Investment Review №334. Customer return

December 2

Global Perspective

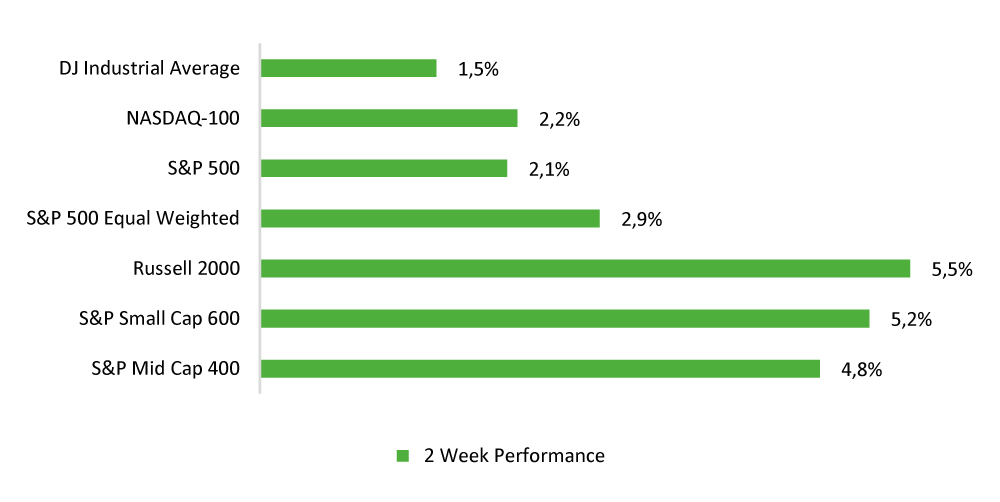

Over the past two weeks, bulls have firmly taken control of the U.S. equity market, with major benchmarks showing broad-based strength: the S&P 500 gained 2.1%, the NASDAQ 100 rose 2.2%, and the Dow Jones Industrial Average added 1.5%. The strongest impulse came from small caps — the Russell 2000 jumped 5.5%, reflecting a renewed appetite for risk assets. The market has entered a broad-based rebound following the recent correction. The rebound started with improving market breadth, and the technical setup now points to room for further expansion of the rally.

Expectations around the December FOMC decision remain the central focus and have been extremely volatile throughout November. Until recently, markets leaned toward the Fed keeping rates unchanged. But the past two weeks marked a turning point: a series of relatively soft macro releases (weak labor-market indicators, moderate PPI growth) combined with dovish-leaning remarks from select Fed officials shifted expectations sharply. This became the key fundamental trigger supporting a renewed “risk-on” regime across asset classes.

Sources: FactSet, Freedom Broke

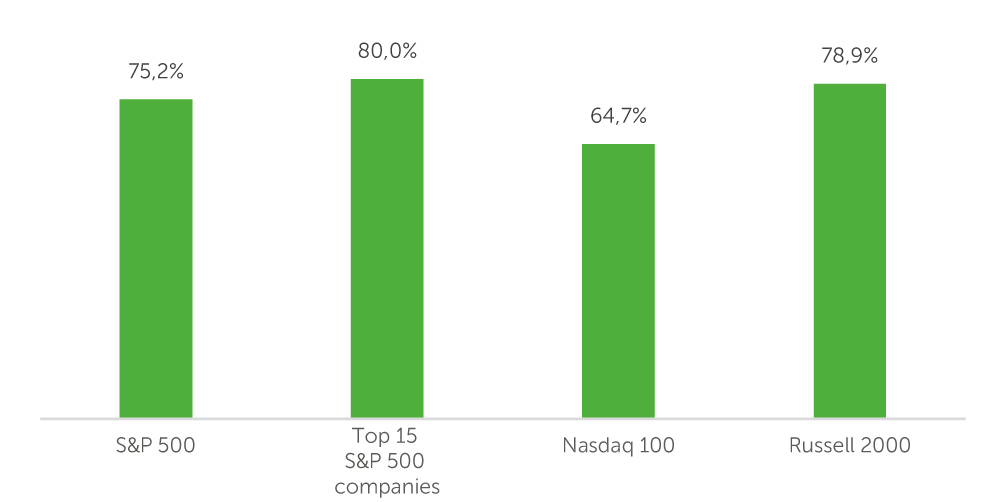

The picture of the broad rebound is confirmed by indicators tracking the share of benchmark constituents with positive returns over the review period. In the S&P 500, more than 75% of companies finished the two-week interval in positive territory, with a median gain of 2.35%. A similar pattern was observed in small caps: breadth reached 79%, while the median increase was significantly higher at 4.84%, highlighting renewed demand for more volatile niches. Even the IT

sector, which had previously been under pressure from AI-related profit-taking, showed signs of stabilization: breadth rose to 65%, and median returns reached 1.51%. Although the sector still lagged the broader market in terms of the overall scale of the recovery, its breadth more than doubled compared with mid-November, indicating a noticeable normalization of the group’s internal dynamics.

