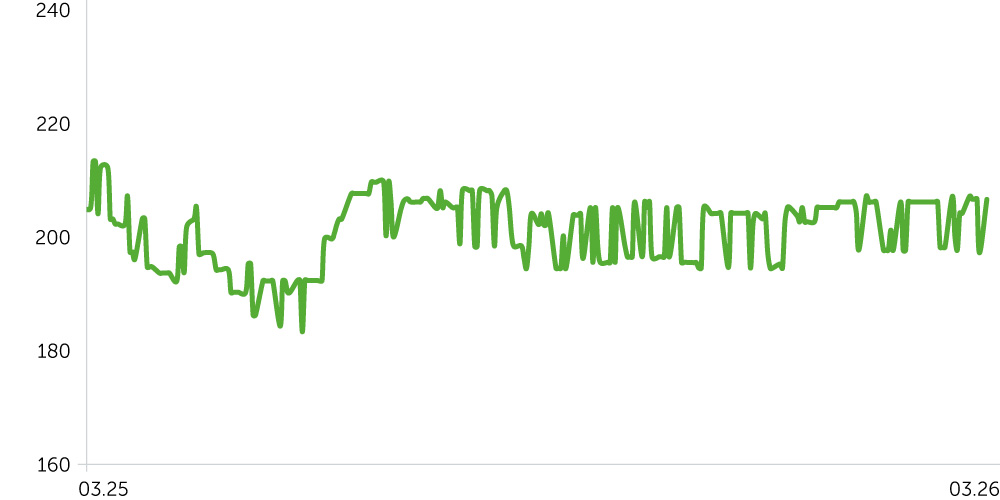

ACBA Bank: 1-Year Stock Trends

USD/AMD: 1-Year Dynamics

3-Year Corporate Bond Index (AMD) – Post-Update

Market Overview

From February 23 to March 9, 2026, local market dynamics were moderate amid mixed macro data and heightened global uncertainty. Acba Bank (ACBA) traded sideways in the lack of material corporate news, while Telecom Armenia (AMTL) edged down 0.3%. The January economic activity index underscored fundamental resilience, posting a solid 7.6% YoY gain and cooling from December’s 18-month non-interest value [OS1.1]. By contrast, foreign trade turnover fell 12% YoY, reflecting a contraction in re-exports of precious metals and stones after December’s surge. International reserves climbed to a record high (+57.6% YoY), providing a meaningful external buffer against unpredictable shocks. Even so, the macro backdrop has turned more complex with inflation running above the CB’s target and additional pro-inflationary risks tied to the military escalation in the Middle East, where retaliatory strikes by Iran, Israel, and the U.S. pushed global oil prices above $100/bbl.

In the debt market, the 3-year corporate AMD bond price index continued to strengthen, rising 0.2% and pulling yields back to one-month lows. Still, the Middle East conflict and higher oil prices pose clear risks for Armenia—an energy importer—via imported inflation and softer economic growth driven partly by potentially higher logistics and production costs. With price growth above target and inflation risks increasing, the likelihood of a more hawkish CB stance—and potential near-term rate hikes—has risen. The AMD appreciated 0.5% against the USD over the period, though FX rate volatility may intensify if global energy prices continue to climb.

Economic Updates

Between February 23 and March 9, Armenia’s macro indicators pointed to a moderation in economic momentum, reflecting slower activity in manufacturing, trade, and construction. Meanwhile, in February, inflation accelerated, exceeding the CB’s target. The S&P Global Ratings agency continues to assess risks to the economy’s financial stability as contained.

- Armenia’s consumer inflation accelerated to 4.3% YoY in February 2026, above expectations (3.9%) and the CB’s target pange (3% ±1 percentage points). The largest increases came from alcohol and tobacco (+10.3% YoY; +1.7% MoM), food (+6.5% YoY; +1.0% MoM), education (+8.3% YoY; 0% MoM), and healthcare (+4.5% YoY; +2.0% MoM). Price growth remains above the CB’s comfort zone despite cooling economic activity. This backdrop tilts risks toward a near-term policy tightening if inflation pressures persist and/or external inflation factors intensify.

- Armenia’s trade deficit narrowed even as turnover contracted. Foreign trade turnover fell 12% YoY and 49.2% MoM. Exports declined 13.5% YoY and 55% MoM, imports dropped 11.2% YoY and 45.2% MoM. The pullback largely reflects the reduction in re-exports (particularly, precious metals and stones) that demonstrated a one-off surge in December 2025.

- The economic activity index rose 7.6% YoY in January but fell 48.3% MoM, driven by broad-based cooling across key sectors. Manufacturing YoY growth slowed to 10.6% in January from 38.6% in December (‑56.7% MoM), trade growth eased to +0.7% from +3.2%, and construction rose 18.7% YoY (vs 20.5% in December) but declined 86.6% MoM.

- S&P Global Ratings highlighted Armenia’s external buffer, with its international reserves reaching a record $5.2bn in January (+57.6% YoY). Overall, the agency assesses risks to Armenia’s financial stability as contained. It projects inflation easing to ~3.2% in 2026 amid a gradual moderation in economic activity, with economic growth of roughly 5.3% in 2026 and 4.8% in 2027.

Corporate News

- Acba Bank (ACBA) announced a public offering of 5-year AMD bonds with a 10.25% annual coupon, paid semiannually, and a total issue size of AMD 10bn. The bonds mature on February 23, 2031.

Two-Week Outlook

Between March 13 and March 23, market focus in Armenia will center on the Central Bank’s policy decision. Our base case is a hold at 6.5%, with a wait-and-see stance, as the recent price uptick appears one-off rather than structural. That said, amid external inflationary pressures, a tightening move cannot be ruled out. Revisions to previously released indicators are also possible.

In the coming days, February readings of the economic activity index—where we do not anticipate material surprises—together with data on industrial output and on exports and imports, which have shown increased volatility in recent months, will be important for the market. These releases, alongside developments in the Middle East, should allow for a more precise assessment of domestic demand and the external sector and help recalibrate expectations for the trajectory of prices and policy rates.