Investment Review №345. Treasuries vs Stocks

Corporate News in Focus of Our Analysts

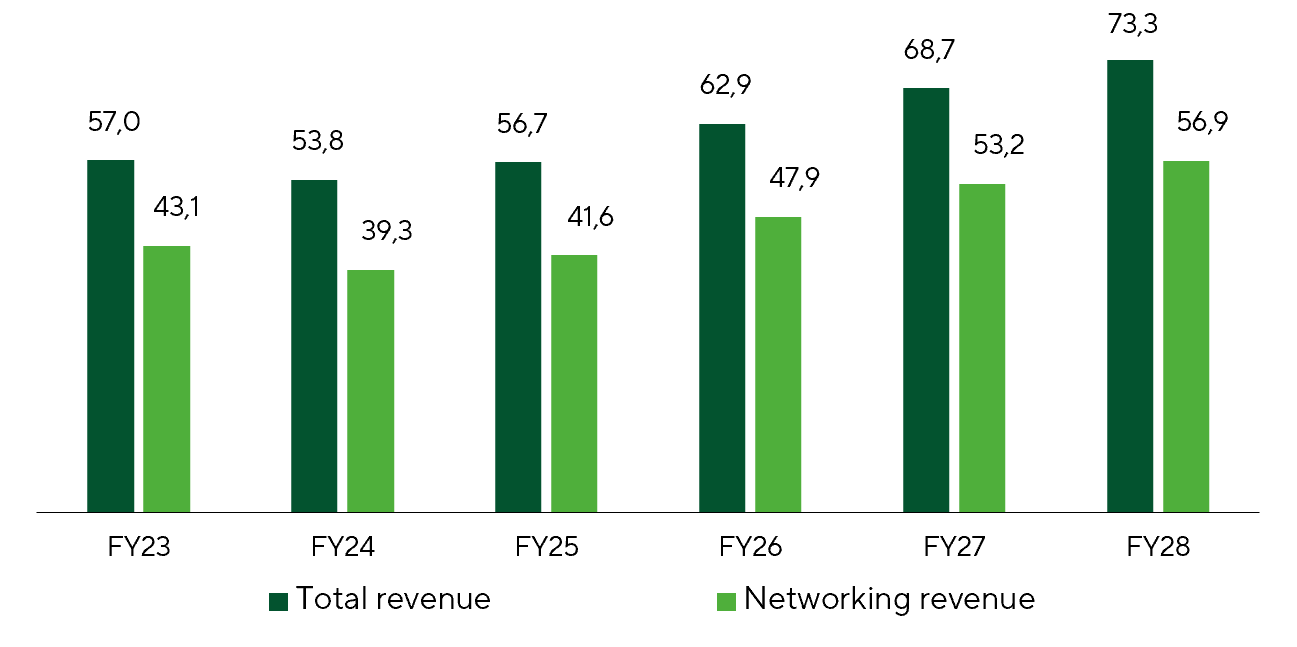

Cisco Systems

On May 13, Cisco Systems (CSCO) reported Q3 FY26 results that clearly beat expectations and an important step toward cementing the company’s role as a core infrastructure provider in the AI era. Revenue, EPS, and margins all exceeded guidance and market expectations. More importantly, the order book expanded: product orders increased across the business—not just from hyperscalers—giving Cisco greater backlog visibility and stronger demand visibility than in prior cycles. Networking is solidifying as a growth engine: hyperscaler AI buildouts and the nascent corporate campus refresh cycle are complementary, mutually reinforcing tailwinds. Management materially raised full-year guidance and its outlook for AI infrastructure demand and offered an encouraging early view of FY 2027. While gross margins remain pressured by higher memory costs and increasing hardware mix, mitigation actions appear to be working and margins have likely stabilized. CSCO shares closed up 13.4% on May 14.

Revenue dynamics of Cisco Systems (CSCO), $ bn.

