Investment Review №334. Customer return

Macro data for the Armenian market is favoring the bulls

High GDP growth rates and strong business activity can support demand for local market assets.

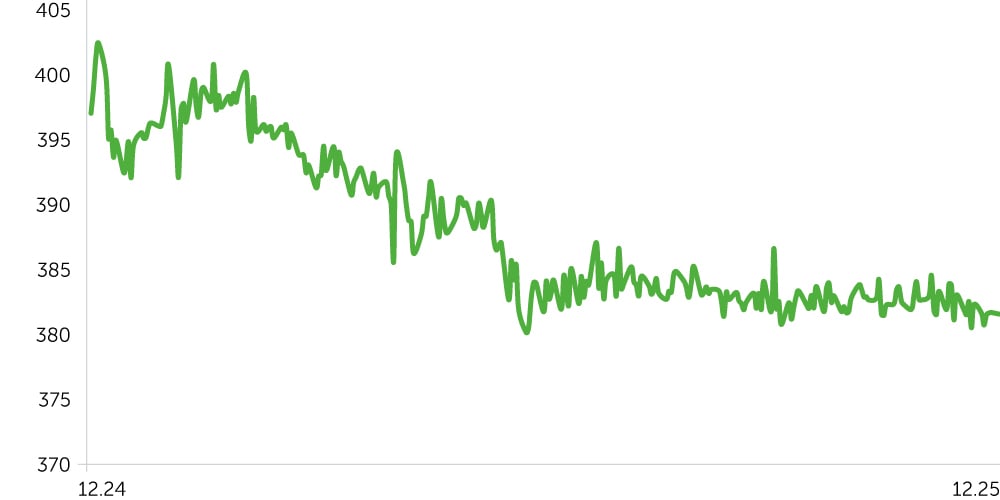

Telecom Armenia: 1-Year Stock Trends

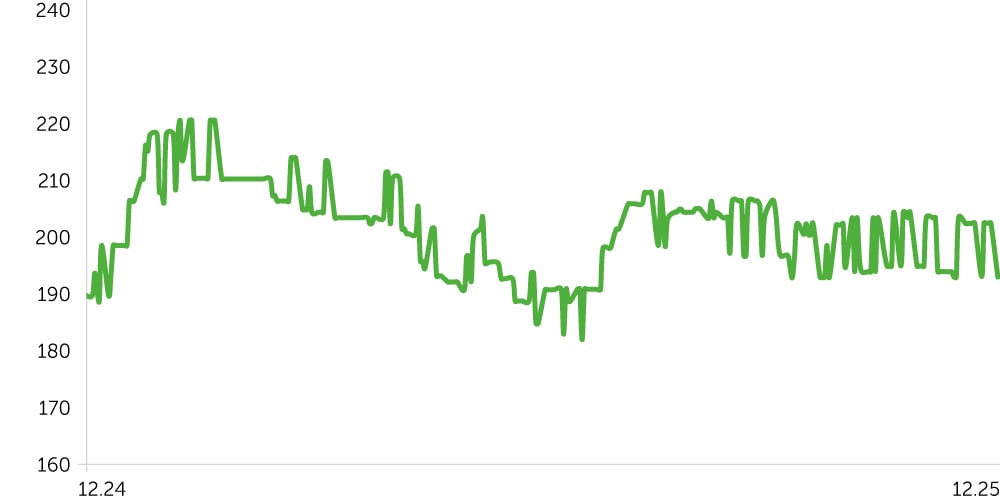

ACBA Bank: 1-Year Stock Trends

USD/AMD: 1-Year Dynamics

Armenian Market Overview

From November 17 to December 1, 2025, Armenia’s equity market showed mixed performance. Shares of ACBA Bank (ACBA) rose 0.6%, approaching their highest levels since February 2025. Strong macroeconomic data — notably faster-than-expected GDP growth in Q3 and an above-consensus business-activity index for October — offered fundamental support to sentiment. Still, despite the positive news flow that would normally stimulate investment activity, structurally low liquidity in the local market continues to weigh on the efficiency of price formation. As a result, Telecom Armenia (AMTL) shares once again edged lower, declining 4.7% and remaining within the sideways range established since mid-2025.

