Investment Review №333. Right to hedge

Corporate News In Focus of Our Analysts

AMD (AMD)

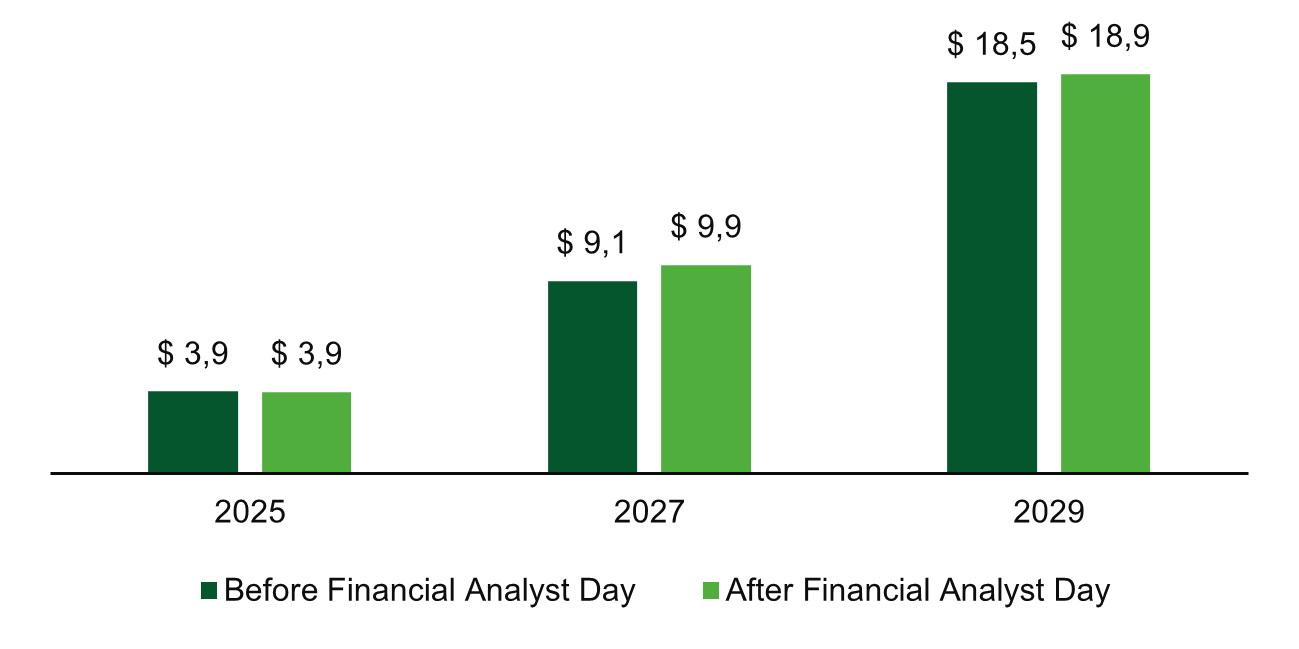

On November 4, AMD, Inc. (AMD) delivered a strong quarterly report and issued an upbeat outlook for the current quarter, beating market expectations across all key metrics and business segments. Despite the solid results, the stock saw a technical pullback after gaining more than 150% over the prior six months. Just a week later, on November 11, the company held its Financial Analyst Day, unveiling an ambitious long-term strategy and financial targets that exceeded investor expectations across the board. Management outlined a path to leadership in the HPC and AI markets, estimating the total addressable compute market at $1 trillion by 2030. A central focus of the presentation was AMD’s long-term financial outlook. Management now projects 35%+ revenue CAGR over the next 3–5 years, which would support stronger margins and EPS expansion. The most striking target was the company’s goal of achieving adjusted EPS above $20. AMD shares rallied 9% the day after the presentation.

Consensus EPS (est.) for AMD, $.