Market breadth: share of companies with positive returns

Sources: FactSet, Freedom Broker

On November 28, the S&P 500 decisively moved above all key moving averages, including the 20-day — traditionally viewed as a signal for further upside momentum. The equal-weight S&P 500 outperformed the headline index by 0.7 p.p. over the same period, a divergence typically interpreted as a shift from a narrow mega-cap–driven market to a more structurally robust, broad-based advance.

The key driver behind the shift in sentiment was a fresh round of repricing in expectations for a December rate cut. Comments from New York Fed President John Williams and several other officials were perceived as softer than expected, particularly against the backdrop of renewed macro releases that largely undershot consensus. As a result, by November 21, futures markets were pricing the probability of a December 25 bp rate cut above 80%, whereas just a week earlier it had fallen below 30%. The market effectively concluded that the dovish camp within the Fed had strengthened, especially given signs of labor-market cooling.

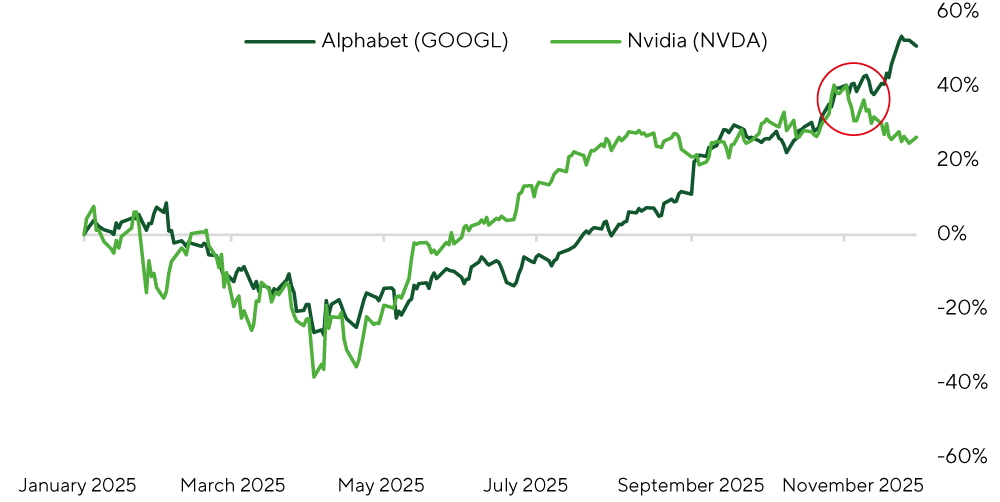

Against the backdrop of improving sentiment, ten of eleven S&P 500 sectors finished the period higher, led by Communication Services, which gained 6.8% on strong advances in Alphabet and Meta. Alphabet (GOOG +10.3%, GOOGL +10.4%) and Meta (+6.5%) accounted for nearly half of the sector’s total advance. Additionally, a notable theme was the divergence between Alphabet and Nvidia: while Nvidia pared back 3.58%, Alphabet posted double-digit gains — a rotation we attribute to a tactical shift in the AI narrative toward alternative compute architectures. Google’s new generation of TPUs has demonstrated strong competitiveness and potential advantages over GPUs in several key workloads, including training and inference of large models. This has called into question the durability of NVIDIA’s former dominance in AI infrastructure and prompted capital to rotate into GOOG/GOOGL as technologically strengthened and relatively undervalued names

Normalized returns of GOOGL and NVDA stocks

Among macro releases, the key factors driving the latest rise in expectations for a December rate cut were the labor-market report and the producer-price data (PPI) for September, published on November 20 and 25, respectively.

The labor-market data, collected before the shutdown, were mixed: the unemployment rate rose to 4.44% from 4.32% a month earlier, exceeding consensus and signaling a gradual cooling of the labor market. At the same time, payrolls increased by 119,000, nearly twice expectations. The rise in unemployment was largely driven by an increase in labor supply, reflecting changing household behavior as well as revisions to the August data. Even so, the combined signal confirmed relative labor-market softness, and investors interpreted this weakness as supportive of faster Fed policy easing.

