Investment Review №346. Riding the Green Wave

Corporate News in Focus of Our Analysts

AvalonBay, Equity Residential

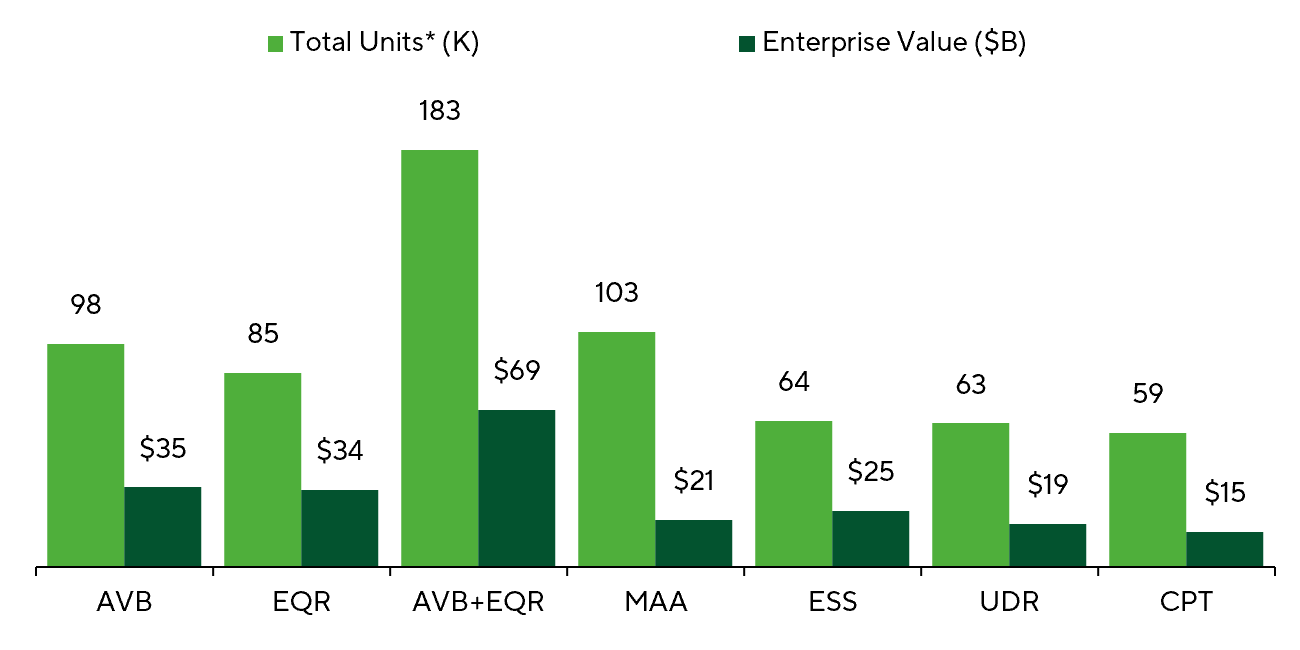

AvalonBay Communities (AVB) and Equity Residential (EQR) announced an all-stock merger on May 21, 2026. The deal marks the largest REIT combination in U.S. history. The transaction brings together the country’s two largest residential real estate portfolios, creating a company with a market capitalization of roughly $52bn and an enterprise value of around $69bn. The combined company will manage approximately 183k apartments.

AvalonBay shareholders will receive 2.793 EQR shares for each AVB share and will own 51.2% of the new company. EQR shareholders will own the remaining 48.8%. AvalonBay CEO Benjamin Schall will lead the combined company. The transaction is expected to close in 2H26, subject to approval by shareholders of both companies.

The merger economics are built around scale. Management expects the combined company to generate annual gross savings of $175m and net savings of $125m within roughly 18 months. The dividend will remain at $2.81/share, in line with Equity Residential’s current payout. Notably, even after the merger, the combined company’s market share will not exceed 3%, meaning the transaction does not require antitrust approval. At the same time, the scale of the deal could set the tone for a new wave of consolidation in the historically fragmented rental housing sector.

Comparison of the Largest Rental Housing REITs

Source: Company filings as of March 31, 2026, and FactSet as of June 1, 2026.