Sources: FactSet, Freedom Broker

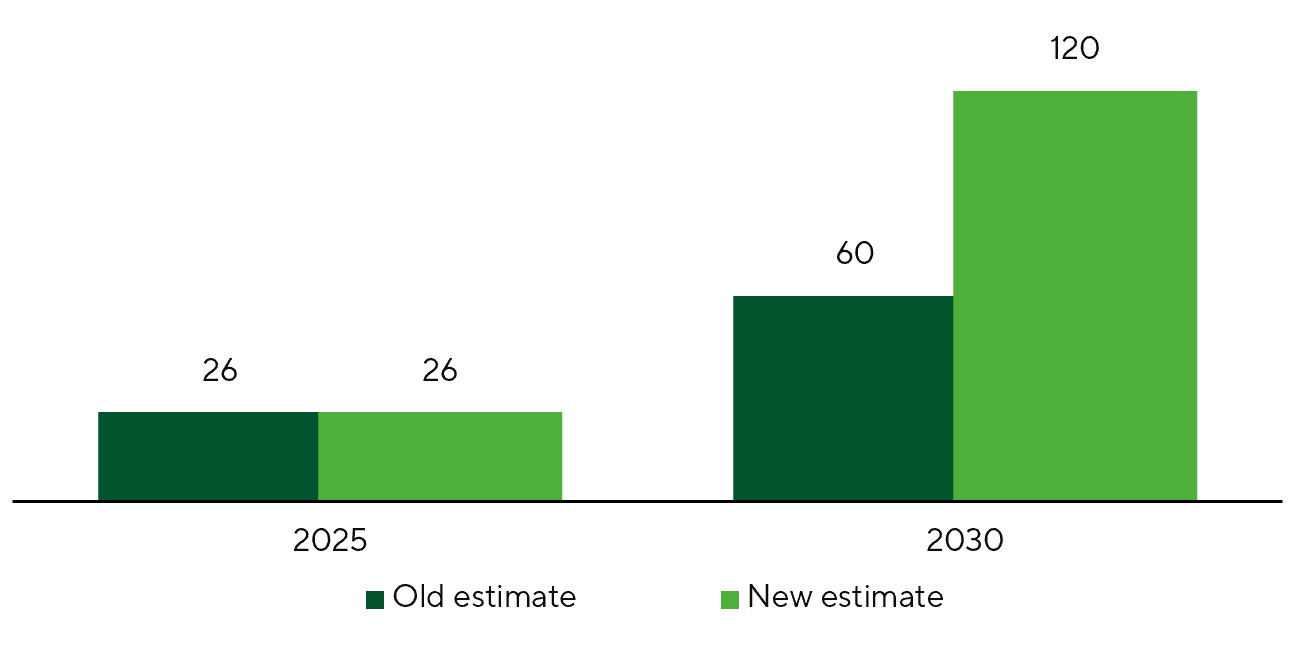

AMD

On May 5, AMD, Inc. (AMD) reported strong Q1 FY26 results, issued upbeat guidance that boosted investor sentiment, and presented encouraging long-term CPU market forecasts. The company exceeded both its own guidance and the high end of market expectations across all key metrics, with structural margin expansion driven by a favorable revenue mix shift toward the Data Center segment. Two items stood out: management effectively doubled its server-CPU TAM forecast and highlighted robust demand for MI450 accelerators for 2027. As early as 2027, AI accelerators could generate “tens of billions of dollars” in revenue for AMD, with potential for further upward revisions as additional contracts are signed. AMD now expects server-CPU TAM to exceed $120bn by 2030, versus a $60bn estimate announced in November—implying an increase in the expected CAGR from roughly 18% to more than 35%. AMD shares rose 18.6% on May 6.

TAM of server CPU, $ bn.