The PPI report, in turn, confirmed that inflation remained modest in September. The headline index rose 0.31% MoM, matching the 0.3% consensus forecast, while the core index, excluding food and energy, increased only 0.1% MoM, below the 0.2% consensus estimate.

анные индекса цен производителей сигнализировали об умеренной инфляции: общий индикатор в соответствии с консенсусом вырос на 0,31% м/м, базовый (без учета цен на продовольствие и топливо) повысился на 0,1% м/м при средних прогнозах 0,2% м/м.

Market Focus

The next two weeks are packed with headlines, and market narratives will be shaped by a mix of macro releases and the remaining Q4 corporate earnings.

The Fed’s rate decision is expected on December 10. Rate expectations, as noted earlier, have been highly volatile. As of the close of the main session on December 1, markets were pricing an 87.4% probability of a 25 bp cut. The Fed will have to make its decision without October CPI data. Although the CPI release had initially been expected on the morning of December 10, the Bureau of Labor Statistics (BLS) canceled the October survey; the next inflation datapoint will be the November report on December 18, while the October figures will be reconstructed through interpolation—effectively as the average between September and November.

Even so, we remain inclined to believe that the Fed will cut rates in December. Policymakers have repeatedly emphasized that, under current conditions, supporting the labor market is the priority, and the rise in unemployment in September is a meaningful argument in favor of easing. The moderate PPI data further reinforce the absence of persistent inflation pressure at the producer level.

Alongside the rate decision, the Fed will publish updated economic projections. We expect that, compared with the September forecasts, only the unemployment projection is likely to change.

The other projections are unlikely to be revised, as the data gap leaves policymakers unsure of how the economy has shifted relative to prior estimates.

Another focal point for the market will be the release of November labor-market data on December 16. The FactSet forecast implies an unemployment rate of 4.5% (rounded), up from the rounded 4.4 percent in October. For the market, a negative surprise could once again be interpreted positively—as in the previous release—potentially strengthening expectations of further easing and supporting demand for risk assets heading into year-end.

Corporate developments will also attract attention. Earnings season is nearly complete, but several companies of interest in the current environment will report their results:

On December 11, Broadcom (AVGO) will release its Q4 report. The company is one of the key beneficiaries of the AI cycle thanks to strong positions in custom AI accelerators, networking solutions, and infrastructure software. AVGO shares have been in the spotlight in recent weeks amid growing interest in Google’s TPU architecture: Google co-develops some AI chips with Broadcom and purchases its networking solutions, so improved sentiment around Google’s AI prospects has already fed into higher expectations for AVGO. Last quarter, Broadcom reported record revenue of 15.95 billion dollars (22% YoY), with the semiconductor segment up 26% YoY and AI-related semiconductor revenue accelerating 63% YoY to 5.2 billion dollars. Profitability remains highly robust: adjusted EBITDA reached 10.7 billion dollars, or 67 percent of revenue, reflecting strong operational efficiency. Free cash flow reached 7 billion dollars—up 47% YoY thanks to exceptionally high cash-conversion levels.

On December 18, Nike (NKE) will report its Q2 FY2026 results. The global leader in athletic apparel and footwear is undergoing an operational restructuring. NKE shares have come under pressure in recent months due to weak gross-margin dynamics and uneven regional demand recovery, but the stock has begun to show signs of stabilization as the company advances its “Win Now” initiatives across key categories and distribution channels. Last quarter, Nike posted modest 1% revenue growth to 11.7 billion dollars, with meaningful channel divergence: Nike Direct sales fell 4%, while wholesale sales increased 7% on recovering North American demand. A notable element of the prior report was the 320 bp decline in gross margin to 42.2%, reflecting higher discounting, a mix shift toward wholesale, and rising U.S. tariffs. Management continues to emphasize cost control: operating expenses fell 1%, and marketing and promotional spend declined 3%. For the upcoming quarter, consensus expects 4.3% QoQ revenue growth, which—combined with disciplined cost management—could generate upside for EPS.

Technical Picture for the Broad Market

The S&P 500 posted a strong five-day rally after rebounding from the 100-day moving average near 6,550 points. As a result, the benchmark has moved above the 20-day moving average. The share of index constituents trading above their 20-day moving average has reached a three-month high, rising above 75%, indicating that the rally is broadening beyond the mega-cap names. The RSI confirms additional room for upside (no overbought conditions). The primary target for the bulls is the all-time high at 6,920; a breakout would open the path toward 7,000. Support levels for the broad market lie at 6,650 and 6,770.

Expected Trading Range

We expect the S&P 500 to trade in the 6,650–7,000 range.