* “Number of apartments” includes projects under construction and apartments in unconsolidated JVs. JV assets are included in full, without adjustment for ownership share.

Zscaler

Despite the sharp selloff following conservative FY2027 guidance, Zscaler’s fundamentals remain solid. Revenue and ARR both increased 25% YoY, operating margin reached a record 23%, and demand for Zero Trust and AI Security solutions continues to accelerate. Management built more cautious assumptions into the outlook due to the Red Canary integration, sales-organization realignment, and temporary softness in new customer acquisition. The existing customer base, however, remains highly resilient, with cross-selling accounting for two-thirds of ARR growth. Additional growth drivers include the Z-Flex platform, expansion of the AI business, and the pending acquisition of Symmetry Systems. In our view, the market is overly focused on the near-term slowdown in ARR growth to 16–17% YoY, while underappreciating Zscaler’s continued leadership in cloud cybersecurity, high customer retention, and the potential for growth to reaccelerate once the commercial restructuring is complete. Key risks include higher CapEx, personnel changes, and slower new customer acquisition in FY2027.

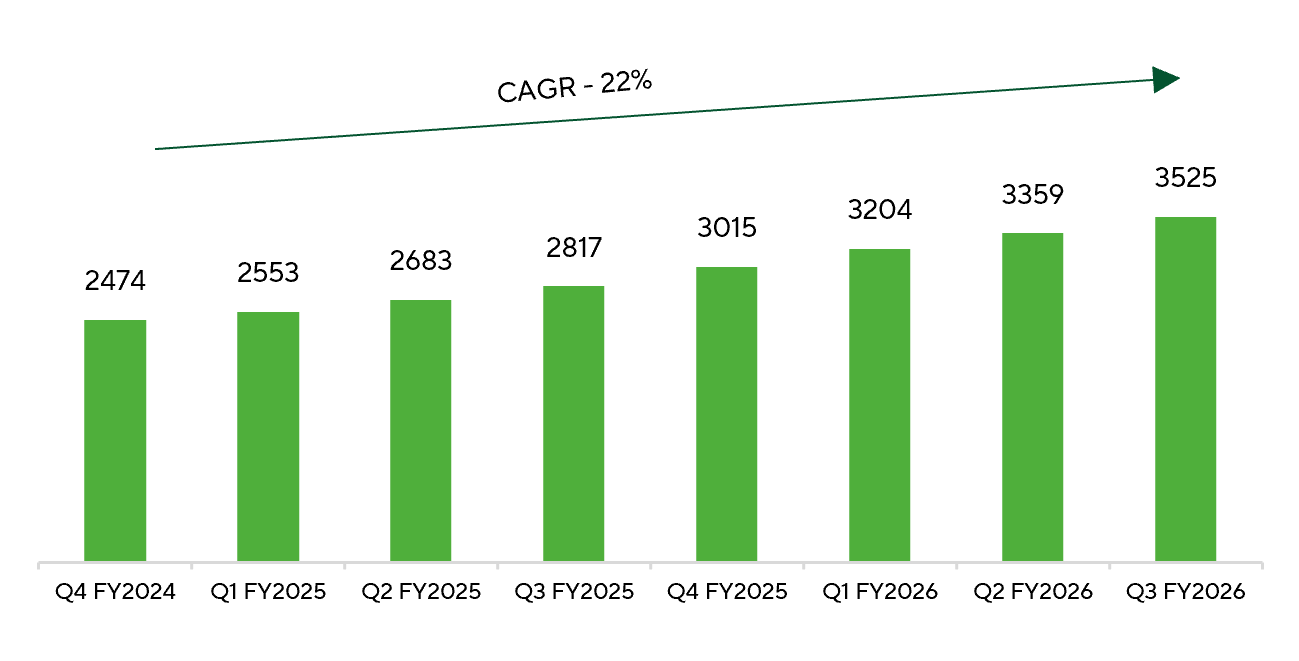

Zscaler Annual Recurring Revenue (ARR) Growth ($ millions)

Source: Zscaler IR presentation.