Sources: AMD, FactSet, Freedom Broker

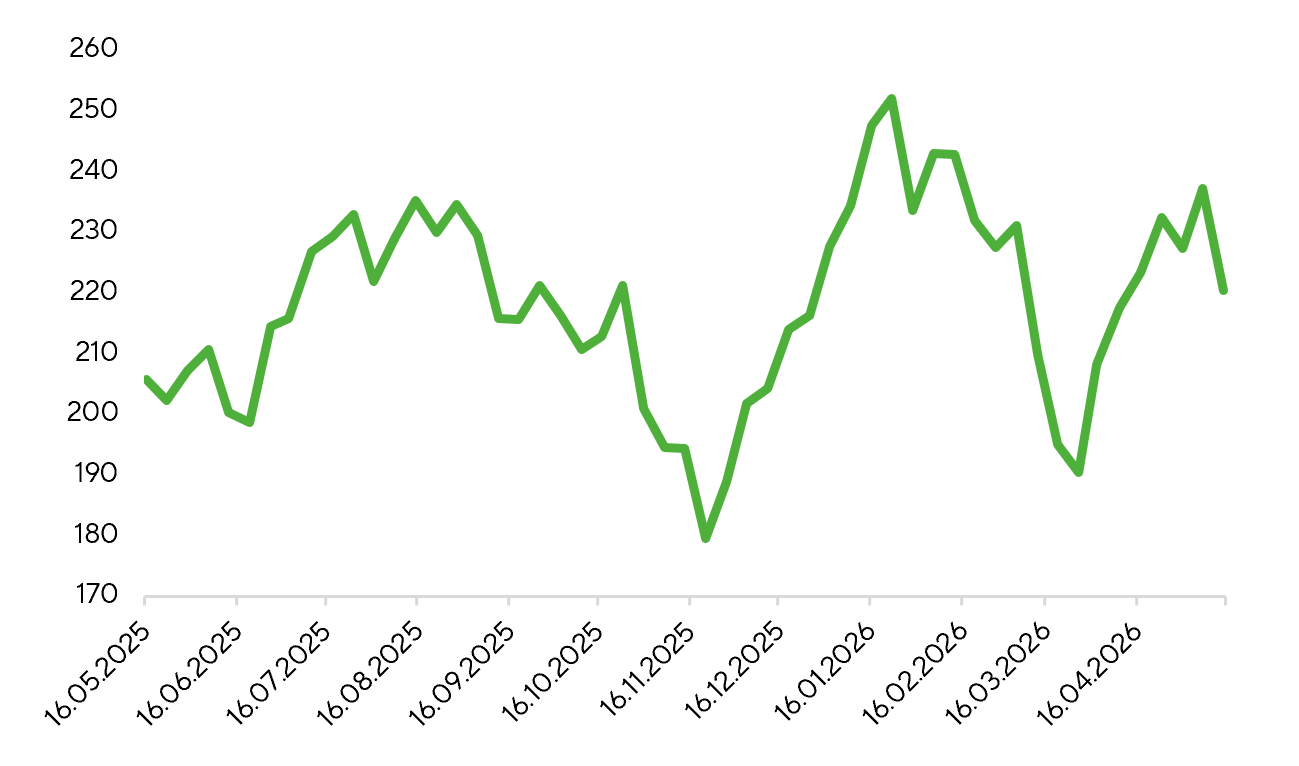

Boeing

Media reports suggest Chinese airlines may place a major order with Boeing (BA) for ~200 aircraft, potentially announced following Donald Trump’s recent visit to China. The prospective deal is viewed as part of broader efforts to restore trade and economic ties between the two countries and could represent Boeing’s largest order in several years.

Reportedly, the order would be predominantly for narrow-body 737 MAX aircraft, with a possible addition of wide-body models for long-haul routes. For Boeing, this would be a significant opportunity to reinforce its position in a strategically important market after an extended period of restrictions and geopolitical tensions. While there has been no official confirmation, markets are already incorporating the potential order into expectations for demand and Boeing’s capacity utilization.

Boeing Share Price.

