Investment Review №327. The soft power of the Federal Reserve

At rest

Moderately positive macroeconomic data was accompanied by sideways movement in stock market prices.

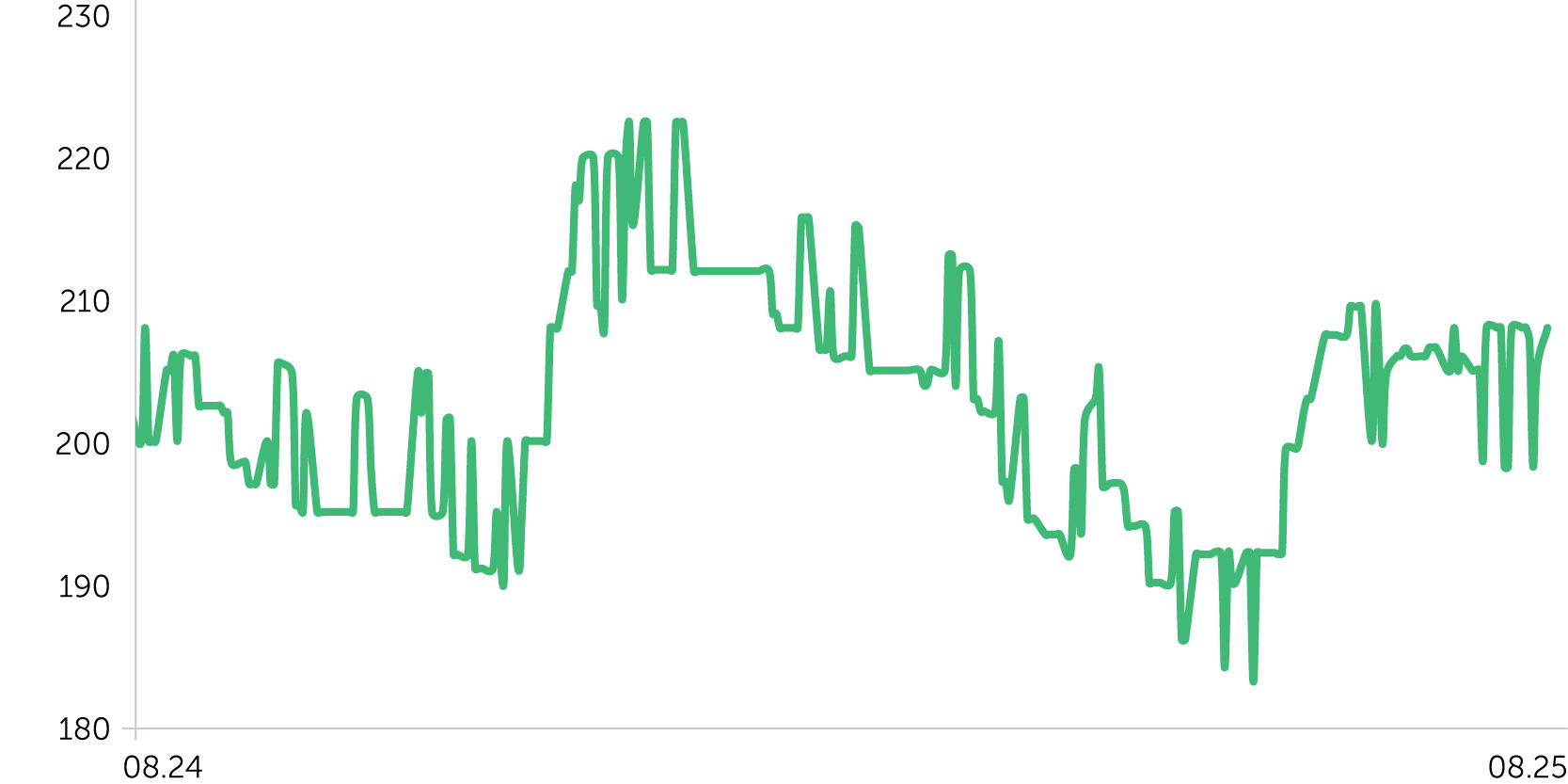

Telecom Armenia: 1-Year Stock Trends

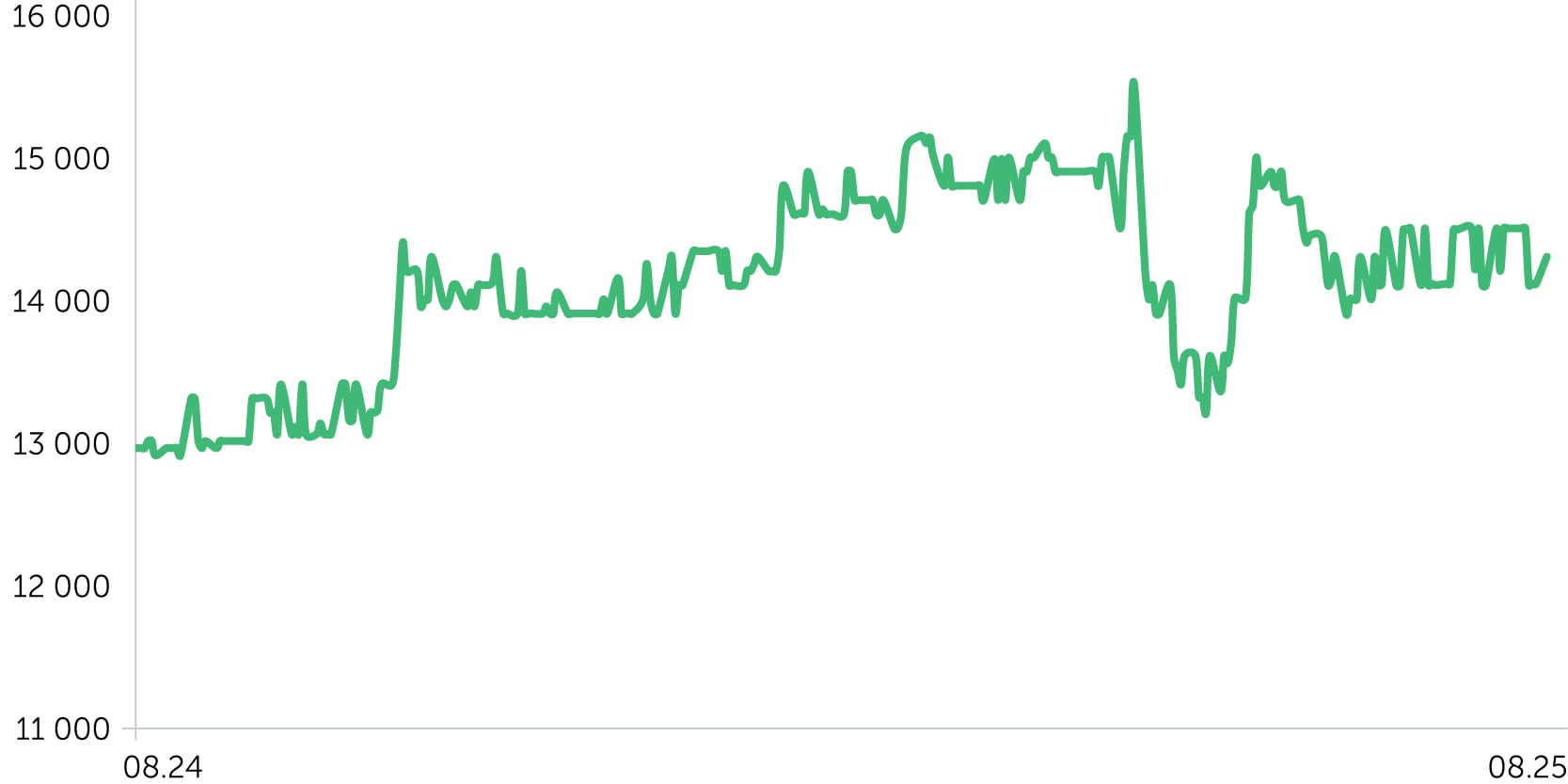

ACBA Bank: 1-Year Stock Trends

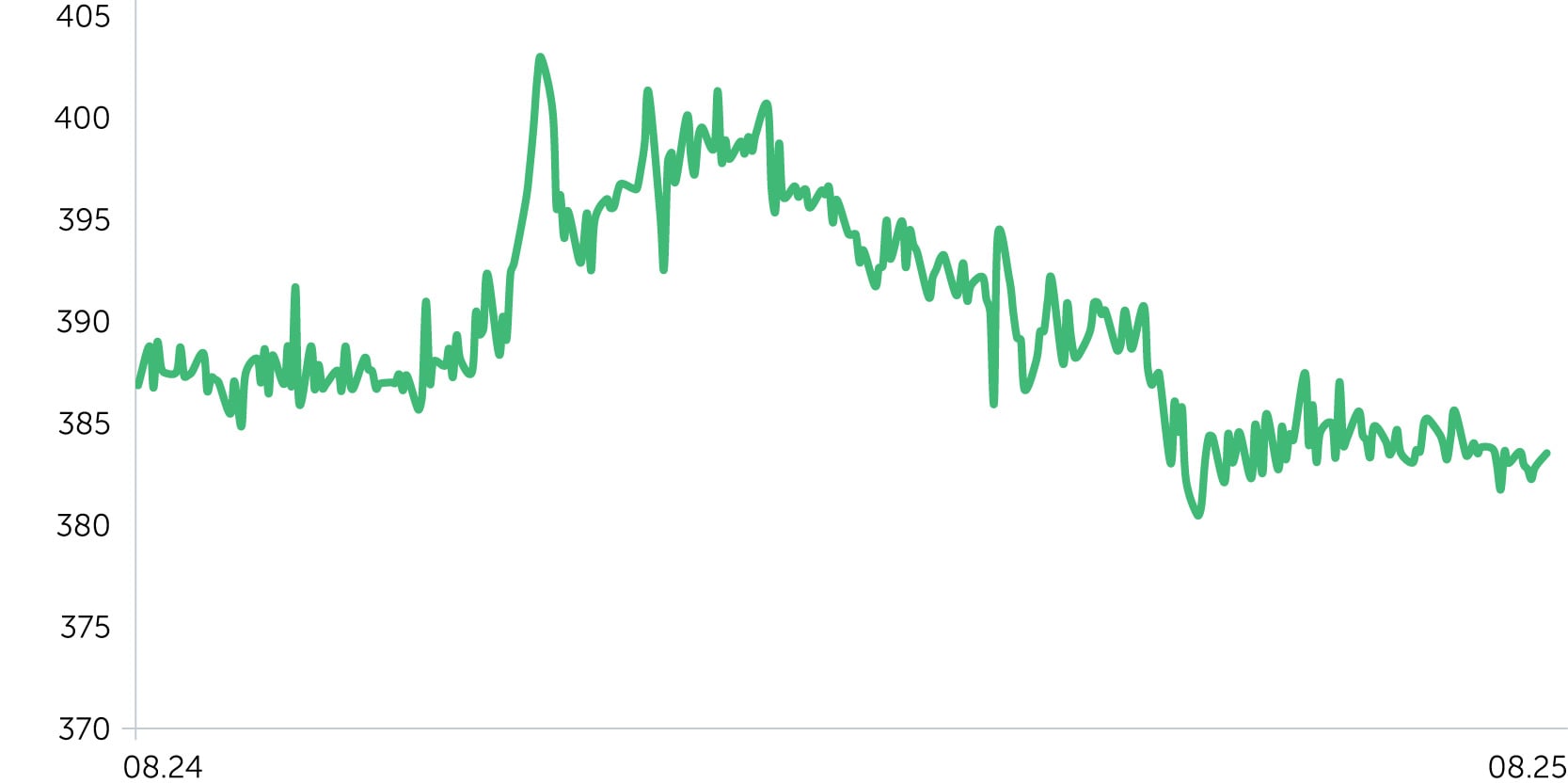

USD/AMD: 1-Year Dynamics

During the observed period from August 11 to August 25, 2025, Armenia's stock market exhibited moderately negative performance, despite the country's positive macroeconomic indicators. Notably, GDP growth and economic activity surpassed forecasts, and industrial production returned to a year-over-year growth trajectory in July for the first time since October 2024. However, due to the stock market's limited diversity and concentration in few sectors, these macroeconomic improvements did not translate into broad stock market gains. For instance, shares of Acba Bank declined by 1.4% during this period and have generally been trading within a narrow range since early July. Relevant company developments include the issuance of bonds in both Armenian dram and U.S. dollars, amounting to AMD 10 billion (approximately $26.3 million) and $10 million, respectively, which may suggest intentions to expand its loan portfolio. Meanwhile, Tell Cell's shares experienced a decline of 5.1%. In contrast, Telecom Armenia (AMTL) showed no change in its stock value during the same timeframe.