Sources: FactSet, Freedom Broker analysis

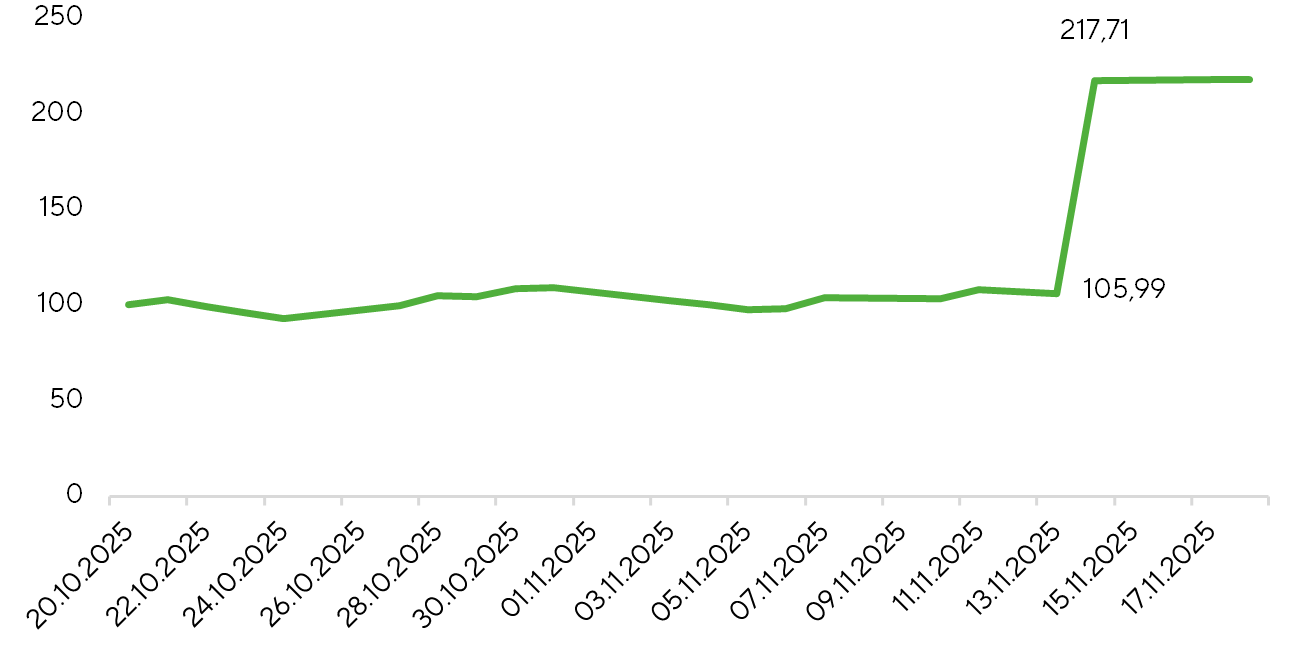

Merck (MRK) — Acquisition of Cidara Therapeutics (CDTX)

Merck announced the acquisition of Cidara Therapeutics for $9.2 billion, aligning with its long-term strategy to prepare for the patent expiration of Keytruda in 2028. The key asset in the deal is CD388, an investigational influenza-prevention therapy designed to provide broad protection against all known seasonal and potentially pandemic strains of influenza A and B through a single subcutaneous or intramuscular dose. The drug maintains efficacy regardless of a patient’s immune status, making it especially valuable for immunocompromised individuals who respond poorly to traditional vaccines. CD388 is currently in Phase 3 trials, with interim results expected after the end of the Northern Hemisphere flu season in June 2026. Based on our assessment, a commercial launch could be possible as early as 2027–2028, assuming positive data. The acquisition is expected to close in 1Q26.