Source: FactSet

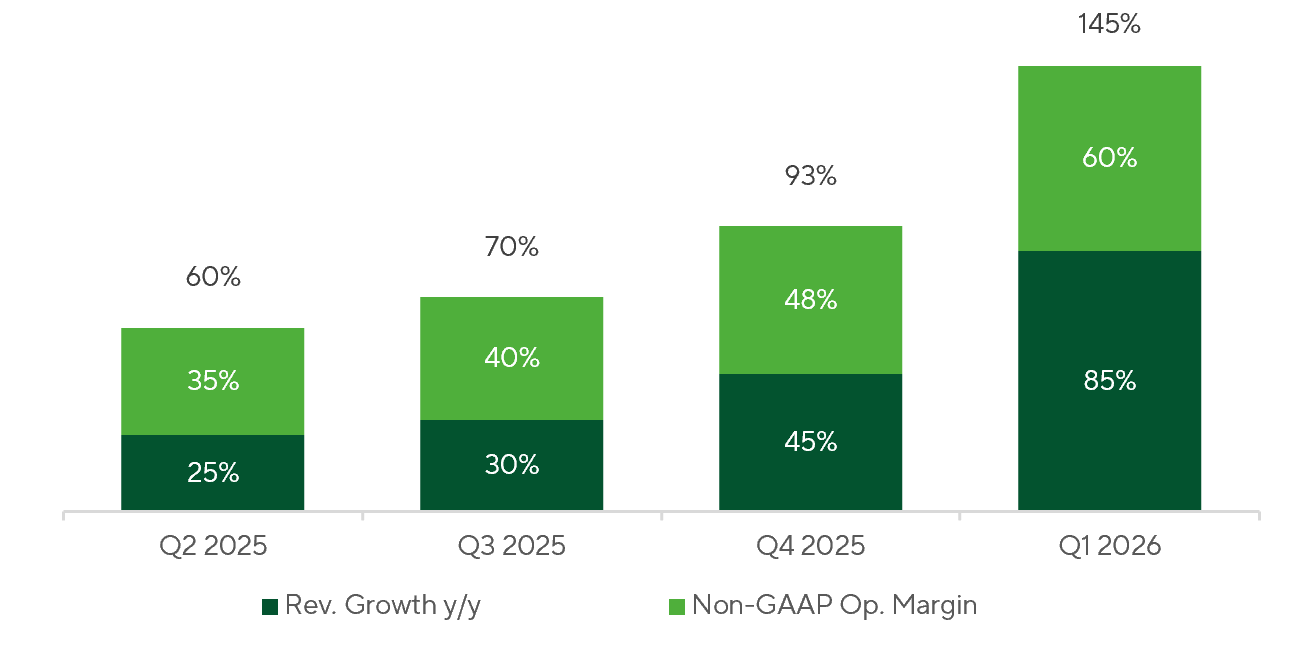

Результаты Palantir

Palantir (PLTR) delivered very strong Q1 2026 results, materially exceeding both its own guidance and market consensus across key metrics. The primary driver was, once again, the U.S. Government segment, where demand for defense and intelligence solutions remains sufficiently strong that the company is prioritizing these contracts over certain commercial projects. In this context, revenue, earnings, and margins came in well above management’s guidance, underscoring not only the strength of demand but also the platform’s scalability. Another constructive signal was robust growth in the contracted backlog, improving visibility for further revenue expansion. Most notably, the company’s outlook for next quarter was ahead of market expectations, and management raised full-year guidance meaningfully. This suggests the current momentum is not one-off, but rather indicative of a sustained business acceleration. Looking ahead, the key growth drivers remain the expansion of U.S. government programs, deeper integration of the AIP platform into enterprise workflows, and further strengthening Palantir’s position as an infrastructure layer for the secure deployment of AI across complex organizations.

Efficiency histogram: PLTR outperforms Rule 40.