AMD, NVIDIA, Qualcomm, Marvell Technology, Intel

GTC 2026 and Computex 2026, held in Taiwan in the first week of summer, clarified the competitive landscape: the market is moving toward agentic AI, and the winners will be those controlling the largest share of the value-creation stack. Nvidia Corp. (NVDA) once again walked investors through its data-center roadmap, confirming full-scale production of Vera Rubin, with initial shipments already expected this fall.

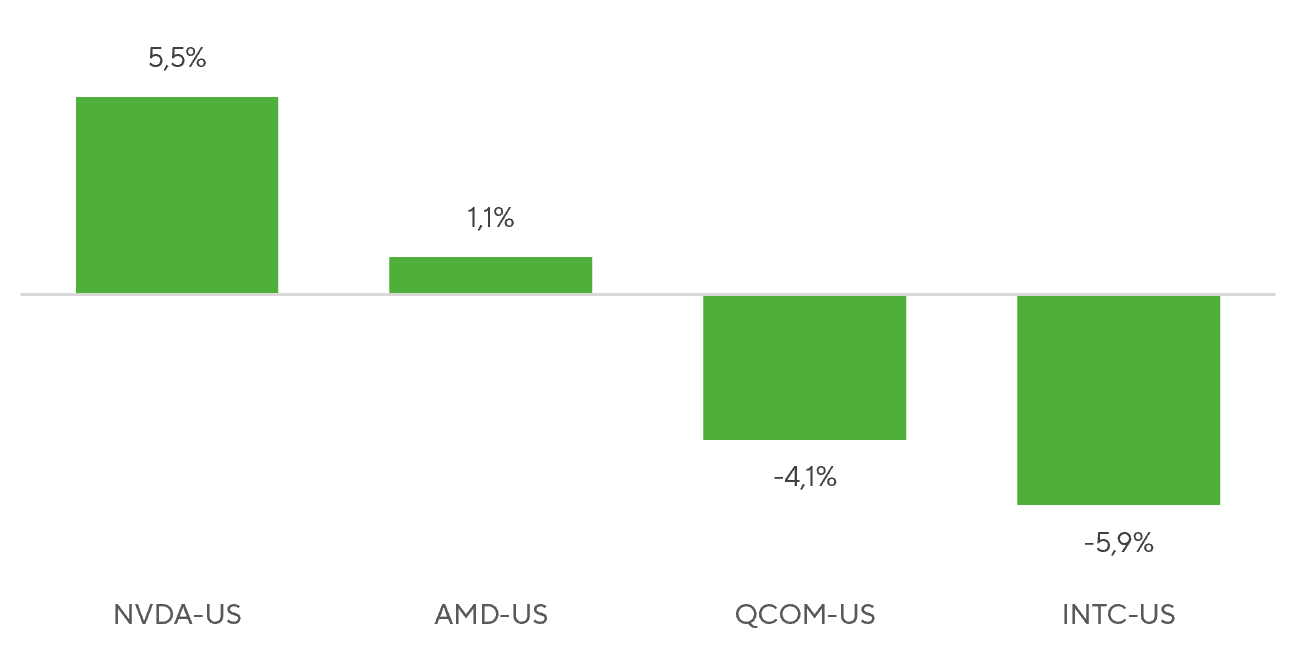

The company also reiterated its recent forecast that the server CPU market could reach $200bn by 2030. At the same time, Nvidia also pushed directly into rival territory: consumer CPUs, with the launch of RTX Spark, an Arm-based SoC for Windows PCs combining a Grace CPU, Blackwell GPU, and up to 128GB of unified memory. The product was presented at GTC together with Microsoft. The message was clear: Arm-based Windows laptops will no longer be limited to Qualcomm (QCOM) chips. In his remarks, Jensen Huang also positioned himself as a defender of software companies, which, despite weak market sentiment, triggered an unexpectedly strong rally across the group. We also highlight Huang’s joint appearance on stage with Marvell Technology (MRVL) management, where he predicted that Marvell could become the next trillion-dollar company. At Computex, Intel Corp. (INTC) delivered the most content-heavy presentation, while Advanced Micro Devices (AMD) and Qualcomm held back their major announcements for their own events in June and July. Lip-Bu Tan’s forward-looking presentation still failed to give investors what they wanted most: fresh progress in the foundry business, including confirmation of new customers, and details on the next-generation Jaguar Shores AI accelerator. Following Nvidia’s aggressive push into the consumer segment, NVDA shares rebounded strongly after the prolonged correction that followed its quarterly report, which was exceptionally strong across all key metrics. AMD recovered its initial Tuesday decline, while INTC and QCOM started June under pressure.