CDTX price chart, $

Sources: FactSet, Freedom Broker analysis

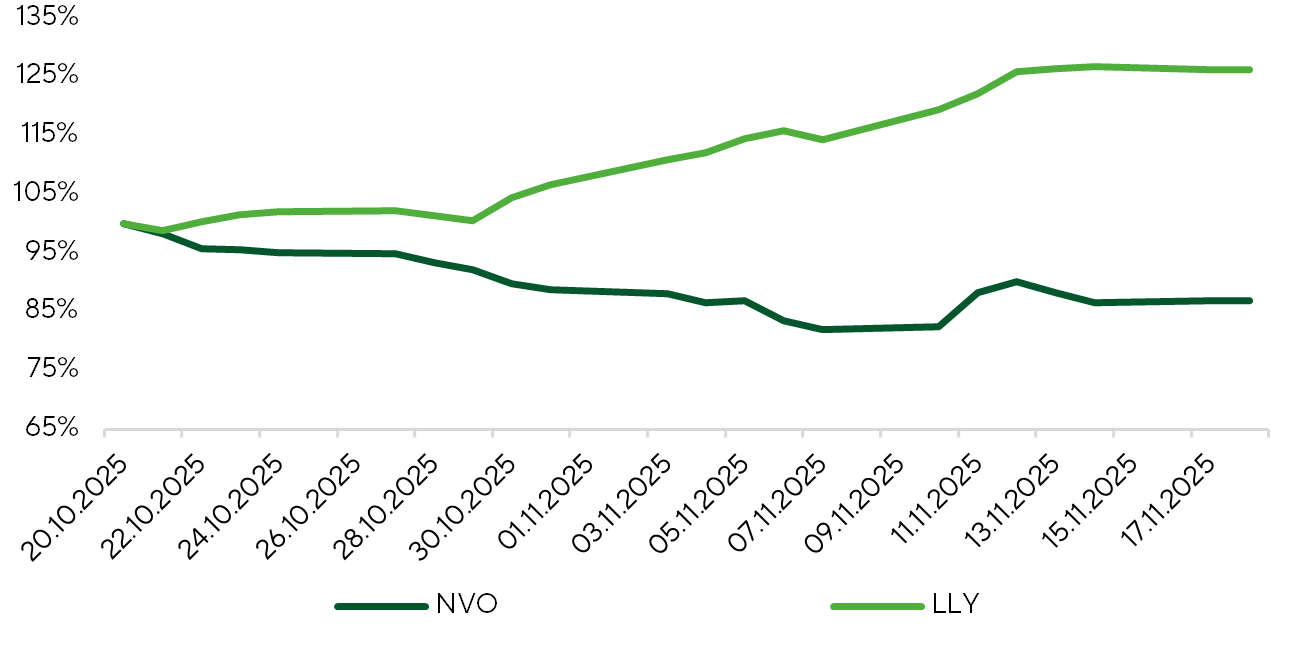

Eli Lilly & Novo Nordisk

On November 6, Eli Lilly and Novo Nordisk announced an agreement with the Trump administration that will sharply reduce prices for GLP-1 drugs and insulin within Medicare/Medicaid through the new TrumpRx platform. Under the deal, injectable GLP-1 therapies will cost about $350 per month (roughly 70% below current levels), while oral formulations will be available starting at $150 per month. In return, the companies will receive a three-year exemption from import tariffs, as well as the ability to expand Medicare/Medicaid coverage to include obesity treatment — a major shift, as these programs previously reimbursed only diabetes therapy. According to Eli Lilly, the policy change opens access to an additional patient pool of roughly 40 million people. Despite lower prices in government programs, pricing in the self-pay and direct-to-consumer (DTC) segments remains unchanged. Overall, the agreement appears highly favorable for both companies: the significant expansion of the eligible patient base should offset potential margin pressure.

LLY and NVO price chart

Sources: FactSet, Freedom Broker analysis

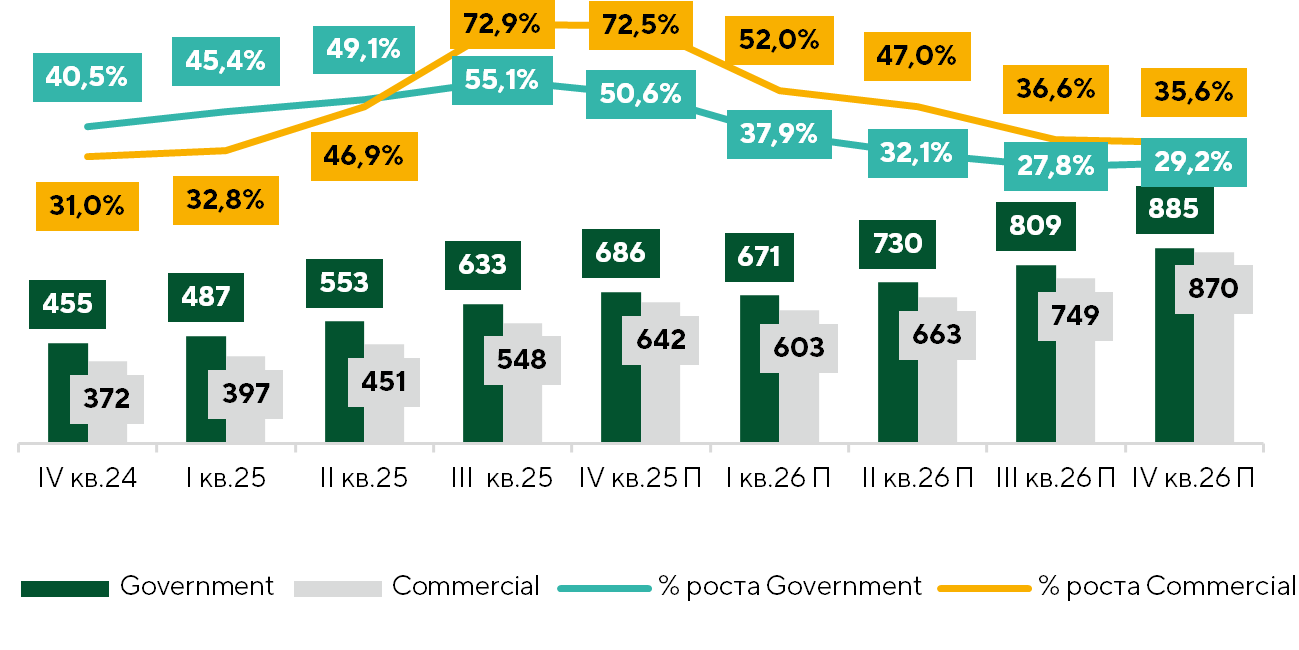

Palantir (PLTR)