Source: PLTR IR Presentation

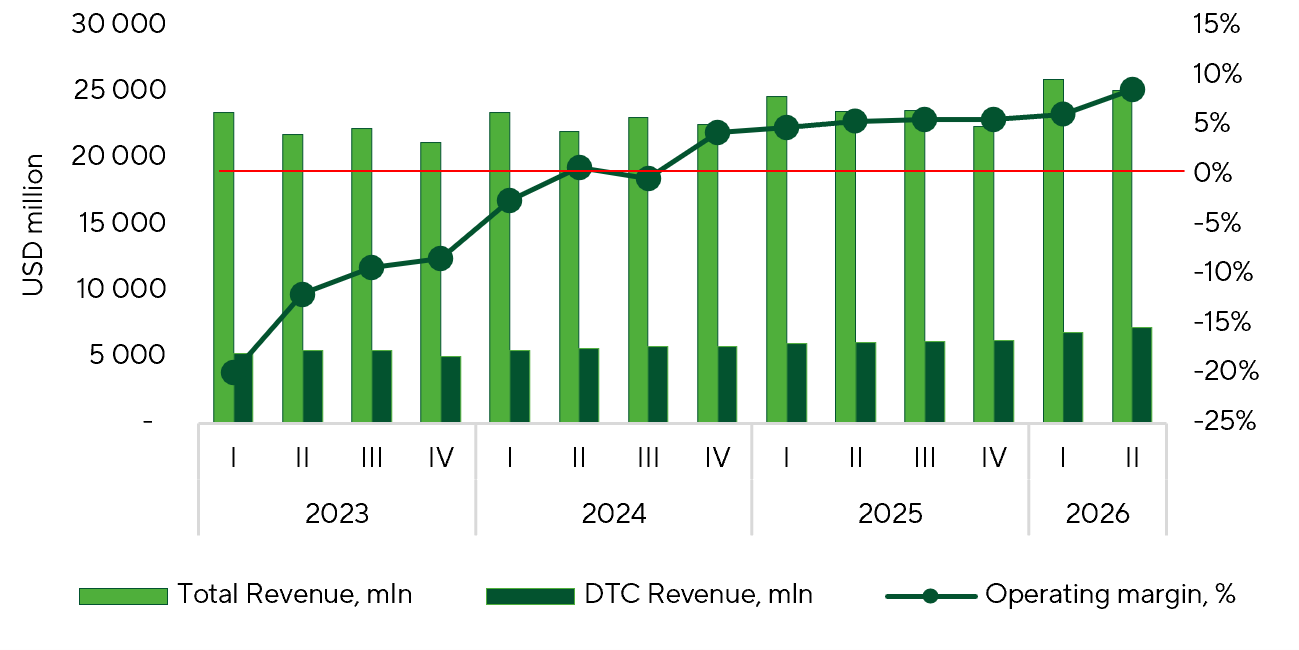

Walt Disney

Walt Disney (DIS) delivered strong revenue growth in Q2 FY26, driven by standout theatrical performance, continued momentum in streaming, and record revenue from its theme parks. Revenue rose 7% YoY to $25.17bn, while total operating income grew 4% YoY to $4.60bn. The Entertainment segment delivered 10% YoY revenue growth to $11.72bn, supported by robust box office results—led by Beastopolis 2 and ongoing contributions from Avatar: Flame and Ashes—and solid streaming growth. Segment operating income rose 6% YoY to $1.34bn on higher subscription and advertising revenue. Streaming continued to deliver solid top-line growth and, for the first time, achieved a double-digit operating margin. SVOD revenue increased 13% YoY to $5.49bn, with subscription revenue up 16% YoY due to both subscriber growth and price increases. Streaming advertising revenue grew 12% YoY. SVOD operating income surged 88% YoY to $582m, compared with $310m a year earlier. Management noted that integrating Hulu into Disney+ is improving retention and reducing churn. The Experiences segment (theme parks and cruises) reported record Q2 revenue and operating income. Segment revenue rose 7% YoY to $9.49bn, and operating income increased 5% to $2.62bn. Growth was driven by a 5% increase in average per-capita spending at U.S. parks, the successful launch of the Disney Adventure cruise ship in Asia, and the opening of the World of Frozen land in Paris.

DTC Revenue and Operating Margin.

Source: FactSet