The price index for three-year AMD-denominated corporate bonds experienced a marginal decline of 0.1%, following a recent upturn, resulting in moderately increased bond yields. We attribute this movement to robust macroeconomic data and stable inflation, which we believe solidify market expectations that the regulator will maintain current refinancing rates in upcoming meetings. This anticipation may reduce interest in medium to long-term bonds and exert upward pressure on yields. Concurrently, the Armenian dram has marginally strengthened against the U.S. dollar, maintaining stability despite indications of an expanding foreign trade deficit. This widening could potentially be mitigated by inflows from remittances, capital investments (FDI, portfolio investments), and revenues from the tourism sector. Notably, July 2025 saw a record number of tourists visiting Armenia, marking a 10.9% increase year-over-year.

Economic Updates

Between August 11 and August 25, 2025, macroeconomic data on Armenia were released, highlighting GDP growth for the second quarter and an acceleration in economic activity in July. A key driver of this uptick was the industrial sector, which expanded for the first time in several months. Concurrently, foreign trade trends revealed positive dynamics, suggesting a potential upward trajectory.

- Armenia GDP growth exceeds expectations in Q2. Preliminary data from the Statistical Committee of Armenia indicates that the nation's GDP grew by 5.9% y/y in Q2, surpassing the anticipated 4.0% y/y. Key sectors contributing to this robust growth include finance and insurance (+7.5% y/y), information and communication (+20.3%), and construction (+24.4%), while the trade sector exhibited a modest increase of 3.1%. The stronger-than-expected GDP performance in Q2 is likely to prompt market participants to revise their annual growth forecasts upward, with the Eurasian Development Bank currently predicting a 5.5% growth rate and the World Bank forecasting 4% growth in 2025.

- July economic activity exceeds expectations; industrial sector returns to growth. Armenia's economic activity index rose by 9.1% y/y and 5.5% m/m in July, outpacing the anticipated figure of 7.0%. The construction and services sectors continue to be the primary catalysts for the index's growth, while the industrial sector posted its first increase since November 2024, with a year-over-year rise of 4.2%.

- Exports, imports improve in July; trade deficit widens. In July, Armenia experienced a 14.3% y/y decrease in foreign trade turnover, accompanied by a marginal 0.2% m/m decline, following a 16.6% reduction in June. Specifically, exports recorded a 10.8% y/y decline, improving from a 15.9% drop in June, while declining by 5.3% m/m. Concurrently, imports fell by 16.5% y/y, slightly better than the 17.1% decrease noted in June, yet recorded an increase of 3.7% m/m. Consequently, the trade deficit expanded modestly from $228 million in June—marking the lowest point since April 2024—to $308 million in July.

Corporate News

- ACBA Bank has announced a public offering of non-documentary bonds totaling AMD 10 billion and $10 million, consisting of 100,000 bonds for each currency. These bonds will mature on August 25, 2030. The coupon rates are set at 10.50% for AMD-denominated bonds and 5.50% for USD-denominated bonds. The placement period will span from August 25 to December 25, 2025. Each bond will have a nominal value of AMD 100,000 or $100,000, respectively.

- Ameriabank CJSC is set to launch a public offering of registered, non-documentary bonds across three currencies, featuring quarterly coupon payments from September 1 to November 7, 2025. The issuance will include $15 million in USD-denominated bonds with a 36-month maturity and a 5% coupon rate. Additionally, the bank will offer bonds totaling €10 million, carrying a 24-month maturity and a 3.5% coupon rate. In Armenian drams, the issuance volume will be AMD 12 billion, with a maturity of 36 months and a 9.75% coupon rate.

Two-Week Outlook

Between August 29 and September 8, the release of new macroeconomic data is expected to be sparse. However, there may be updates to previously released indicators.

The primary event in focus is the upcoming release of the country's Consumer Price Index (CPI) for August. Analysts predict a modest acceleration in inflation, with expectations for the rate to shift from 3.4% in July to 3.6% in August. This increase is likely driven by robust demand in the services sector and a low base effect from the previous year. In the days following the CPI release, the Central Bank is scheduled to convene to evaluate monetary policy directions. Currently, consensus forecasts suggest the refinancing rate will remain unchanged, conditional on the inflation data confirming expectations without indicating heightened fundamental price pressures.

Overall, the macroeconomic environment remains conducive to growth. Economic expansion is being bolstered by both seasonal factors, such as a strong tourist season, and potentially more structural shifts. In this context, the continuity of growth observed in the industrial sector in July may become a crucial indicator for evaluating the economy's long-term prospects in the coming months.