Stock Price Performance, June 1–2, 2026 (%)

Source: FactSet, Freedom Broker analysis

Snowflake

Snowflake delivered strong quarterly results ahead of expectations. The company is entering a new phase of growth, where AI is no longer a marketing story but a real driver of platform demand. Management raised guidance, confirming business acceleration and growing confidence in the durability of the current trend. Importantly, customers are not just testing new AI tools. They are starting to scale them across workflows, increasing the long-term value of the platform and creating a stronger base for further consumption growth.

The expanded strategic partnership with AWS provided another validation point, with commitments of more than $6bn. The agreement strengthens Snowflake’s position inside the world’s largest cloud ecosystem and serves as external confirmation that demand for the company’s solutions can continue to expand for years. Over the next several years, Snowflake has the potential to become one of the key infrastructure platforms for enterprise AI, combining data, analytics, and AI applications within a single ecosystem. The combination of accelerating AI adoption and long-term AWS support materially increases the probability that Snowflake can sustain high growth rates and continue to raise guidance over time.

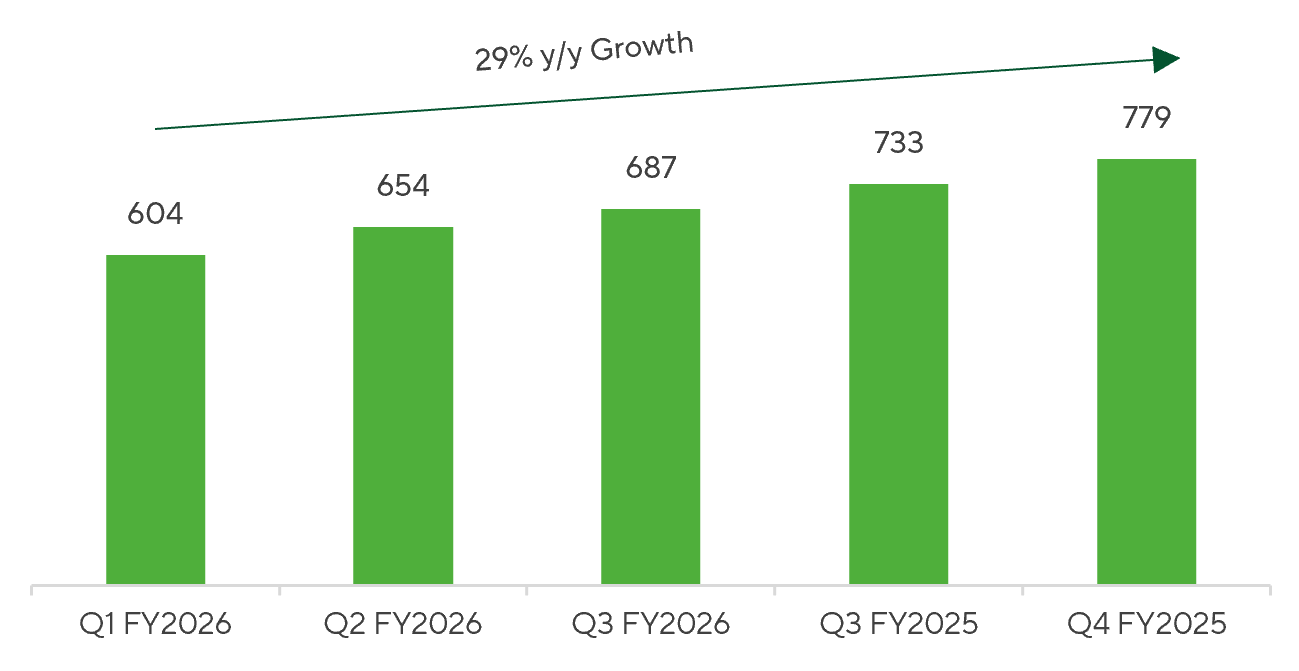

Growth in Customers Generating More Than $1 Million in Product Revenue

Source: Snowflake IR presentation

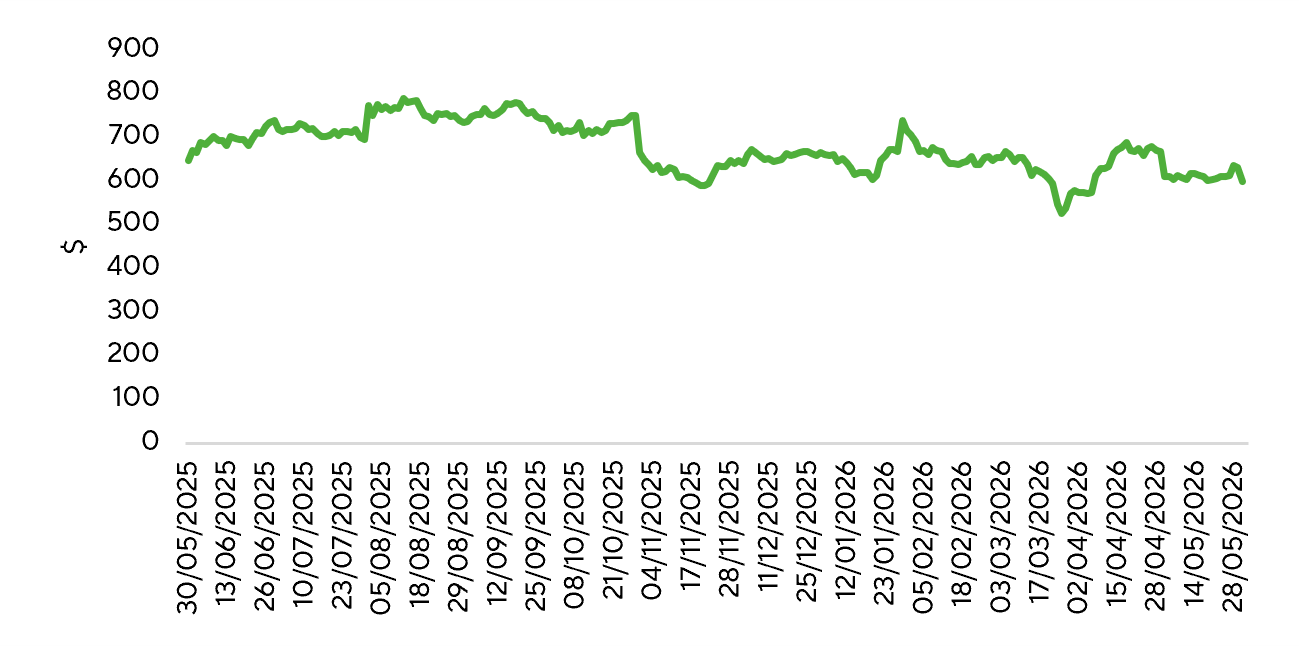

Meta Platforms