In the debt market, the price index of three-year AMD-denominated corporate bonds increased 0.2% as yields moved lower. Macroeconomic statistics continue to confirm price stability: the Producer Price Index (PPI) for October rose 5.9% YoY, in line with expectations, helping keep real yields at attractive levels. The FX market remains stable: the dram appreciated 0.4% against the U.S. dollar over the period, bringing total year-to-date strengthening to 3.9%. On the other hand, foreign-trade data for October showed an unexpected widening of the trade deficit, though it is important to note some recovery in export and import volumes (excluding re-exports of precious metals and stones).

Economic Updates

Between November 17 and December 1, 2025, Armenia’s macroeconomic backdrop was marked by strong GDP growth and elevated economic activity, alongside stable inflation. At the same time, a notable widening of the trade deficit was recorded; however, this may prove to be a one-off development.

- Armenia’s GDP grew 6.2% YoY in Q3 2025, exceeding expectations of 5.9% in the preliminary estimate and accelerating from 5.2% YoY growth in Q2. Capital-intensive industries were the main contributors: construction rose 24.6% YoY, electricity/gas/steam supply increased 21.7% YoY, and administrative and support services grew 18.4% YoY, pointing to an ongoing investment cycle in infrastructure and private real-estate development. Sectors shaping the economy’s long-term potential also made significant contributions: information and communications expanded 17.6% YoY, while finance and insurance grew 10.5% YoY. Downside pressure came from education (−3.3% YoY) and mining (−3.0% YoY), though their weight in total GDP is limited. Overall, the data confirm the economy’s relative resilience to external shocks, and the above-trend momentum may continue to support risk appetite for local assets.

- Economic activity in October also exceeded expectations, accelerating to 10.1% YoY (vs. 8.0% expected), well above the growth rates of prior months. On a monthly basis, the index declined 4%, likely reflecting seasonality. Construction remains the key driver, rising 20.1% YoY in October. Services excluding trade also showed strong performance, up 12.8% YoY. Domestic trade grew more modestly at 1.0% YoY. Overall, the data — together with Q3 GDP — confirm the economy’s resilience and indicate potential for growth to exceed the baseline projections of the World Bank (5.2%) and the Ministry of Finance (5.1%) for 2025, a moderately positive signal for the country’s investment climate.

- The trade deficit in October reached its widest level since March 2023. Exports fell 21.8% YoY, imports declined 11.9% YoY, and total foreign-trade turnover decreased 16% YoY. However, monthly dynamics point to stabilization: exports rose 12% MoM, imports increased 21.8% MoM, and trade turnover expanded 17.8% MoM. The annual decline largely reflects reduced re-exports of precious metals. Excluding imports and exports of (semi-)precious metals and stones, exports and imports grew 7.1% and 7.5% YoY, respectively. The recovery in both exports and imports compared with the prior month may indicate a normalization of trade flows. Nonetheless, all else equal, a widening trade deficit could put pressure on the dram if sustained, although the October figures appear to be largely priced into current exchange-rate levels.

Corporate News

- Firebird, a company planning to build a large-scale AI data center in Armenia, has received a license from the U.S. government allowing it to import NVIDIA graphics processors into the country, Presswire reports. According to the plan, the data center will use AI servers supplied by Dell Technologies Inc. and will be built on NVIDIA’s Blackwell-generation GPUs.

Two-Week Outlook

Between December 5 and 15, only a limited amount of macroeconomic data is scheduled for release, and we do not expect the publication of revised indicators to materially affect the assessment of current economic conditions.

The key release will be November consumer-price inflation, where annual CPI growth is expected to accelerate from 3.1 percent in October to roughly 3.7 percent YoY. We consider it unlikely that the new inflation data will produce meaningful surprises for the market or lead to a shift in the Central Bank’s monetary-policy stance. With price dynamics stabilizing and economic growth remaining strong, we expect the regulator to keep the refinancing rate at the current 6.75% level in the short and medium term — including at the upcoming mid-December meeting. Under these conditions, maintaining positive real yields should provide moderately supportive demand in the local financial market, particularly in the bond market, which continues to attract substantial investor interest.