Palantir significantly outperformed market expectations in the third quarter of 2025. The primary growth driver was the accelerating momentum in the U.S. commercial segment, where revenue surged 121% y/y on the back of a record volume of new contracts and rapid adoption of AIP (Artificial Intelligence Platform). At the same time, revenue in Europe remains stagnant. The company expects further strengthening of its financial performance in 4Q25, above current market forecasts. However, investors are increasingly factoring in key risks for 2026: a likely slowdown in U.S. commercial growth after record expansion, potential pressure from reduced defense spending, and margin headwinds driven by rising hiring costs for AI specialists. Palantir’s current premium valuation implies that both the 2025 results and a sustained long-term hyper-growth trajectory are already fully priced in—an inherently difficult pace to maintain. This creates a risk of limited upside for the stock.

Revenue ($ million) and growth rates (%) Palantir by segment

Sources: FactSet, Freedom Broker analysis

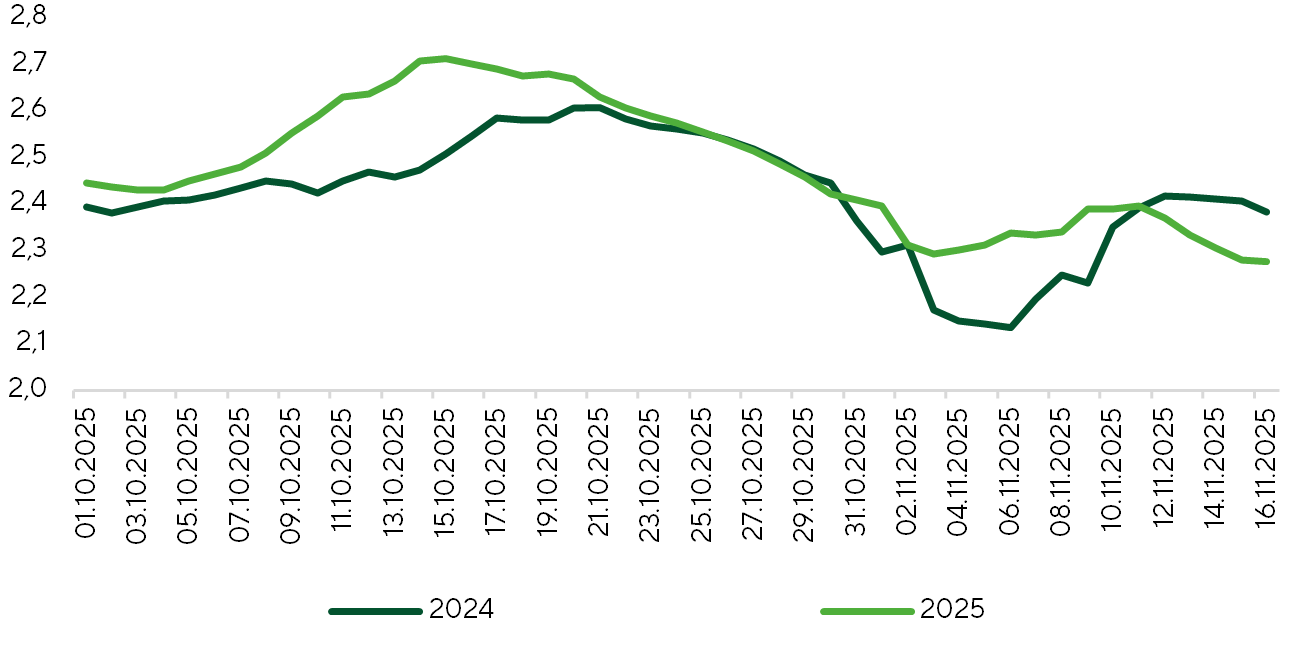

Airline Sector — Operational Disruptions Intensify

During the shutdown, airlines faced severe operational disruptions: more than 10k flights were canceled or delayed due to shortages of air-traffic controllers and Transportation Security Administration staff, many of whom went unpaid and were forced into unpaid leave. The Federal Aviation Administration (FAA) was compelled to reduce flight volume by 10% at major U.S. airports, including New York, Los Angeles, and Washington. According to TSA data, weekly passenger throughput as of November 17 is down roughly 5–6%.

The November 12 reopening of the government immediately restored funding and allowed air-traffic control and security operations to resume, easing the operational strain on airlines as they work to fully normalize their schedules. However, some media outlets report that a complete recovery has not yet occurred. Looking ahead, this should help airlines capitalize on the critical Thanksgiving travel period. Still, share prices may remain under pressure given that government funding has been extended only through the end of January 2026.

Average daily passenger traffic at US airports, million people

Sources: FactSet, Freedom Broker analysis