Meta is rolling out new subscription products, marking a broader push to diversify revenue beyond advertising and partially offset rising AI infrastructure spending. The company is launching consumer subscriptions Instagram Plus and Facebook Plus at $3.99/month, alongside WhatsApp Plus at $2.99/month. Instagram Plus and Facebook Plus will include Stories and views analytics, expanded reactions, audience lists, profile customization, and additional pinned items. Meta also said more entertainment features will be added over time. WhatsApp Plus will offer themes, ringtones, premium stickers, and more pinned chats. Meta is also introducing paid access to AI features through Meta One Plus at $7.99/month and Meta One Premium at $19.99/month. The Premium tier will offer more computing power, deeper reasoning, and expanded image and video generation. For businesses and creators, Meta One Essential at $14.99/month and Meta One Advanced at $49.99/month will include verification, impersonation protection, analytics, and planning tools. The operating model for these subscriptions will likely be built around Muse Spark, the recently introduced model developed by Meta’s new Superintelligence Labs division.

Meta’s advantage is scale: Instagram, Facebook, and WhatsApp give the company massive distribution and a clear path to embedding AI into everyday consumer and business workflows. The key test will be execution. Competition with OpenAI, Anthropic, and Google’s Gemini will depend on model quality and whether users see enough value to pay.

Meta stock price dynamics